Historic 5% Yield on 30-Year Treasury Auction Signals Deepening Investor Fears of Inflation and Market Instability

The historic 5.046% yield on the 30-year Treasury auction, the first above 5% since 2007, signals deep investor concerns over inflation, Federal Reserve policy, and global bond market stress. Beyond ZeroHedge's focus on a quant crash parallel, this event reflects structural shifts in risk perception, with potential volatility looming for risk-parity funds and long-term debt demand.

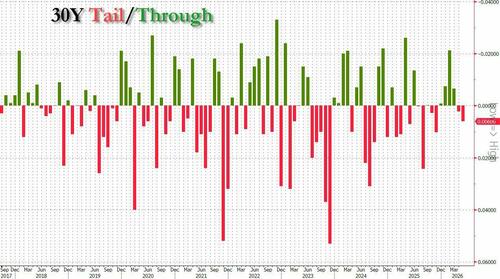

The recent 30-year Treasury auction, which marked a historic high yield of 5.046%—the first above 5% since August 2007—has sent ripples through financial markets, reigniting memories of the quant crash that preceded the Global Financial Crisis. As reported by ZeroHedge, the auction 'tailed' by 0.5 basis points, with a bid-to-cover ratio of 2.303, below the six-auction average of 2.43, signaling weakening demand. Beyond the surface-level 'ugliness' of the auction, this event reflects deeper investor anxieties about persistent inflation, rising debt levels, and the Federal Reserve's tightening policies, which are straining bond markets and echoing historical patterns of systemic stress.

ZeroHedge's coverage draws a direct line to the 2007 quant crash, a period when surging rates triggered a violent unwind of leveraged positions by quantitative funds, contributing to broader market turmoil. However, this comparison misses critical nuances. The 2007 crash was exacerbated by over-leveraged mortgage-backed securities and a lack of transparency in risk models—issues less pronounced today due to post-crisis regulatory reforms like Dodd-Frank. Instead, the current environment is shaped by different risks: a post-pandemic surge in inflation, geopolitical instability (e.g., the Russia-Ukraine conflict impacting energy prices), and a Federal Reserve balancing act between curbing inflation and avoiding recession. The Treasury yield's climb above 5% suggests markets are pricing in sustained higher rates, a trend corroborated by the U.S. Department of the Treasury's auction data, which shows consistent upward pressure on long-term yields since mid-2022.

What ZeroHedge underplays is the broader context of global bond market dynamics. The U.S. is not alone in facing yield spikes; European sovereign debt, such as German bunds, has seen similar pressures, with 10-year yields approaching 2.5% in 2023, per Bloomberg data. This synchronized rise in yields points to a global reassessment of risk amid central banks' hawkish stances. Moreover, the auction's weak demand (noted in the low bid-to-cover ratio) may reflect institutional investors shifting toward shorter-duration assets or alternative safe havens like gold, a pattern seen during past inflationary cycles. The Treasury's own reports indicate foreign investor participation (Indirects) at 66.6%, near average, suggesting that while demand isn't collapsing, confidence in long-term U.S. debt as a risk-free asset is fraying at the edges.

Another overlooked angle is the potential impact on quantitative strategies today. While ZeroHedge hints at struggling quants, it fails to connect this to the broader volatility in risk-parity funds, which balance equity and bond exposures. Rising yields disrupt these models, as bonds lose their traditional role as a hedge against equity downturns—a dynamic reminiscent of the 2007 VaR (Value at Risk) shocks but driven by different catalysts. If yields continue to climb, as hinted by the Fed's recent minutes signaling no immediate pivot to rate cuts, we could see forced deleveraging among these funds, amplifying market turbulence.

Synthesizing data from the U.S. Treasury, Federal Reserve minutes, and Bloomberg's global yield tracker, this auction is less a singular 'bubble-popping' event and more a symptom of a structural shift. Investors are grappling with a new regime of higher-for-longer rates, fiscal deficits (U.S. debt-to-GDP ratio nearing 120%, per Treasury data), and geopolitical wildcards. Unlike 2007, the crisis trigger may not be a quant meltdown but a slower, grinding erosion of confidence in sovereign debt as an anchor of stability. The coming months will test whether central banks can navigate this tightrope without sparking a broader sell-off.

MERIDIAN: If Treasury yields sustain above 5% in upcoming auctions, expect increased volatility in risk-parity funds and a potential shift by institutional investors toward shorter-duration assets or alternatives like gold.

Sources (3)

- [1]U.S. Department of the Treasury Auction Results(https://home.treasury.gov/resource-center/data-chart-center/quarterly-refunding/Documents/auctions.pdf)

- [2]Federal Reserve Minutes of the Federal Open Market Committee(https://www.federalreserve.gov/monetarypolicy/fomcminutes202310.htm)

- [3]Bloomberg Global Bond Yield Tracker(https://www.bloomberg.com/markets/rates-bonds/government-bonds/global)