Iran Oil Disruptions: Weighing Recessionary Risks Against Economic Resilience in Historical Context

Historical oil shocks analyzed against current Iran-related price spikes reveal recession risks tied to duration, inflation backdrop, and Fed responses; multiple viewpoints presented using primary economic research while noting what initial reporting overlooked.

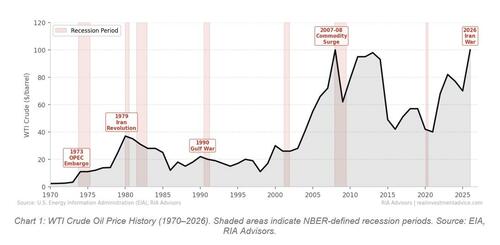

The recent spike in Brent crude prices, rising over 60% following U.S. and Israeli strikes on Iran that began in late February, has renewed debates about the transmission of geopolitical shocks to the real economy. While the original ZeroHedge analysis by Lance Roberts correctly highlights the repeating pattern of investors mislearning lessons from prior oil crises, it underplays the evolving structural factors in global energy markets and over-relies on a simplified historical taxonomy without sufficiently integrating primary data from the U.S. Energy Information Administration (EIA) and Federal Reserve research on monetary policy transmission.

Primary documents, including James Hamilton's seminal 1983 paper 'Oil and the Macroeconomy Since World War II' (Journal of Political Economy), establish that oil price increases of the magnitude seen in 1973 and 1979 correlated with U.S. recessions, but Hamilton's later updates emphasize that the key mechanism is not the nominal price but the disruption to consumer and business expectations. A 2021 Federal Reserve Board working paper further nuances this by showing no mechanical link between net oil price increases and recessions when controlling for monetary policy responses, a point the source article references but does not fully explore in the current Iran context.

Multiple perspectives emerge on the current situation. One view, drawing from 1970s patterns, warns of recessionary risks as higher energy costs feed into broader inflation, potentially forcing the Federal Reserve to maintain restrictive policy longer than markets currently anticipate. With CPI components already showing sticky shelter and services inflation, a sustained oil shock above $100 per barrel could re-anchor inflation expectations higher, complicating the Fed's dual mandate. This connects directly to energy prices influencing transportation, manufacturing, and household budgets, echoing the stagflation risks Roberts flags though current data does not yet meet the technical definition.

An alternative perspective points to post-2010 developments: the U.S. as a net petroleum exporter since 2019 (per EIA monthly data) provides a buffer absent in the 1970s, while strategic petroleum reserves and diversified supply chains from the shale revolution may limit duration. The 1990 Gulf War, where prices spiked 75% but normalized within months, is cited as precedent for contained impacts, with the S&P 500 recovering swiftly. Recent IMF analysis of the 2022 Russia-Ukraine shock similarly found muted global GDP effects due to substitution effects and fiscal responses, though it noted uneven impacts on emerging markets.

What the original coverage missed includes the interplay with current Fed policy expectations: futures markets are pricing in rate cuts by mid-year, but an oil-driven inflation rebound could delay this, tightening financial conditions via higher yields. Patterns from the 2008 episode show how oil shocks amplify existing fragilities rather than acting in isolation. The source also under-analyzes demand-side dynamics, as slowing Chinese industrial activity documented in official NBS data could offset some supply-driven price pressure. Ultimately, outcomes hinge on disruption persistence, pre-shock inflation levels, and central bank credibility, variables that require monitoring primary EIA export/import figures and FOMC meeting transcripts rather than headline narratives alone.

MERIDIAN: Current oil price surges from Iran tensions could pressure Fed rate paths and inflation expectations, though U.S. export status and market adaptations offer potential offsets depending on how long disruptions persist.

Sources (3)

- [1]Oil Shocks & Recessionary Outcomes(https://www.zerohedge.com/markets/oil-shocks-recessionary-outcomes)

- [2]Oil and the Macroeconomy Since World War II(https://www.jstor.org/stable/1803493)

- [3]The Macroeconomic Effects of Oil Supply Shocks(https://www.federalreserve.gov/pubs/feds/2021/202101/202101pap.pdf)