Fed's Limited Arsenal: Monetary Constraints Meet Geopolitical Volatility in High-Leverage Environment

Analysis of Fed policy limits amid above-target inflation and financial leverage, incorporating geopolitical risk factors and multiple institutional perspectives from FOMC records, BIS reports, and IMF assessments, while noting gaps in domestic-only coverage.

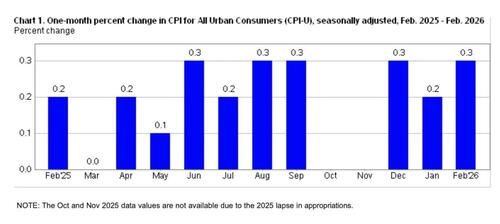

Recent market commentary has highlighted the Federal Reserve's narrowing set of viable policy options as inflation remains above target while signs of stress emerge in private credit, commercial real estate, and regional banking linkages. The ZeroHedge analysis correctly identifies the tension between 2.4% headline CPI and 2.5% core readings against the Fed's long-stated 2% objective, alongside the chain of leverage connecting private credit to private equity and bank balance sheets. However, this domestic-focused account understates the amplifying role of external geopolitical factors and overstates the complete exhaustion of tools by omitting ongoing debates around balance sheet management and international coordination.

Primary Federal Reserve documents, including the January 2026 FOMC minutes and Chair Powell's February 2026 Humphrey-Hawkins testimony, reveal internal discussions acknowledging 'elevated uncertainty' from global supply disruptions without committing to rate paths. These records show policymakers weighing persistent shelter and services inflation against emerging weakness in manufacturing orders. In contrast, the Bank for International Settlements' March 2026 Quarterly Review documents how private credit assets exceeding $2 trillion sit largely outside traditional regulatory perimeters, creating opacity that standard stress tests may miss - a dimension only briefly alluded to in the original coverage.

Multiple perspectives emerge on appropriate responses. One view, echoed in IMF staff papers on high-debt environments, holds that allowing controlled deleveraging could restore price discovery but risks amplifying downturns given current debt-to-GDP ratios above 120% for the non-financial corporate sector. Another perspective, reflected in statements from the European Central Bank and select Federal Reserve regional presidents, emphasizes the need for vigilance against unanchoring inflation expectations, particularly if geopolitical shocks such as Red Sea shipping disruptions or potential energy market volatility from Eastern European tensions drive commodity prices higher. These could simultaneously create stagflationary pressures: supply-side inflation alongside demand destruction.

What original coverage missed includes the potential for fiscal-monetary coordination through Treasury facilities, historical precedents in the 1970s where geopolitical oil shocks complicated Fed decisions, and the role of dollar dominance in exporting U.S. monetary conditions globally. BIS data further shows cross-border leverage channels that could transmit domestic stress to emerging markets, an international dimension absent from the initial analysis.

The current juncture thus presents no consensus solution. Hawkish voices prioritize credibility through sustained restrictive policy; dovish analyses warn of self-reinforcing deleveraging spirals. Primary communications from central banks consistently avoid endorsing either 'big print' liquidity injections or full hands-off approaches, instead stressing data dependence. This leaves the monetary framework exposed when simultaneous demands for stimulus and inflation control arise from geopolitical catalysts, revealing structural vulnerabilities built through successive cycles of intervention and low-rate leverage accumulation.

MERIDIAN: The Fed's constrained toolkit faces tests from potential geopolitical supply shocks that could demand opposing policy responses, likely exposing coordination gaps between monetary, fiscal, and international authorities in coming quarters.

Sources (3)

- [1]I'm Sorry, But The Fed Has Run Out Of Road(https://www.zerohedge.com/markets/im-sorry-fed-has-run-out-road)

- [2]FOMC Minutes - January 2026(https://www.federalreserve.gov/monetarypolicy/fomcminutes20260129.htm)

- [3]BIS Quarterly Review - Private Credit and Financial Stability(https://www.bis.org/publ/qtrpdf/r_qt2603.htm)