Unmasking Economic Vulnerabilities: Oil Prices as Harbingers of Recession Risk

This analysis connects oil price volatility to inflation and recession risks, synthesizing historical research, IMF outlooks, and current geopolitical factors to reveal macro vulnerabilities and self-reinforcing debt cycles often missed in Fed-centric narratives.

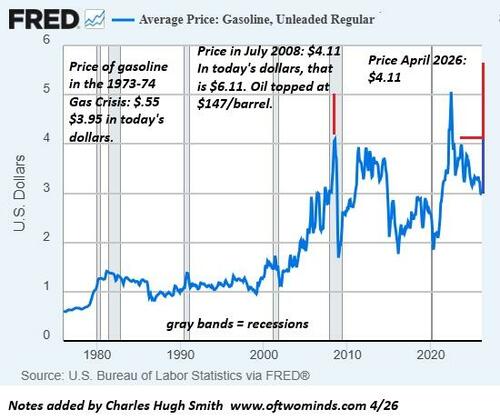

While mainstream economic commentary remains fixated on Federal Reserve interest rate decisions and prospects of a 'soft landing,' the interplay between oil prices, inflation, and underlying economic vulnerabilities presents a more consequential picture of risks that could define the next cycle. Charles Hugh Smith's analysis on ZeroHedge correctly identifies that recessions rarely require a specific oil price spike; rather, they emerge when optimistic narratives of permanent growth, rising corporate profits, strong employment, and healthy household balance sheets collide with reality. Inflation quietly diverts earnings toward essentials, prompting more borrowing that eventually leads to retrenchment. Credit-asset bubbles sustain the 'wealth effect' without requiring deferred consumption, yet both debt accumulation and speculative manias are self-liquidating.

Smith's account captures these demand-side dynamics and the role of suspended disbelief in sustaining consumption. However, original coverage underplays supply-side geopolitical triggers, historical econometric evidence, and current macro patterns visible in primary sources. James D. Hamilton's NBER paper 'Causes and Consequences of the Oil Shock of 2007-08' (2009) demonstrates through statistical analysis that exogenous oil supply disruptions preceded nearly every U.S. recession since World War II, operating via reduced consumer spending power and policy dilemmas that amplify contraction. Similarly, the IMF's World Economic Outlook (October 2023) documents how energy price volatility drives divergent inflation outcomes: cost-push effects in advanced economies versus growth drags in import-dependent emerging markets.

What much coverage misses is the post-pandemic context of record global debt levels (per BIS quarterly reviews) layered atop supply-chain fragilities exposed by COVID disruptions and the Russia-Ukraine conflict's lasting impact on European energy markets. OPEC+ production cuts, Red Sea shipping attacks, and Middle East tensions represent primary risk factors not fully synthesized in happy-story consumer-spending statistics. U.S. Energy Information Administration petroleum status reports show that while domestic shale has provided a buffer, it has not eliminated global price transmission into CPI components such as transport and plastics—core inputs for 'green' technologies and data centers alike.

Multiple perspectives emerge from primary documents. Supply-side analysts cite EIA drilling productivity data suggesting market adaptation can cap price spikes. Demand-side and heterodox views, aligned with Hamilton, emphasize that oil acts as an implicit tax, eroding discretionary income faster than hedonic adjustments in official inflation metrics can conceal. The critical macro pattern beyond standard Fed-focused coverage is the compounding feedback: sustained oil above $80-90 per barrel accelerates the decay of confidence Smith describes, simultaneously pressuring central banks to maintain higher rates longer while exposing over-indebted households and firms. This differs from 1970s stagflation only in today's elevated leverage ratios; asset bubbles in equities and housing become especially brittle when energy costs undermine the very earnings needed to service debt.

Synthesizing these sources reveals the next economic cycle may be shaped less by monetary fine-tuning than by whether energy price shocks uncloak the extent to which recent growth rested on deferred realities rather than sustainable productivity. Neither pure optimism of technological deliverance nor fatalism is warranted; primary data instead point to heightened recession risk when oil volatility intersects with pre-existing financial imbalances.

MERIDIAN: Sustained oil above $85-90 per barrel will compound inflation and erode confidence in debt-fueled growth narratives faster than Fed rate adjustments can offset, raising the probability of a policy-induced recession by late 2024 if supply shocks materialize.

Sources (3)

- [1]Oil, Inflation, & Recession(https://www.zerohedge.com/personal-finance/oil-inflation-recession)

- [2]Causes and Consequences of the Oil Shock of 2007-08(https://www.nber.org/papers/w15002)

- [3]World Economic Outlook, October 2023(https://www.imf.org/en/Publications/WEO/Issues/2023/10/10/world-economic-outlook-october-2023)