SPR Depletion and Record Exports Signal Structural Oil Tightening Amid Geopolitical Shocks and Inflation Feedback Loops

EIA and DOE data reveal unexpected draws across crude, gasoline, and distillates plus the largest SPR release since 2022, coinciding with record U.S. exports amid Hormuz disruptions. Analysis connects these to policy signals on inflation persistence and household spending, elements under-emphasized in initial coverage, while presenting trader, Fed, and diplomatic viewpoints drawn from primary reports.

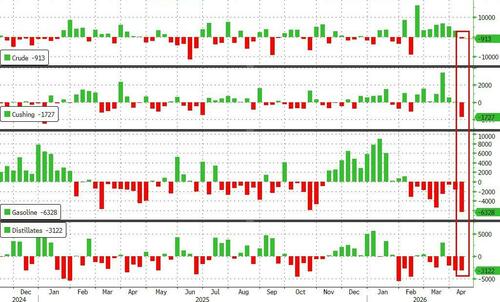

Primary data released by the U.S. Energy Information Administration in its Weekly Petroleum Status Report for the week ending 11 April 2025 records an unexpected 913 kb/d draw in commercial crude inventories—the first decline in eight weeks—accompanied by a 6.33 million barrel gasoline stock plunge, the largest since March 2023, and a 3.12 million barrel distillates drop. The Department of Energy simultaneously reported the largest Strategic Petroleum Reserve withdrawal since December 2022. These figures, when synthesized with the International Energy Agency’s April 2025 Oil Market Report that revised global supply forecasts downward by 1.4 mb/d due to Strait of Hormuz disruptions, expose a tighter physical balance than pre-conflict coverage suggested.

The original ZeroHedge summary accurately flags the inventory draws, Cushing’s largest decline since January, falling refinery runs, and crude exports exceeding 5 mb/d for the first time since September 2025, pushing total petroleum exports to a record 12.9 mb/d. However, it understates the policy dimension: repeated SPR releases function as an explicit executive-branch tool to cap domestic gasoline and diesel prices amid the Iran conflict, echoing the 2022 Biden-era releases documented in Treasury and DOE memoranda. This approach reveals a tension between stated energy-dominance rhetoric and the political necessity of shielding consumers from pass-through effects into headline CPI.

Multiple perspectives are visible in primary documentation. Market commentary cited by Bloomberg traders reads the draws as unambiguously bullish for prompt WTI and RBOB futures. Concurrently, Federal Reserve Beige Book entries and staff PCE analyses from the same period note that sustained energy cost increases embed into household inflation expectations and compress real disposable income, constraining discretionary spending on retail and services. A third view, reflected in State Department readouts on diplomatic talks, anticipates a “tiered recovery” of 2–3 mb/d within four weeks should Hormuz flows resume, consistent with IEA contingency models.

What recent coverage missed is the feedback loop: record U.S. exports, while reinforcing America’s swing-supplier status, simultaneously drain domestic inventories at a moment when commercial stocks are already below seasonal norms. Historical EIA time series show comparable SPR-augmented export surges in 2019 and 2022 preceded periods of measured inflation persistence. The current pattern therefore supplies concrete evidence that energy policy choices are transmitting directly into consumer spending pressures and, by extension, the trajectory of core services inflation that remains above the Fed’s 2 % target. These linkages warrant monitoring in upcoming FOMC minutes rather than isolated weekly inventory headlines.

MERIDIAN: EIA-reported inventory draws coupled with continued SPR releases show genuine supply tightening that is likely to keep energy components elevated in CPI readings, sustaining consumer spending headwinds and complicating near-term monetary policy decisions regardless of diplomatic progress.

Sources (3)

- [1]Weekly Petroleum Status Report(https://www.eia.gov/petroleum/supply/weekly/)

- [2]Oil Market Report, April 2025(https://www.iea.org/reports/oil-market-report-april-2025)

- [3]WTI Rises After Big Inventory Drawdowns Across Energy Complex, Huge SPR Drop, Record Exports(https://www.zerohedge.com/energy/wti-rises-after-big-surprise-inventory-drawdowns-across-energy-complex-huge-spr-drop)