Narrow Market Leadership Amplifies Volatility Risks Amid Evolving Policy and Geopolitical Pressures

Market concentration in tech heightens summer correction risks through overlooked policy and geopolitical channels, with balanced views on momentum sustainability versus external shocks.

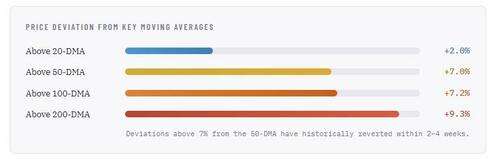

The concentration of S&P 500 gains in a handful of technology and semiconductor names, as detailed in recent market commentary, extends beyond simple technical deviations above moving averages. Historical patterns from prior cycles, including 2020-2021 and 1999-2000, show that such narrow breadth often coincides with inflection points triggered by external policy shifts rather than purely internal momentum exhaustion. Equal-weight indices lagging cap-weighted benchmarks by 200 basis points year-to-date reflect not just sector rotation but structural exposure to regulatory scrutiny on AI exports and supply-chain resilience. One perspective emphasizes the bull case of sustained primary trends supported by earnings growth in mega-cap leaders, drawing on primary Federal Reserve data showing resilient corporate balance sheets. A contrasting view highlights downside amplification from potential trade policy escalations affecting chip manufacturers, as seen in Commerce Department export control records from 2023 onward, which could unwind gamma-driven flows faster than oscillators like RSI or MACD predict. Coverage to date underplays these linkages to broader fiscal and monetary frameworks, such as upcoming Treasury issuance patterns and their interaction with concentrated equity holdings in institutional portfolios. Synthesizing primary index construction methodologies from S&P Dow Jones with volatility metrics from the Options Clearing Corporation reveals that single-stock implied volatility spikes may interact with cross-border investment restrictions to produce sharper mean reversions than domestic technical signals alone indicate. This setup underscores the need to monitor both domestic sector dispersion and international policy developments for a fuller risk assessment.

MERIDIAN: Narrow tech leadership in indexes could intersect with trade and regulatory policy shifts to accelerate pullbacks, particularly if export controls tighten further on semiconductor supply chains.

Sources (2)

- [1]S&P Dow Jones Indices Sector Weight Data(https://www.spglobal.com/spdji/en/)

- [2]Federal Reserve Statistical Release on Market Volatility(https://www.federalreserve.gov/releases/)