The Fed's Engineered Market: How Interventions Have Rewired Cycles, Suppressed Risk Signals, and Rendered Traditional Bear Markets Obsolete

Federal Reserve interventions since 2008 have expanded its balance sheet dramatically, instituted a de facto 'put' on markets, and suppressed volatility, rendering classic 20% bear market definitions obsolete. High valuations persist amid moral hazard, transforming declines into buying opportunities while building hidden systemic fragilities evident in carry trades and leveraged positioning. Credible research and official records show this rewiring distorts risk signals, with mainstream views missing the engineered nature and long-term rupture potential.

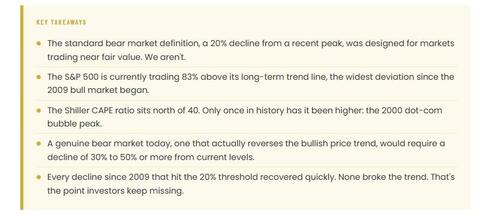

For decades, investors have relied on straightforward definitions: a 10% drop is a correction, while a 20% decline signals a bear market and a fundamental regime change. These rules, developed in the 1960s when markets orbited closer to fair value, no longer capture reality in an era of unprecedented Federal Reserve intervention. Structural policies including quantitative easing and the implicit 'Fed put' have fundamentally altered market cycles, compressing volatility, elevating valuations, and transforming what once were trend-reversing bear markets into temporary corrections within a policy-supported supercycle.

The scale of this rewiring traces directly to the Great Recession response. The Federal Reserve expanded its balance sheet through large-scale asset purchases (LSAPs) of mortgage-backed securities and longer-term Treasuries starting in 2008, shifting from traditional liquidity tools to direct market support aimed at lowering long-term rates and improving financial conditions. What began as emergency measures evolved into a new policy paradigm of prolonged accommodation, forward guidance, and repeated interventions that markets now price in as a backstop. Historical records show these actions limited immediate economic harm but fostered long-term dependency.[1][1]

Academic research corroborates an asymmetric policy response. Studies show the Fed's reaction to stock price declines intensifies sharply during recessions and bear markets, with a 10% drop raising the probability of rate cuts by roughly 50% in such environments—evidence of the 'Fed put' in action. This predictable easing suppresses volatility and encourages risk-taking, creating moral hazard on steroids. Rather than allowing prices to reflect underlying fundamentals, interventions have internalized protection, leading to rapid rebounds that obscure deeper fragilities.[2][3]

Valuation metrics underscore the distortion. Robert Shiller's cyclically adjusted price-to-earnings (CAPE) ratio has hovered at elevated levels far above its long-term average of approximately 17, reflecting prices stretched well beyond historical trends. Such extremes, once precursors to prolonged drawdowns lasting years with negative real returns, now occur within a framework where policymakers view sharp declines as threats to stability requiring response. This has disconnected traditional risk signals—yield curves, valuations, and momentum—from their historical predictive power.[4]

Going deeper, the pattern connects to global carry trades and volatility suppression dynamics. Central bank actions since the 1998 LTCM rescue through the 2020 COVID response have encouraged procyclical leverage, with markets assuming intervention before losses become systemic. Rapid recoveries following volatility spikes—such as the 2024 yen carry unwind—appear as resilience but actually demonstrate dependency on suppressed volatility and implicit backstops. This creates hidden leverage in nonbank sectors, debt-funded buybacks, and compressed risk premia, narrowing policy space amid competing mandates like inflation control. What mainstream coverage frames as 'normal volatility' is better understood as engineered rewiring: bear markets are no longer allowed to fully unfold, but the accumulated imbalances raise the tail risk of a larger dislocation when the backstop is tested by simultaneous shocks.[5]

The original intent of bear market definitions—to signal a genuine trend reversal and valuation reset—has been superseded. Without updates accounting for an eightfold balance sheet expansion and consistent put provision, the 20% threshold now measures noise within a Fed-dominated trend rather than a regime shift. Investors ignoring this structural change court complacency, as the next true test may arrive not as a standard correction but as a systemic unraveling when intervention limits are reached.

Liminal Analyst: The Fed's repeated rewiring of market cycles has severed price discovery from fundamentals, sustaining elevated valuations and suppressed signals that mask growing fragility—setting the stage for a potentially uncontainable correction when policy space evaporates amid inflation or geopolitical shocks.

Sources (5)

- [1]The Great Recession and Its Aftermath(https://www.federalreservehistory.org/essays/great-recession-and-its-aftermath)

- [2]Why the G7 Must Tackle Hidden Systemic Threats to Global Financial Stability(https://www.csis.org/analysis/why-g7-must-tackle-hidden-systemic-threats-global-financial-stability)

- [3]When does the fed care about stock prices?(https://www.sciencedirect.com/science/article/abs/pii/S0378426622001522)

- [4]How the Fed Responds to Stock Market Moves(https://www.nber.org/digest/sep01/how-fed-responds-stock-market-moves)

- [5]Online Data - Robert Shiller(http://www.econ.yale.edu/~shiller/data.htm)