Trump-Warren Alliance Exposes Housing Financialization as Wealth Transfer Mechanism

Bipartisan legislation backed by Trump and Warren restricts institutional investors (350+ homes) from buying more single-family properties, with exemptions and sell-off rules. Beyond consumer safeguards, it challenges the financialization of housing as a driver of upward wealth transfer, highlighting populist tensions over shelter as asset class vs. human need. Critics warn of supply risks.

In a development that defies conventional political lines, Congress appears poised to restrict large private equity and institutional investors from further acquiring single-family homes through the 21st Century ROAD to Housing Act. The Senate passed the legislation in March 2026 by a resounding 89-10 margin, building on an earlier strong House vote, with explicit backing from President Trump—who framed it as ensuring "homes are for people, not corporations"—and collaboration involving Senator Elizabeth Warren. While mainstream coverage often casts this as consumer protection against predatory landlords and rent hikes, a deeper examination reveals it as an emerging challenge to the post-2008 financialization of American housing, where shelter was systematically converted into an asset class that funnels wealth upward.[1][2]

Following the financial crisis, institutional capital, including spinoffs from firms like Blackstone, aggressively purchased distressed single-family properties, transforming them into rental portfolios. This "build-to-rent" model accelerated, doubling its market share by concentrating ownership in key metros like Atlanta and pricing out individual buyers. Federal Reserve research and FTC actions documented how these investors imposed 60% higher rent increases, junk fees, and reduced maintenance, effectively extracting economic rents from families rather than facilitating ownership and generational wealth building. The result is a structural wealth transfer: homeownership, historically the primary vehicle for middle-class equity accumulation, becomes harder for younger cohorts while institutional balance sheets swell with predictable yields in a low-rate environment.[3]

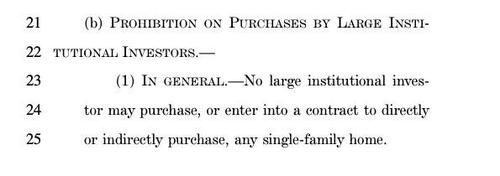

The bill defines "large institutional investors" as for-profit entities controlling 350 or more single-family homes (excluding manufactured housing), prohibiting most additional purchases with carve-outs for certain build-to-rent, senior, or renovated properties—often mandating sale to individuals after seven years. Notably, it imposes no forced divestiture of existing holdings, includes enforcement via steep penalties, and sunsets after 15 years. This framework, while populist in rhetoric, attempts market restructuring by altering incentives that treated housing primarily as a financial commodity rather than a foundational human need. Critics from libertarian and abundance perspectives argue it may constrict rental supply and deter innovation, potentially exacerbating shortages if not matched with zoning liberalization. Yet the unusual alignment—Trump's executive order prioritizing "Stopping Wall Street from Competing with Main Street Homebuyers" meeting Warren's long-standing scrutiny of corporate landlords—suggests broader erosion of neoliberal consensus on unrestricted capital flows into everyday life.[1][4]

Mainstream outlets frame the tensions narrowly around affordability metrics, evictions, and "junk fees," missing the heterodox implication: this is pushback against a system where housing scarcity benefits asset managers more than it incentivizes broad-based supply growth. By limiting institutional dominance in the single-family sector, the proposal implicitly questions how financial engineering since the Great Recession redistributed claims on future shelter costs. Whether this yields meaningful decompression of wealth concentration or merely symbolic restraint amid ongoing supply constraints remains uncertain. The bill's reconciliation process, including modifications that some claim soften its edge at private equity's behest, will determine if it restructures incentives or preserves the status quo. What unites disparate factions is recognition that unchecked corporate absorption of the housing stock intensifies affordability as a political crisis, one rooted in treating homes as perpetual yield vehicles.

LIMINAL: This rare alignment reveals housing financialization as a core vector of intergenerational wealth extraction; the ban may blunt rentier power but risks incomplete restructuring absent deeper supply-side reforms, exposing fractures in both parties' growth models.

Sources (5)

- [1]Senate Advances 21st Century ROAD to Housing Act(https://www.lw.com/en/insights/senate-advances-21st-century-road-to-housing-act)

- [2]What's in the 21st Century ROAD to Housing Act?(https://bipartisanpolicy.org/explainer/whats-in-the-21st-century-road-to-housing-act/)

- [3]US Senate Advances Housing Legislation that Includes a Ban on Institutional Investors Purchasing Single-Family Homes(https://www.mayerbrown.com/en/insights/publications/2026/03/us-senate-advances-housing-legislation-that-includes-a-ban-on-institutional-investors-purchasing-single-family-homes)

- [4]Senate passes bipartisan housing bill targeting large investors(https://www.npr.org/2026/03/12/nx-s1-5742566/senate-bipartisan-housing-bill-investors-ban)

- [5]Warren Probes Biggest Corporate Landlords on Predatory Rental Practices(https://www.banking.senate.gov/newsroom/minority/warren-probes-biggest-corporate-landlords-on-predatory-rental-practices-across-housing-sector)