Inflation Expectations Surge to 3-Year High: Unpacking Economic Anxiety and Policy Implications

The NY Fed's April 2024 survey shows one-year inflation expectations spiking to 3.64%, a 3-year high, alongside deepening financial pessimism and fears of unemployment. Beyond the numbers, this signals potential stagflation risks, policy challenges for the Federal Reserve, and market volatility as global pressures and domestic labor trends converge.

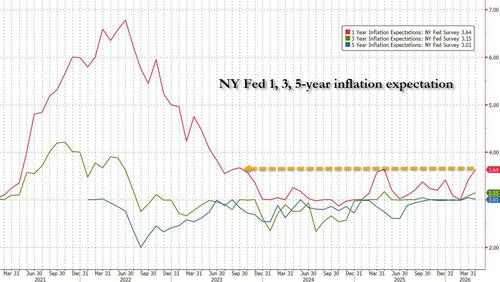

The New York Federal Reserve's latest Survey of Consumer Expectations, released in April 2024, reveals a significant uptick in one-year-ahead inflation expectations to 3.64%, the highest since September 2023, up from 3.42% in the prior month. While medium- and long-term expectations remain stable at 3.15% and 3.01% respectively, this short-term spike signals growing unease among consumers about near-term price pressures, even as specific commodity expectations like gas prices dropped sharply from 9.42% to 5.11%. Beyond the headline numbers, the survey uncovers deeper financial pessimism: 43.9% of respondents expect a higher unemployment rate in the next year, a record high since April 2025, while perceptions of current and future financial situations have worsened markedly. Credit access, both current and expected, is also perceived as tightening, compounding household anxiety. This data, originally reported by ZeroHedge, suggests an economy teetering on the edge of stagflation—a combination of stagnant growth and persistent inflation—that could force monetary policy into a delicate balancing act.

What the initial coverage missed is the broader context of how these inflation expectations interact with recent Federal Reserve actions and global economic trends. The Fed has maintained a hawkish stance on interest rates, with the federal funds rate held steady at 5.25-5.5% since mid-2023, as per their March 2024 meeting minutes. This rigidity aims to curb inflation but risks exacerbating the financial pessimism evident in the NY Fed survey, particularly as households report a declining expectation of income growth (down to 2.8%, a low since October 2025) against rising spending growth expectations (up to 5.4%). Historically, such a divergence often precedes reduced consumer spending, a key driver of U.S. GDP, potentially tipping the economy toward recession if not addressed.

Moreover, the survey’s findings must be read against global inflationary pressures. The International Monetary Fund’s April 2024 World Economic Outlook notes persistent supply chain disruptions and geopolitical tensions, particularly in the Middle East, as ongoing risks to price stability. These external factors likely amplify domestic inflation fears, a nuance absent from the ZeroHedge report. Domestically, the labor market data within the survey—such as the increased perceived probability of job loss (14.6%)—aligns with softening employment indicators reported by the Bureau of Labor Statistics, which showed nonfarm payroll growth slowing in recent months. This convergence suggests that consumer sentiment may be a leading indicator of a broader economic downturn, a connection not fully explored in the original article.

The critical question is whether the Federal Reserve will interpret this spike in short-term inflation expectations as a transient psychological response or a structural shift requiring tighter policy. Rising expectations for government debt growth (10.0%, the highest since June 2023) and tax increases (3.4%) in the survey hint at public skepticism about fiscal solutions, potentially limiting the Fed’s room to maneuver without spooking markets. Investors, already jittery from mixed economic signals, may pivot toward defensive assets if these expectations persist, a behavioral shift that could deepen market volatility in 2024. Unlike the original coverage, which focused narrowly on survey metrics, this analysis ties consumer sentiment to actionable policy and market outcomes, revealing a feedback loop of economic uncertainty that merits closer scrutiny.

MERIDIAN: Rising short-term inflation expectations could pressure the Federal Reserve to maintain or tighten rates, risking a slowdown. If consumer spending falters, a mild recession in late 2024 becomes more likely.

Sources (3)

- [1]Survey of Consumer Expectations, April 2024(https://www.newyorkfed.org/microeconomics/sce)

- [2]Federal Reserve March 2024 Meeting Minutes(https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20240320.pdf)

- [3]IMF World Economic Outlook, April 2024(https://www.imf.org/en/Publications/WEO/Issues/2024/04/16/world-economic-outlook-april-2024)