Treasury's $189 Billion Borrowing Hike Signals Deepening Fiscal Pressures Amid Rising Debt and Policy Uncertainty

The U.S. Treasury's raised borrowing estimate of $189 billion for the current quarter, up $80 billion, reflects deepening fiscal pressures amid rising national debt and interest costs. Beyond market impacts, this signals structural deficits, geopolitical strains, and political risks, highlighting a narrowing fiscal runway.

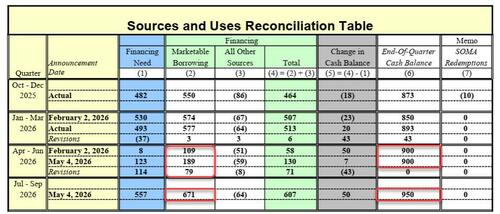

The U.S. Department of the Treasury's announcement of a revised quarterly borrowing estimate of $189 billion for the current quarter, up $80 billion from the February forecast of $109 billion, underscores mounting fiscal challenges as the nation grapples with lower-than-expected cash flows and a persistent structural deficit. This adjustment, driven primarily by reduced tax receipts and only partially offset by a higher starting cash balance of $893 billion, reflects broader patterns of increasing national debt—now exceeding $34 trillion as of early 2026—and the growing burden of interest payments, which consumed over 15% of federal spending in FY2025 per Congressional Budget Office (CBO) projections.

While the original coverage by ZeroHedge highlights the raw numbers and immediate market implications, it misses critical contextual links to long-term fiscal sustainability and geopolitical pressures. First, the Treasury's borrowing surge aligns with a historical pattern of escalating third-quarter needs, as evidenced by borrowings of $1.058 trillion in Q3 2025 and $1.01 trillion in Q3 2023. However, this hike occurs against a backdrop of rising interest rates, with the Federal Reserve's ongoing efforts to curb inflation potentially pushing yields on Treasury securities higher. The CBO's February 2026 report projects that net interest costs could reach $1.2 trillion annually by 2030 if current borrowing trends persist, squeezing discretionary spending and amplifying risks of a debt spiral.

Second, the announcement's timing—preceding the Quarterly Refunding Announcement—obscures a critical policy debate overlooked in initial reporting: the interplay between domestic borrowing and international economic commitments. The Treasury's potential reliance on increased bill issuance to cover obligations like the $175 billion in IEEPA tariff repayments over the next three years, as noted by Deutsche Bank, could strain short-term liquidity in global markets. This is particularly relevant given recent geopolitical tensions, including U.S.-China trade disputes and Middle East instability, which have historically influenced Treasury yields and foreign holdings of U.S. debt (down to 22% of total debt in 2025 per Treasury International Capital data).

Third, the original coverage underplays the political dimension. With FY2026 deficits projected at $2.068 trillion under Deutsche Bank's base case—and potentially $200 billion higher if defense budgets expand—Congressional gridlock over debt ceiling negotiations looms large. Historical precedent, such as the 2011 and 2023 debt ceiling crises, suggests that partisan brinkmanship could exacerbate market volatility, a factor absent from the initial analysis.

Synthesizing sources beyond the primary announcement, the Treasury's own 'Marketable Borrowing Estimates' (February 2026) reveal a consistent underestimation of cash flow shortfalls, suggesting systemic forecasting challenges. Meanwhile, the CBO's 'Budget and Economic Outlook: 2026-2036' warns of a debt-to-GDP ratio approaching 120% by decade's end, a threshold associated with reduced economic flexibility in crises. These data points, combined with Deutsche Bank's deficit scenarios, indicate that the Treasury's borrowing hike is not a mere quarterly adjustment but a symptom of structural imbalances that could constrain U.S. policy options—domestically and abroad—in the face of unforeseen shocks.

Ultimately, the $189 billion figure is less about immediate market reactions and more about what it portends: a narrowing fiscal runway as interest costs, geopolitical obligations, and political dysfunction converge. The Treasury's ability to manage this trajectory without triggering higher borrowing costs or crowding out private investment remains an open question, one that markets and policymakers alike must confront beyond the scope of quarterly refunding previews.

MERIDIAN: The Treasury's borrowing hike may pressure bond yields upward in the short term, with a potential 10-year Treasury yield increase of 20-30 basis points by Q3 2026 if geopolitical or political risks materialize.

Sources (3)

- [1]Treasury Marketable Borrowing Estimates, February 2026(https://home.treasury.gov/policy-issues/financing-the-government/quarterly-refunding/marketable-borrowing-estimates)

- [2]CBO Budget and Economic Outlook: 2026-2036(https://www.cbo.gov/publication/59711)

- [3]Treasury International Capital (TIC) Data, 2025(https://home.treasury.gov/data/treasury-international-capital-tic-system)