Bypassing Hormuz: Gulf Pipeline Network Plans Mark Structural Shift in Energy Security and Regional Leverage

Gulf states are revisiting costly pipeline networks to bypass the Strait of Hormuz amid heightened risks, signaling a potential long-term transformation in global oil logistics, shipping economics, and Middle East power balances that integrates with broader trade corridors like IMEC.

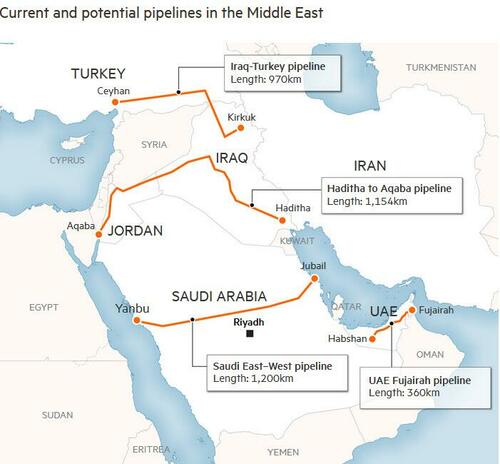

Recent reporting indicates that Gulf states are accelerating consideration of new pipelines and expanded existing routes to reduce dependence on the Strait of Hormuz, a chokepoint that has long been central to global oil flows. According to the U.S. Energy Information Administration's World Oil Transit Chokepoints analysis, approximately 21 million barrels per day of crude oil and petroleum products passed through the strait in 2022, representing about one-fifth of global consumption. The FT report cited by ZeroHedge underscores that the East-West pipeline, constructed in the 1980s during the Iran-Iraq War's tanker conflict, is now operating at or near its 7 million barrels per day capacity, delivering to Yanbu on the Red Sea. Saudi Aramco CEO Amin Nasser recently highlighted its strategic role in current operations.

This coverage builds on historical patterns seen during the 1980s 'tanker war' and 2019 attacks on shipping, yet original reporting largely frames the issue as an immediate response to ongoing conflict without fully connecting it to longer-term structural trends. What is missed is how these plans align with Saudi Vision 2030's emphasis on Red Sea development, including Neom's deepwater port, and the stalled India-Middle East-Europe Economic Corridor (IMEC) proposed in 2023, which envisioned rail and potential pipeline links from the Gulf to Europe. Primary documentation from the EIA shows repeated vulnerabilities at multiple chokepoints, including the Bab el-Mandeb strait, where recent disruptions have compounded risks.

Synthesizing perspectives, Gulf officials and executives, as quoted in the FT, view a 'web of corridors' as essential for resilience, moving beyond individual projects to networked infrastructure that could also transport non-oil goods. Israeli energy executive Yossi Abu emphasized controlling 'own destinies' through onshore routes. However, this must be balanced against Iranian statements in official media that such bypasses represent attempts to circumvent legitimate regional security concerns, potentially heightening tensions rather than resolving them. Construction firms like Cat Group note inquiries predating recent escalations, with costs estimated at $5 billion to replicate the East-West line and $15-20 billion for multi-country routes through Iraq or Oman, per industry engineering studies.

The original ZeroHedge piece correctly flags urgency but underplays political complexity: pipelines require cross-border agreements on operation and revenue sharing, challenging the 'individualist policies' historically preferred by Gulf producers who favored tanker exports. Multiple viewpoints emerge on global impacts—shipping industry analyses suggest reduced tanker demand through Hormuz could ease insurance premiums and alter freight rates, while OPEC reports emphasize that new land routes might stabilize supply but introduce new vulnerabilities to terrestrial disruptions such as those from militant groups in Iraq. Environmental considerations from primary IEA assessments also warrant note, as expanded fossil infrastructure could conflict with net-zero timelines.

In synthesis with the EIA chokepoints report and the 2023 IMEC joint statement by participating governments, these developments point to a potential permanent alteration in Middle East geopolitical leverage. Iran's influence via the strait may diminish if alternatives scale, yet high costs, security risks including unexploded ordnance, and the need for regional cooperation present substantial barriers. This reflects a broader pattern where energy infrastructure increasingly serves as both economic and strategic tool, observed similarly in Eurasian pipeline politics. Outcomes remain contingent on sustained threat levels and diplomatic alignments, with near-term focus likely on expanding Fujairah and East-West capacities rather than entirely new cross-border webs.

MERIDIAN: Gulf pipeline expansion could gradually erode Iran's Hormuz leverage over 20% of global oil flows while integrating with multimodal trade routes, yet formidable costs and coordination challenges mean this shift will likely strengthen resilience without fully eliminating maritime dependencies.

Sources (3)

- [1]Gulf States Considering Network Of New Pipelines To Bypass Strait Of Hormuz(https://www.zerohedge.com/energy/gulf-states-considering-network-new-pipeliness-bypass-strait-hormuz)

- [2]Gulf states seek oil export alternatives as Hormuz risks rise(https://www.ft.com/content/gulf-pipelines-hormuz-bypass-2026)

- [3]World Oil Transit Chokepoints(https://www.eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints)