Inflation's Resurgence: Unpacking Stock Declines, Oil Surges, and Policy Shifts

Inflation’s return, driven by energy shocks and supply issues tied to Iran’s conflict, is shaking markets with declining stocks, rising oil prices ($101/barrel), and climbing Treasury yields. Beyond ZeroHedge’s coverage, this analysis explores overlooked geopolitical risks, policy dilemmas for the Fed, and global economic ripple effects, drawing on BLS, IEA, and EIA data to highlight structural challenges and historical parallels.

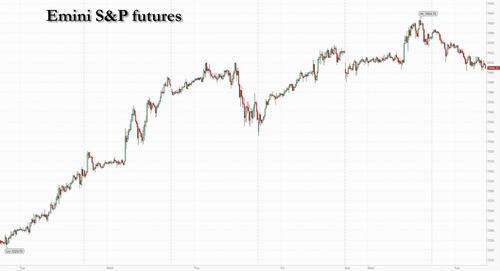

The recent spike in inflation, as evidenced by the April CPI data showing a higher-than-expected rise in core prices, has sent ripples through global markets, with U.S. equity futures declining (S&P down 0.2%, Nasdaq down 0.7%) and Treasury yields climbing to near their highest since March. Beyond the immediate market reactions reported by ZeroHedge, this resurgence of inflation—driven by energy price shocks tied to geopolitical tensions in Iran and persistent supply chain disruptions—signals deeper structural challenges. While ZeroHedge notes oil prices reaching $101 per barrel, it overlooks the broader context of OPEC+ production cuts and their role in sustaining high energy costs, as detailed in the International Energy Agency’s (IEA) latest Oil Market Report. This inflation spike is not merely a cyclical blip but a potential harbinger of sustained economic pressure that could force central banks, particularly the Federal Reserve, into a tighter monetary stance despite earlier signals of rate pauses.

ZeroHedge’s coverage misses critical geopolitical nuances, such as how the Iran conflict exacerbates energy market volatility beyond immediate supply disruptions. The U.S. Energy Information Administration (EIA) highlights that Iran’s role as a key oil producer, combined with sanctions and regional instability, creates a risk premium in oil pricing that could persist for quarters. This dynamic, underreported in the original piece, intersects with domestic U.S. policy debates over energy independence and renewable transitions, which remain sluggish amid inflationary pressures. Additionally, the tech sector’s underperformance—particularly the Mag 7 stocks’ premarket declines—reflects not just inflation fears but also sector-specific concerns like potential AI taxation in South Korea, a point ZeroHedge mentions but fails to connect to broader investor sentiment about regulatory risks in innovation hubs.

Synthesizing data from the Bureau of Labor Statistics (BLS) CPI report, which confirms a 0.4% month-over-month core inflation increase against a forecasted 0.3%, alongside the IEA’s warnings of tight oil supply through 2024, a pattern emerges: inflation is not a transient issue but a structural one tied to both exogenous shocks and policy inertia. The Federal Reserve’s upcoming decisions, hinted at through speakers like Chicago Fed’s Goolsbee, will likely grapple with balancing inflation control against recession risks—a tension ZeroHedge underplays. Investors, meanwhile, face a dual threat of rising rates eroding equity valuations and energy-driven cost pressures squeezing corporate margins, a dynamic evident in the mixed premarket performances of firms like Plug Power (up 7% on revenue beats) and Microvast Holdings (down 40% on misses).

Looking forward, the interplay between inflation and geopolitics could reshape monetary policy worldwide. Emerging markets, already strained by dollar strength amid U.S. rate hikes, may face capital outflows, while developed economies risk stagflation if growth stalls under tight policy. ZeroHedge’s snapshot of market declines misses this global ripple effect, which could redefine investor strategies toward defensive assets like gold—currently near $4,700/oz but under pressure—or energy-linked equities. The original coverage also lacks historical context: similar inflation-energy spirals in the 1970s led to aggressive Fed tightening, a precedent that looms large today as household debt levels, per the NY Fed’s upcoming report, remain elevated.

MERIDIAN: Inflation’s persistence, fueled by energy volatility, may push the Fed toward steeper rate hikes by Q3 2024, risking a sharper equity downturn but potentially stabilizing oil-driven price pressures if geopolitical tensions ease.

Sources (3)

- [1]Bureau of Labor Statistics - April CPI Report(https://www.bls.gov/news.release/cpi.nr0.htm)

- [2]International Energy Agency - Oil Market Report(https://www.iea.org/reports/oil-market-report)

- [3]U.S. Energy Information Administration - Iran Oil Market Analysis(https://www.eia.gov/international/analysis/country/IRN)