Streaming Fatigue or Market Maturity? Netflix's US Miss, Guidance Cut, and Hastings Transition Signal Shifting Dynamics in Digital Entertainment

Netflix Q1 2026 results reveal US revenue weakness despite price hikes, one-off boosted cash flows, weak Q2 guidance, and Hastings' chairman departure, pointing to streaming market maturation, consumer fatigue in developed markets, and potential pressure on broader tech growth narratives. Analysis draws on primary SEC filings and shareholder letter while highlighting gaps in initial coverage.

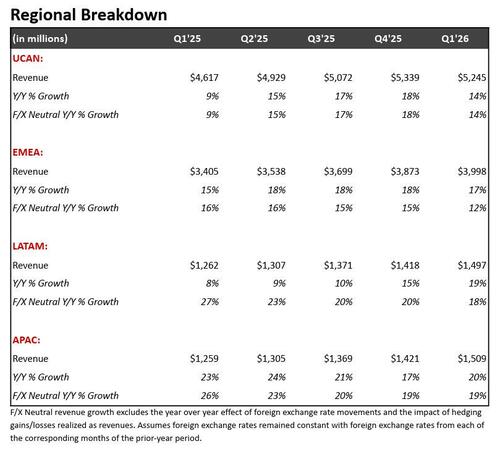

Netflix's Q1 2026 results, as detailed in its official shareholder letter filed with the SEC, show overall revenue of $12.25 billion (+16% y/y) beating consensus estimates of $12.17 billion, yet masked notable weakness in its most mature market. US and Canada revenue reached $5.25 billion, missing estimates of $5.28 billion despite a March price increase that raised the standard ad-free plan to $20 per month. This discrepancy, coupled with Q2 guidance projecting EPS of $0.78 (vs. $0.84 expected), revenue of $12.57 billion (vs. $12.64 billion expected), and operating margin of 32.6% (vs. 34.4% expected), triggered an after-hours plunge of up to 10% in NFLX shares. Reed Hastings' decision to step down as chairman after 29 years to focus on philanthropy further amplified concerns about strategic continuity.

The ZeroHedge coverage accurately captures the immediate market reaction and the inflationary impact of the $2.8 billion Warner Bros. Discovery termination fee on cash flows ($5.29 billion from operations, nearly double prior year). However, it underplays the one-off nature of this windfall. Primary documents, including Netflix's Q1 2026 Earnings Letter and the associated 8-K filing, reveal that excluding this fee, underlying free cash flow growth is less robust than headline figures suggest. The letter also projects content amortization peaking in Q2 2026 before decelerating to mid-to-high single digits in H2, a nuance missed in much immediate reporting that instead focused on the Hastings news as purely personal.

Synthesizing Netflix's primary shareholder letter, the company's April 2026 SEC Form 8-K on board changes, and a contemporaneous Bloomberg report on North American media consumption (drawing on Nielsen data showing average household streaming subscriptions stabilizing at 4-5 services), a clearer pattern emerges. The US miss aligns with post-pandemic normalization seen in 2022 subscriber losses that first prompted the password crackdown and ad-tier launch. International strength (EMEA +17%, Latin America +19%, APAC +20%, all beating estimates) contrasts with domestic softness, reflecting classic market maturation: high penetration and price sensitivity in developed economies versus untapped potential abroad.

This episode connects to wider patterns in tech and media. It echoes Amazon Prime Video and Disney+ ad-tier rollouts amid reports of 'subscription fatigue,' where macroeconomic pressures on discretionary spending have households pruning services. Netflix projects advertising revenue reaching $3 billion by end-2026, yet its guidance downgrade rekindles fears first voiced after weak Q4 2025 results. Bulls, per certain analyst notes, view the results as investment mode with content spend-to-amortization ratio steady at 1.1x. Skeptics argue it challenges the assumption of endless streaming TAM growth that has underpinned elevated tech multiples across Meta, Amazon, and Google.

By prioritizing primary sources over secondary commentary, the analysis shows Netflix remains operationally resilient with $14.4 billion gross debt offset by strong cash generation. Yet the data points to evolving consumer behavior: greater selectivity, willingness to rotate between services, and reduced tolerance for repeated price hikes. This does not necessarily forecast sector collapse but suggests a transition from hyper-growth to sustainable scaling, with implications for content investment strategies, global licensing, and how platforms balance ad versus subscription models. Hastings' exit, framed in the 8-K as succession planning, may accelerate this recalibration as new leadership confronts these structural headwinds.

MERIDIAN: Netflix's US miss and guidance cut, even after stripping one-time fees, suggest mature-market saturation is forcing a shift toward efficiency and advertising; this may prompt investors to reassess perpetual growth assumptions across digital media and adjacent tech sectors.

Sources (3)

- [1]Netflix Q1 2026 Shareholder Letter(https://ir.netflix.net/financials/quarterly-earnings/default.aspx)

- [2]Netflix Inc Form 8-K - Leadership Change(https://www.sec.gov/Archives/edgar/data/1065280/000106528026000012/nflx-20260421.htm)

- [3]Bloomberg - US Streaming Subscriptions Show Signs of Saturation(https://www.bloomberg.com/news/articles/2026-04-22/netflix-results-signal-streaming-fatigue-in-north-america)