S&P's Unyielding Index Rules Block $14BN Passive Inflows to SpaceX, Revealing How Methodological Gatekeeping Directs Trillions

S&P Dow Jones Indices rejected fast-track S&P 500 inclusion for mega-cap IPOs like SpaceX, preserving 12-month seasoning, profitability, and float rules. This delays billions in passive inflows and exposes how index methodologies silently channel trillions, creating tensions between benchmark quality and economic representativeness in an era of massive pre-IPO scaling.

S&P Dow Jones Indices has reaffirmed its strict eligibility criteria for the S&P 500 and related benchmarks, rejecting proposed exceptions for mega-cap IPOs that would have accelerated entry for companies like SpaceX, Anthropic, and OpenAI. The decision, announced after a public consultation, maintains the 12-month seasoning period, GAAP profitability requirements over the most recent quarter and trailing four quarters, and a minimum 10% public float. As a result, even at multi-trillion dollar valuations, these firms face at least a one-year delay before potential inclusion, pushing the earliest realistic entry for recently listed SpaceX to mid-2027 or later.[1][2]

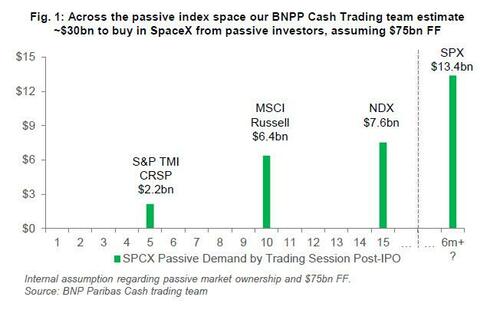

This outcome diverges from shifts by Nasdaq and FTSE Russell, which have embraced faster-track mechanisms for the largest new listings. Bloomberg reported that the move closes the door on rapid passive demand for SpaceX following what is described as the world's largest IPO, delaying an estimated $13-14 billion in mechanical inflows from S&P 500-tracking funds. Reuters noted the decision explicitly rejects size-based waivers, prioritizing 'core index principles' of consistency, financial viability, and investability over immediate representativeness.[3]

The lens here is rarely examined outside specialized finance circles: index methodology functions as invisible infrastructure directing trillions in passive capital. With passive strategies now dominating large swaths of equity ownership, a handful of index providers effectively act as allocators of 'dumb money' on an enormous scale. Inclusion triggers automatic buying by ETFs and mutual funds regardless of price or fundamentals, creating self-reinforcing liquidity and price support. By refusing to bend rules for pre-IPO mega-caps that scale to blue-chip size in private markets, S&P preserves a barrier against hype-driven volatility but risks rendering its benchmark less representative of the actual economy—particularly in high-growth sectors like space infrastructure and generative AI where profitability may lag due to heavy reinvestment.[4]

Deeper connections emerge when viewed against the evolution of public versus private markets. Companies can now remain private longer, achieving valuations once reserved for mature public firms, as seen in pre-IPO estimates for SpaceX exceeding $1.7 trillion. Earlier proposals, covered by The Wall Street Journal and Barron's in May 2026, floated shortening the seasoning period to six months and waiving profitability and float tests for the largest issuers precisely to address this gap. State Street Global Advisors analysis highlighted that without changes, S&P 500 inclusion for these names remains unlikely near-term, creating a divergence with broader indices and potentially leaving passive portfolios underweight transformative technologies. Critics of fast entry worried about embedding untested pricing and elevated volatility into core benchmarks; supporters argued exclusion distorts the 'market portfolio' that trillions benchmark against.[5][6]

This episode underscores a subtle power dynamic: index rules are not neutral technicalities but active shapers of capital flows, corporate behavior, and perceived market legitimacy. Firms may prioritize meeting GAAP profitability or expanding float over optimal R&D allocation to unlock index-driven demand. For everyday investors whose 401(k)s track the S&P 500, the decision means delayed exposure to some of America's most valuable and innovative enterprises. In a market where passive assets eclipse active management, these methodological choices—made by a small committee—quietly recalibrate where capital concentrates, often with larger real-world impact than many regulatory announcements. The S&P's adherence to tradition may safeguard benchmark integrity but highlights how arbitrary thresholds can postpone the integration of epoch-defining companies into the heart of institutional portfolios for years.

LIMINAL: S&P's refusal to update rules shows how a few index providers function as unelected directors of passive trillions, delaying mechanical buying pressure for AI and space leaders like SpaceX and potentially distorting what counts as the 'market' for millions of investors.

Sources (5)

- [1]SpaceX, Other Mega IPOs Denied Fast Index Entry by S&P(https://www.bloomberg.com/news/articles/2026-06-04/s-p-dow-jones-keeps-megacap-ipo-rules-as-is-after-consultation)

- [2]SpaceX blocked from early US benchmark index entry as S&P reaffirms existing rules(https://www.reuters.com/business/finance/sp-global-keeps-fast-entry-proposal-unchanged-spacex-listing-looms-2026-06-04/)

- [3]S&P Eyes Plan to Ease Index Rules With SpaceX IPO Looming(https://www.wsj.com/livecoverage/stock-market-today-dow-sp-500-nasdaq-05-01-2026/card/s-p-eyes-plan-to-ease-index-rules-with-spacex-ipo-looming-IGOu9L1zutkzsgc5nR0G)

- [4]Mega-cap IPOs: Implications for institutional investors and index managers(https://www.ssga.com/us/en/institutional/insights/mega-cap-ipos-implications-for-institutional-investors-and-index-managers)

- [5]S&P Is Thinking About Changing Its Rules for the S&P 500. What It Means for SpaceX, OpenAI(https://www.barrons.com/articles/sp500-spacex-ipo-openai-stocks-anthropic-c9e7699e)