China's Structural Oil Demand Decline: EVs, Economic Shifts, and Geopolitical Stress Test Reveal Durable Global Energy Transition

Corroborated reporting confirms China's oil demand weakness stems from EVs, slower growth, and policy shifts, not just the 2026 supply shock. This points to earlier peak demand with lasting effects on global markets and energy transitions.

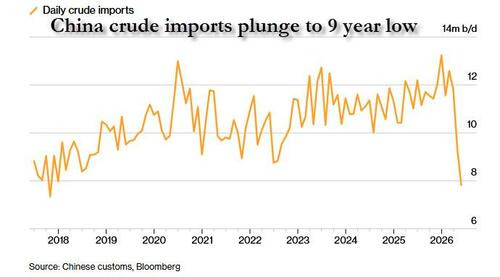

China's apparent ability to weather the 2026 Iran conflict-driven oil supply shock with sharply lower imports underscores a deeper, structural reduction in oil intensity that predates the crisis. Customs data confirm May 2026 crude imports fell 29% year-over-year to 7.8 million barrels per day (mb/d), the lowest level since October 2017, as Beijing drew on massive stockpiles amid Strait of Hormuz disruptions rather than chasing expensive spot cargoes.[1][2]

Sinopec, China's largest refiner, reported notable weakness in refined product sales. First-quarter 2025 domestic fuel sales declined 5.3%, with full-year 2025 gasoline sales down 2.5% and diesel 9.1%, reflecting both electrification and subdued economic activity, particularly in construction.[3][4] Goldman Sachs analysts have linked recent Chinese fuel demand destruction—potentially as high as 20% in some segments—to the combined effects of high prices and structural change.[5]

The shift is amplified by rapid EV adoption. China accounted for the majority of global electric car sales growth in 2025, with EVs nearing 55% of new car sales; charging volumes and infrastructure expanded dramatically, reaching over 21 million total piles by early 2026.[6][7] Public transport gains and a prolonged property sector downturn have further eroded diesel demand from trucking and construction.

IEA analysis shows China's oil-based fuel consumption had already plateaued or declined modestly pre-crisis, with 2024 volumes below 2021 levels despite economic size.[8] This suggests the current import collapse is not solely crisis-driven but reveals a durable drop in oil intensity. Consequences include reduced leverage for producers facing lower baseline demand, potential price suppression from sustained demand destruction, and accelerated global transition timelines as China demonstrates that high EV penetration can decouple economic activity from liquid fuels faster than models predicted.

[Energy Aspects / IEA analysts]: China's oil demand may have already peaked or will do so by 2025-2026, forcing downward revisions to global long-term demand forecasts and pressuring OPEC+ output strategies.

Sources (5)

- [1]Bloomberg(https://www.bloomberg.com/news/articles/2026-06-09/china-s-oil-imports-plunge-to-eight-year-low-on-war-disruptions)

- [2]Reuters(https://www.reuters.com/sustainability/climate-energy/sinopecs-quarterly-net-income-falls-28-slower-fuel-sales-2025-04-28/)

- [3]IEA Global EV Outlook 2026(https://www.iea.org/reports/global-ev-outlook-2026/executive-summary)

- [4]Energy Aspects via Anadolu Agency(https://www.aa.com.tr/en/energy/oil/china-oil-imports-set-to-decline-in-april-amid-hormuz-disruption/56549)

- [5]MarineLink / Customs Data(https://www.marinelink.com/news/china-oil-imports-collapse-down-540141)