China and India Lead Accelerating Nuclear Renaissance to Fuel AI Boom and Decarbonization

China has reached ~125 GW nuclear capacity with aggressive expansion plans, while India's 2025 SHANTI Act and SMR program open the sector to private investment explicitly for AI data centers. This underreported renaissance addresses AI-driven electricity demand projected to approach 1,000 TWh by 2030 and supports global decarbonization, positioning Asia for energy and technological leadership per Bloomberg, Brookings, IEA, and industry analyses.

While mainstream coverage often focuses on AI model breakthroughs and semiconductor races, a quieter but more foundational shift is underway: an accelerating global nuclear renaissance disproportionately led by China and India. This buildout addresses the explosive, 24/7 electricity demands of hyperscale data centers while advancing decarbonization—connections frequently missed amid broader climate and tech narratives.

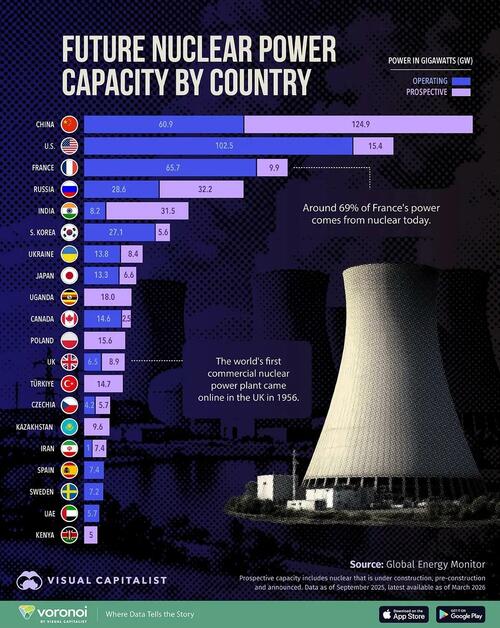

Recent data underscores the scale. China's installed nuclear capacity has reached approximately 125 GW, placing it at the global forefront with 60 operational units and 36 under construction—more than half the world's total reactors being built. Chinese authorities project further rapid growth, targeting 110 GW by 2030 per five-year planning and up to 200 GW by 2040, with seven new reactors slated for commercial operation in 2026 alone.[1][2] This trajectory aligns with earlier projections that China could surpass the United States (currently around 100+ GW) and dominate long-term capacity, potentially reaching 180+ GW with all planned projects realized.

India, traditionally more cautious, is undergoing a structural pivot. The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India (SHANTI) Act of 2025 dismantles the state monopoly, enabling private participation, public-private partnerships, and up to 49% foreign direct investment. A substantial budget allocation supports deploying five Bharat Small Modular Reactors (SMRs) by 2033, explicitly tied to co-locating with AI data center parks for captive, carbon-free baseload power. Major players are responding: Microsoft has committed $17.5 billion to Indian AI and data center infrastructure, while the Adani Group is exploring nuclear plants to underpin its $100 billion AI data center ambitions. Similar moves by Google, Amazon, and Reliance highlight how nuclear policy reform is unlocking energy for India's AI push.[3]

The deeper connection lies in AI's insatiable energy appetite. Global data center electricity use hit ~415 TWh in 2024 and is projected to reach 945–1,200 TWh by 2030–2035, driven largely by inference workloads that now dominate consumption. AI-optimized facilities can require 2–4 times the power of traditional servers, with single queries consuming measurable watt-hours at massive scale. Renewables alone struggle with intermittency and grid constraints; nuclear's ~93% capacity factor offers unmatched reliability for hyperscalers seeking gigawatts of firm, low-carbon power. Brookings notes this is already spurring restarts and direct nuclear deals in the US and France, yet China and India are moving fastest on new builds.[4]

This renaissance—centered on mature fission technologies, evolving SMR designs for factory production and co-location, and supportive policies—ties directly to international commitments like the goal of tripling global nuclear capacity by 2050, which China has endorsed. The IEA highlights innovation in SMRs, new financing models, and policy support as critical to a "new era" for nuclear amid rising electricity demand from data centers and electrification.[5]

Geopolitically, the implications are profound and underreported. Asian leadership in nuclear deployment reduces fossil fuel import dependence, bolsters energy security, and creates advantages in the AI economy where reliable power equals computational dominance. Western regulatory hurdles and slower permitting contrast sharply with China's construction pace and India's recent liberalization. While safety records remain strong and waste management evolves, the missed narrative is how this shift could reshape uranium markets, supply chains, and even tech investment flows toward nations mastering both AI and its atomic backbone. Fusion remains a longer-term prospect, but scaled fission is here now—powering the digital future that mainstream outlets have yet to fully connect.

[LIMINAL]: Asia-led nuclear expansion will anchor AI supremacy and energy independence for China and India, exposing Western regulatory lag and reordering global power dynamics around firm, carbon-free baseload as the foundation of technological and climate leadership.

Sources (6)

- [1]China's installed nuclear power capacity hits 125mln kW, ranks first globally(https://www.globaltimes.cn/page/202604/1359130.shtml)

- [2]China Keeps Pushing Nuclear Power With Ambitious Growth Target(https://www.bloomberg.com/news/articles/2026-03-09/china-keeps-pushing-nuclear-power-with-ambitious-growth-target)

- [3]Global energy demands within the AI regulatory landscape(https://www.brookings.edu/articles/global-energy-demands-within-the-ai-regulatory-landscape/)

- [4]Pairing India's AI Infrastructure with Nuclear Power(https://www.nuclearbusiness-platform.com/media/insights/india-ai-infrastructure-with-nuclear)

- [5]The Path to a New Era for Nuclear Energy(https://www.iea.org/reports/the-path-to-a-new-era-for-nuclear-energy)

- [6]China and Brazil among new signatories to tripling nuclear goal(https://www.world-nuclear-news.org/articles/china-and-brazil-sign-up-to-tripling-nuclear-goal)