Japan's Supplementary Budget Push Exposes Structural Fiscal Vulnerabilities Amid Middle East Energy Shocks

Japan's extra budget for fuel subsidies amid Middle East-driven energy costs strains an already elevated debt burden, with potential transmission effects on global yields that prior coverage underemphasized.

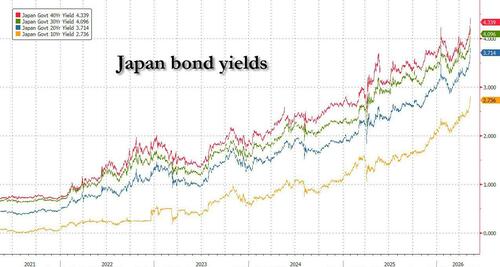

Japan's decision to compile a supplementary budget for gasoline and utility subsidies, as outlined in recent statements from Prime Minister Sanae Takaichi, intersects with longstanding patterns of debt accumulation that trace back to the Bank of Japan's yield curve control framework initiated in the 2010s. Primary documents from the Ministry of Finance highlight cumulative general account deficits exceeding 200 percent of GDP, a metric reinforced in annual budget white papers rather than secondary interpretations. This approach draws parallels to prior interventions during the 2011 Fukushima crisis and 2022 global energy spikes, where short-term relief measures deferred structural adjustments. One perspective emphasizes the necessity of shielding import-dependent households from oil price volatility tied to Middle East conflicts, citing Japan's reliance on regional crude supplies documented in trade statistics from the Ministry of Economy, Trade and Industry. An alternative view, reflected in opposition proposals such as those from Yuichiro Tamaki, questions the sustainability of additional issuance without corresponding revenue measures, potentially accelerating the 10-year JGB yield climb observed since October 1996. Markets appear to have overlooked linkages to yen carry trade dynamics, where sustained low-rate differentials could transmit pressure to U.S. Treasury yields through cross-border capital flows, a connection evident in coordinated G7 finance discussions rather than isolated domestic reporting. These developments underscore trade-offs between immediate economic stabilization and long-term debt trajectory management without endorsing specific policy paths.

MERIDIAN: Japan's supplementary budget issuance could sustain upward pressure on JGB yields, with secondary effects on global carry trades that warrant monitoring in upcoming central bank coordination.

Sources (3)

- [1]Ministry of Finance Japan Annual Budget Documents(https://www.mof.go.jp/english/budget/budget/index.htm)

- [2]Bank of Japan Monetary Policy Meeting Minutes(https://www.boj.or.jp/en/mopo/mpmdeci/index.htm)

- [3]G7 Finance Ministers Statement on Economic Risks(https://www.mof.go.jp/english/international_policy/convention/g7/index.htm)