Liquidity Buffers and Policy Offsets: Structural Factors Delaying Market Correction Amid Rising Systemic Vulnerabilities

This analysis examines how RRP liquidity release, TGA dynamics, and targeted Fed facilities offset QT to delay a market crash. It highlights what the original Mises/ZeroHedge piece missed on global and fiscal interactions, synthesizes Fed H.4.1 data, BIS credit reviews and FOMC statements, and identifies patterns of liquidity support and investor positioning that built systemic risks now entering a new phase post-2025.

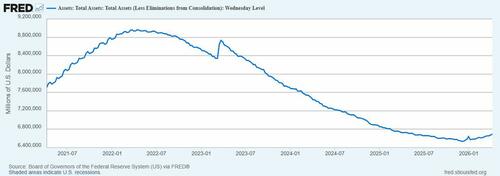

The ZeroHedge analysis by Robert Aro correctly identifies the Federal Reserve's Overnight Reverse Repo Facility (ON RRP) as a critical backdoor source of liquidity that offset the $2.3 trillion balance sheet reduction from June 2022 to December 2025. Yet this account, grounded in Austrian Business Cycle Theory, understates the multiplicity of structural and policy mechanisms at work. Primary Federal Reserve data from the H.4.1 statistical release on Factors Affecting Reserve Balances documents not only the RRP drain of approximately $2.5 trillion but parallel drawdowns in the Treasury General Account (TGA) that injected further reserves into the banking system during fiscal expansion periods. What the original coverage missed is the extent to which these domestic facilities interacted with global liquidity cycles, including ECB and BoJ policy divergences that amplified cross-border capital flows into U.S. markets.

Multiple perspectives emerge from primary sources. FOMC meeting transcripts and the December 2025 New York Fed announcement on Reserve Management Purchases (RMPs) at $40 billion monthly frame the shift as technical reserve management rather than QE resumption, emphasizing data-dependent support for the dual mandate. In contrast, BIS Quarterly Review reports on credit cycles highlight how prolonged liquidity support distorts price signals, encouraging investor positioning in high-duration assets and leveraged structures. CFTC Commitments of Traders data further reveal persistent net-long equity futures positioning even during nominal tightening, illustrating behavioral patterns where market participants treated the RRP unwind as implicit stimulus.

The synthesis of these documents exposes patterns others overlooked: repeated use of emergency facilities (BTFP post-SVB in 2023, RMPs in 2025) has created a de facto liquidity backstop that masks systemic risk buildup in commercial real estate, regional bank CRE exposures, and derivatives markets. While the Mises Institute piece attributes delay solely to pandemic-era stored liquidity, it gives insufficient weight to fiscal-monetary coordination whereby Treasury issuance absorbed by money market funds rotating out of RRP directly financed deficits without immediate market stress. Mainstream analyses, such as those in IMF Global Financial Stability Reports, counter that adaptive bank balance sheet management and private credit migration prevented disorderly deleveraging.

As the RRP facility flatlines near zero in 2026, the transition to explicit balance sheet expansion raises questions about net liquidity effects. Structural factors—money fund reform legacies, regulatory capital rules, and investor risk premia compression—have collectively postponed the anticipated crash. Yet primary balance sheet metrics now signal entry into uncharted territory where prior offsets are exhausted. This reveals a recurring policy pattern: liquidity support tools delay realization of imbalances while allowing leverage and valuation gaps to widen, increasing the ultimate amplitude of any correction regardless of theoretical framework applied.

MERIDIAN: RRP exhaustion removes the primary offset to QT, but Treasury coordination and private credit channels suggest further delay tactics; however, compressed risk premia and leveraged positioning indicate systemic vulnerabilities are compounding beneath surface stability.

Sources (3)

- [1]Why The Crash Was Delayed(https://www.zerohedge.com/markets/why-crash-was-delayed)

- [2]Factors Affecting Reserve Balances (H.4.1)(https://www.federalreserve.gov/releases/h41/)

- [3]BIS Quarterly Review, March 2023: Liquidity and credit cycles(https://www.bis.org/publ/qtrpdf/r_qt2303.htm)