Unpacking the 'Stunning Quarter': What Lies Beneath the Highest Earnings Growth in Two Decades

US Q1 earnings growth of 24.6%, the highest in over two decades, reflects corporate strength driven by AI, pricing power, and commodity prices. However, this analysis uncovers risks like overvaluation, geopolitical volatility, and uneven sectoral gains, questioning the sustainability of this rebound amidst global market dynamics.

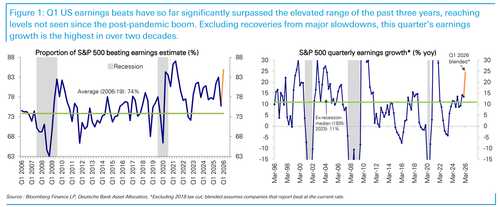

The recent report from Deutsche Bank, highlighted by ZeroHedge, labels the US Q1 earnings season as a 'stunning quarter,' with S&P 500 earnings growth projected at 24.6%, a level not seen in over two decades outside post-shock recoveries. This figure, surpassing the 13.4% growth of Q4, is driven by widespread sectoral strength, with all 11 S&P sectors posting positive growth for the first time in four years. While the AI boom is a noted catalyst, broader factors such as supply constraints, higher pricing power, and commodity price surges also contribute. Deutsche Bank has subsequently raised its 2026 EPS forecast from $320 to $342, signaling confidence in sustained corporate performance. However, this analysis aims to go beyond the surface-level exuberance, examining the underlying drivers, overlooked risks, and broader geopolitical and economic contexts that shape this narrative.

First, the earnings growth must be contextualized within a post-pandemic economic landscape where pent-up demand and stimulus-driven liquidity have bolstered corporate balance sheets. The AI value chain's surge, while significant, masks disparities across sectors. For instance, tech and mega-cap growth (MCG) stocks have disproportionately driven the headline figures, potentially skewing perceptions of uniform strength. According to data from the U.S. Bureau of Economic Analysis, real GDP growth in Q1 2024 was a more modest 1.6% annualized, suggesting that corporate earnings are outpacing broader economic expansion—a potential indicator of unsustainable growth or inflationary pressures.

Second, the original coverage underplays the role of geopolitical volatility, particularly the Iran conflict's impact on oil and commodity prices, which Deutsche Bank itself notes as a driver of revised EPS forecasts. Higher input costs may have bolstered revenues for energy and materials sectors, but they also risk squeezing margins for consumer-facing industries if sustained. The International Energy Agency’s (IEA) April 2024 Oil Market Report warns of potential supply disruptions in the Middle East, which could further elevate costs and challenge the durability of this earnings boom.

Third, the narrative of 'growing into high valuations' overlooks the persistent risk of overvaluation in the US equity market. While earnings growth mitigates some concerns, the S&P 500’s forward P/E ratio remains elevated at approximately 20.5, compared to a historical average closer to 15, per data from FactSet. This suggests that even robust earnings may not fully justify current market pricing, especially if macroeconomic headwinds like interest rate hikes or geopolitical shocks materialize. The Federal Reserve’s minutes from its March 2024 meeting indicate a cautious stance on inflation, with potential rate increases still on the table, which could dampen investor sentiment and corporate borrowing.

Finally, the comparison to other global markets, as noted by Deutsche Bank, reveals a nuanced picture. While US equities have moved from the bottom quartile to the middle of the global pack since the Iran conflict's onset, markets in Europe and Asia have shown stronger relative performance over the past 18 months. This raises questions about whether the US corporate rebound is as exceptional as portrayed, or if it merely reflects a catch-up to global trends amplified by unique factors like AI investment.

In sum, while the Q1 earnings growth signals a robust corporate sector, it also unearths concerns about sustainability amidst geopolitical risks, inflationary pressures, and valuation challenges. The interplay between these factors will likely shape whether this 'stunning quarter' marks a lasting rally or a fleeting peak.

MERIDIAN: The current earnings boom may fuel short-term market optimism, but sustained geopolitical tensions and potential rate hikes could cap gains by late 2024.

Sources (3)

- [1]Deutsche Bank Thematic Research: The Great 2026 Reset(https://www.zerohedge.com/markets/stunning-quarter-highest-earnings-growth-over-two-decades)

- [2]International Energy Agency: Oil Market Report April 2024(https://www.iea.org/reports/oil-market-report-april-2024)

- [3]Federal Reserve Minutes of the Federal Open Market Committee, March 2024(https://www.federalreserve.gov/monetarypolicy/fomcminutes20240320.htm)