Kazakhstan's Strategic Uranium Reserve Signals Structural Global Nuclear Supply Vulnerabilities Amid AI Demand Surge

Kazakhstan's uranium reserve initiative exacerbates a tightening global market amid AI-driven nuclear demand, revealing structural energy security risks that transcend the U.S.-centric focus of initial coverage and point to broader fragmentation in nuclear supply chains.

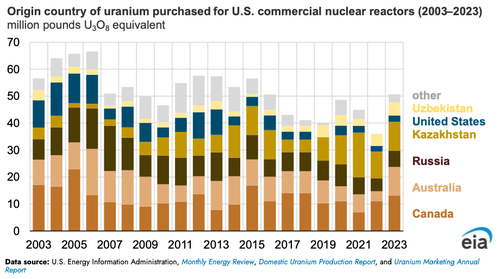

Kazakhstan's newly approved strategy to accelerate geological exploration at a minimum of two prospective uranium deposits annually and establish a strategic reserve, as detailed in the presidential decree signed by President Kassym-Jomart Tokayev, extends beyond domestic resource management. While the ZeroHedge coverage correctly identifies this as further evidence of a global supply-demand imbalance and notes Kazakhstan's status as the top producer with approximately 14% of global confirmed resources, it frames the issue predominantly through the lens of U.S. reactor fleet vulnerabilities and lagging construction compared to China. This treatment overlooks the deeper structural realignment in energy security that treats uranium less as a commodity and more as a strategic asset akin to rare earth elements or petroleum reserves.

Primary documents provide essential context. Kazakhstan's official strategy document emphasizes securing long-term feedstock for planned domestic nuclear power stations, optimizing sulfuric acid supply for in-situ recovery operations, and ensuring full utilization of future conversion and enrichment capacity with indigenous uranium. The IAEA-OECD Nuclear Energy Agency 'Uranium 2022: Resources, Production and Demand' (Red Book) identifies identified resources recoverable at under $130/kgU at 6.1 million tonnes globally, yet notes that exploration expenditures have declined significantly since 2016 peaks, creating a lagged response to post-2022 demand signals. World Nuclear Association supply analyses corroborate Kazakhstan's 43% share of world production in 2022-2023 while documenting how 12 of its 14 operating enterprises function as joint ventures with Chinese, Russian, French, Canadian, and Japanese entities, illustrating entangled geopolitical dependencies mainstream coverage rarely synthesizes.

What original reporting missed is the multi-vector nature of Kazakhstan's positioning. Rather than a simple market tightening, the reserve mirrors patterns seen in China's National Uranium Reserve Program and recent Australian and Canadian policy reviews on critical minerals. These moves occur against surging nuclear demand driven by AI hyperscalers. Microsoft’s 2024 agreements for small modular reactor development to power data centers and similar explorations by Google and Amazon represent a qualitative shift: computational infrastructure now directly competes with grid electricity for baseload nuclear output. This intersection was referenced but not deeply connected in the source material.

Multiple perspectives emerge. Producer nations view strategic reserves as prudent hedging against price volatility and resource nationalism, consistent with OPEC+ models. Consumer states, per U.S. Department of Energy assessments on nuclear fuel security, see heightened risks of supply weaponization, especially given Kazakhstan’s geographic position and historical Russian influence over regional enrichment pathways. Environmental and non-proliferation analyses from organizations like the OECD NEA caution that accelerated extraction could strain water resources in arid regions and complicate safeguards if enrichment capacity expands domestically.

The cumulative net deficit projected at over 200 million pounds through 2045 is not merely cyclical, as secondary market commentary often suggests, but reflects chronic underinvestment in mine development during the post-Fukushima era. China’s current construction of 39 reactors (per its National Nuclear Safety Administration filings) alongside India’s expansion under the Civil Nuclear Liability framework and U.S. restarts of shuttered facilities compound this. Mainstream coverage frequently presents these as isolated national decisions rather than evidence of a fragmented global nuclear fuel cycle transitioning from just-in-time markets to strategic stockpiling.

This development indicates a structural shift: energy security for nuclear-dependent economies, including those powering AI infrastructure, will increasingly depend on diversified sourcing, domestic revival of mining in aligned jurisdictions, and potential technological alternatives such as advanced fuel cycles. Kazakhstan’s plan, while bolstering its export credentials in the near term, may accelerate exactly the supply anxiety it seeks to mitigate for others.

MERIDIAN: Kazakhstan's strategic reserve will likely catalyze parallel moves by other major producers, prompting Western governments to accelerate domestic uranium and fuel-cycle investments while deepening bilateral fuel agreements with Australia and Canada over the next 5-7 years.

Sources (3)

- [1]Uranium Supply Crunch Worsens Amid Kazakhstan’s Plan For Strategic Reserve(https://www.zerohedge.com/energy/uranium-supply-crunch-worsens-amid-kazakhstans-plan-strategic-reserve)

- [2]Uranium 2022: Resources, Production and Demand (Red Book)(https://www.oecd-nea.org/jcms/pl_65376/uranium-2022-resources-production-and-demand)

- [3]Supply of Uranium - World Nuclear Association(https://world-nuclear.org/information-library/nuclear-fuel-cycle/mining-of-uranium/supply-of-uranium.aspx)