Partners Group PE Fund Gate Signals Broader Liquidity Stress in Private Markets Overlooked by Public-Market Obsession

Partners Group's gating of its $8.6B evergreen PE fund after redemption requests hit 9.8% marks the spillover of private credit anxieties into equity strategies. This first-of-its-kind move for a major PE evergreen vehicle highlights structural liquidity mismatches in private markets, driven by reactive private wealth clients amid higher rates, exit backlogs, and valuation concerns—trends underreported amid focus on public equities.

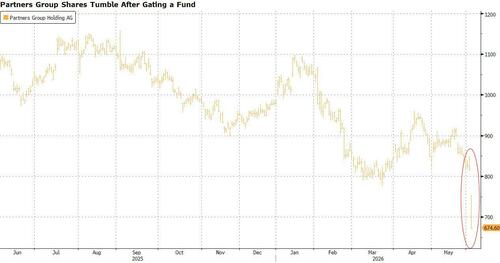

Partners Group has become the first major private equity manager to gate withdrawals from one of its flagship evergreen funds, capping redemptions at 5% of net asset value per quarter after requests surged to an estimated 9.8%. The $8.6 billion Global Value SICAV, which invests across private equity, credit, and other illiquid assets, now joins private credit vehicles facing sustained redemption pressure from skittish private wealth clients.[1][2]

According to a letter to investors reported by Bloomberg, the Swiss alternative asset manager cited macroeconomic shifts, geopolitical tensions, and accelerating flows from private credit into other private market strategies. CEO David Layton emphasized that the move protects long-term investors in inherently illiquid assets, noting that most redemptions originated from Asia and Australia. The firm maintains roughly 15% liquidity plus an undrawn credit facility, and insists the gating is not tied to underlying performance but to broader investor anxiety. Shares in Partners Group plunged as much as 18% on the news—the largest intraday drop on record—dragging down peers including EQT, CVC, and U.S. names like KKR, Blackstone, and Ares in sympathetic selling.[3][4]

This episode reveals dynamics mainstream financial coverage—preoccupied with public equities, Treasury yields, and headline credit spreads—has largely ignored. Evergreen funds, pioneered by Partners Group and now totaling over $56 billion across its platform, were sold as a more democratic, liquid gateway into private markets for high-net-worth individuals, who comprise about one-fifth of the firm's AUM and a outsized share of the Global Value fund. These clients, far more reactive than institutions, are now transmitting redemption pressure across asset classes after quarters of private credit outflows tied to concerns over software exposure, AI disruption, and debt quality.[1]

Deeper context from industry reports underscores the structural mismatch: private markets face a multi-year liquidity squeeze with trillions in unrealized buyout inventory, extended hold periods, and slower exits despite modest 2024-2025 rebounds in deal activity. McKinsey's Global Private Markets Report 2026 and Bain & Co. analyses highlight how higher interest rates have ended the easy-leverage, multiple-expansion era, forcing discipline on valuations while LPs constrain new commitments. What others miss is the feedback loop now emerging—gating in evergreen structures risks eroding trust in the 'semi-liquid' private market products marketed to retail-adjacent investors, potentially accelerating a shift toward secondaries at discounts and forcing GPs to confront over-valuations previously masked by infrequent marking.[5][6]

The Partners Group action, despite the firm's recent attempts to project positive fundraising momentum, functions as a canary. It demonstrates how private wealth's impatience can destabilize the delicate balance evergreen vehicles require between quarterly liquidity promises and multi-year underlying holds. As geopolitical and macro uncertainty persists, further spillover could pressure fundraising across private equity, real estate, and infrastructure while exposing the fragility of listed alternative managers whose public equities now trade as proxies for private-market health. This is not isolated idiosyncrasy; it is the surface manifestation of liquidity stress that public-market fixation has allowed to build largely out of sight.

LIMINAL: This first PE gating is an early warning of widening liquidity stress across private markets that could cascade into more fund restrictions, discounted secondaries, forced revaluations, and eroded confidence in evergreen products as wealth clients retreat—exposing risks that public market coverage continues to downplay.

Sources (5)

- [1]Partners Caps Evergreen Fund Redemptions as Requests Rise(https://www.bloomberg.com/news/articles/2026-06-03/partners-group-gates-evergreen-fund-as-redemption-requests-rise)

- [2]Partners Group cap prompts share plunge as private credit worries spread(https://www.reuters.com/world/partners-group-caps-withdrawals-86-billion-fund-shares-plunge-2026-06-03/)

- [3]Swiss Private-Equity Giant Caps Investor Withdrawals, Sparking Share Selloff(https://www.wsj.com/finance/investing/swiss-private-equity-giant-caps-investor-withdrawals-sparking-share-selloff-a4229304)

- [4]Global Private Markets Report 2026(https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report)

- [5]Private Equity Outlook 2025: Is a Recovery Starting to Take Shape?(https://www.bain.com/insights/outlook-is-a-recovery-starting-to-take-shape-global-private-equity-report-2025/)