Nuclear Renaissance: SMRs and Uranium Deficits Reshape Global Energy Markets

Goldman Sachs' latest nuclear forecast highlights a buildout of large-scale reactors and SMRs, projecting a 17% uranium demand increase by 2045. This analysis digs deeper into geopolitical supply risks, policy gaps, and tech-driven energy demands, revealing overlooked challenges and market dynamics shaping the nuclear renaissance.

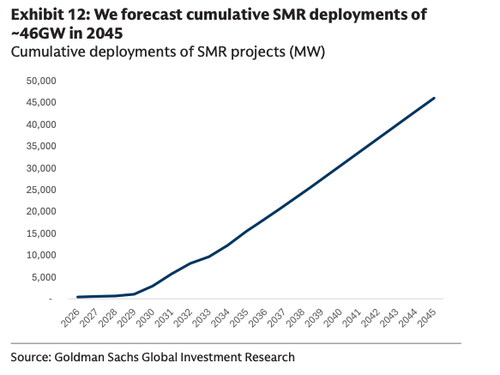

The recent acceleration of nuclear power buildouts, as highlighted in Goldman Sachs' latest 'Nuclear Nuggets: Global Reactor Tracker,' marks a critical pivot in global energy markets toward sustainable, reliable power sources amid intensifying decarbonization pressures. Beyond the report's focus on North American reactor progress and the inclusion of small modular reactors (SMRs) in uranium demand forecasts, this development signals deeper geopolitical and economic undercurrents that warrant scrutiny. Goldman's forecast of 46 GW of SMR capacity by 2045, driving a 17% increase in uranium demand (62 million pounds), only scratches the surface of a broader transformation. This article examines overlooked dimensions of this nuclear renaissance, including geopolitical supply chain risks, policy misalignments, and the intersection of nuclear energy with emerging tech-driven power demands.

First, while Goldman notes a looming uranium supply deficit of 2.3 billion pounds between 2025 and 2045, it underplays the geopolitical fragility of uranium supply chains. Roughly 40% of global uranium production comes from Kazakhstan, a nation navigating complex relations with Russia and China, both of whom exert influence over Central Asian resources. The U.S. and EU, key drivers of nuclear expansion, remain heavily reliant on imports, with the U.S. sourcing over 90% of its uranium from foreign markets as of 2022, per the U.S. Energy Information Administration (EIA). Recent legislative moves, such as the U.S. Senate's May 2024 passage of a ban on Russian uranium imports (H.R.1042), aim to reduce dependency but risk short-term supply shocks absent domestic capacity ramp-up. Goldman's analysis misses how these geopolitical fault lines could exacerbate price volatility beyond the projected stabilization in the $80-90 per pound range.

Second, the inclusion of SMRs in Goldman's forecast, while forward-looking, glosses over significant policy and technical hurdles. SMRs, touted for their scalability and lower upfront costs, remain largely unproven at commercial scale. The U.S. Nuclear Regulatory Commission's (NRC) approval of NuScale Power’s design in 2023 was a milestone, but subsequent project delays—such as the cancellation of a planned Idaho SMR project in November 2023 due to cost overruns—highlight persistent financial risks. Moreover, regulatory frameworks across jurisdictions are inconsistent; Canada’s collaboration between Bruce Power and SaskPower, as noted by Goldman, is promising, but federal-provincial alignment on nuclear strategy remains uneven in other regions. This gap could delay SMR deployment timelines, a factor Goldman's optimistic 2045 projections do not fully account for.

Third, the intersection of nuclear buildouts with tech-driven energy demands, briefly touched on in Goldman's earlier coverage of Big Tech's interest in uranium, reveals a critical pattern. Data centers, powering AI and cloud computing, are projected to account for 8% of global electricity demand by 2030, per the International Energy Agency (IEA). Nuclear energy's reliability makes it an attractive solution, yet Goldman's analysis overlooks how this demand spike could intensify uranium deficits sooner than anticipated. Companies like Microsoft, which announced a 2024 partnership with Constellation Energy to power data centers with nuclear energy, are already reshaping market dynamics—a trend that could outpace reactor construction timelines if policy and investment lag.

Synthesizing primary sources, the U.S. Department of Energy’s 2023 report on nuclear energy innovation underscores the urgency of scaling domestic fuel production and SMR technologies to meet net-zero goals, while the IAEA’s 2024 'Nuclear Energy Outlook' projects a doubling of global nuclear capacity by 2050 if current policy commitments hold. Both sources suggest that while momentum is undeniable, execution risks—ranging from funding to public opposition—remain understated in forecasts like Goldman’s. The EIA’s data on uranium import dependency further contextualizes the supply chain vulnerabilities that could undermine this nuclear resurgence.

In sum, the nuclear buildout, amplified by SMRs, represents a linchpin in the global shift to decarbonized energy systems. Yet, beyond Goldman's focus on reactor progress and uranium pricing, the story is one of geopolitical chess, policy friction, and tech-driven demand surges. These undercurrents will likely determine whether nuclear power fulfills its promise as a cornerstone of sustainable energy or stumbles under the weight of systemic challenges.

MERIDIAN: The nuclear buildout's success hinges on resolving uranium supply chain vulnerabilities and policy inconsistencies. Without rapid investment in domestic production and streamlined SMR regulations, projected deficits could spike prices and delay decarbonization goals.

Sources (3)

- [1]Nuclear Nuggets: Global Reactor Tracker - Goldman Sachs(https://www.zerohedge.com/energy/nuclear-buildout-accelerates-goldman-now-including-smrs-forecast)

- [2]U.S. Energy Information Administration - Uranium Market Data 2022(https://www.eia.gov/nuclear/uranium_marketing/html/summary.php)

- [3]International Atomic Energy Agency - Nuclear Energy Outlook 2024(https://www.iaea.org/publications/15260/nuclear-energy-outlook-2024)