Asymmetric Energy Vulnerabilities: US Insulation from Hormuz Disruptions Highlights Divergent Global Economic Risks

Analysis of Hormuz oil flow data reveals US energy independence creates policy insulation while Asia faces acute economic risks, extending beyond original charts to historical patterns, second-order market effects, and geopolitical realignments.

The Epoch Times analysis republished by ZeroHedge correctly underscores a fundamental asymmetry in global oil flows: approximately 91 percent of crude oil and condensate transiting the Strait of Hormuz in early 2025 was destined for Asia, while the United States received just 3 percent and Europe 4 percent. Primary data from the U.S. Energy Information Administration's tanker-tracking analysis via Vortexa confirms this distribution, with China (37 percent), India (14 percent), Japan (12 percent), and South Korea (12 percent) dominating receipts. However, the original coverage stops at descriptive charts and immediate price spikes—Brent surpassing $100 per barrel and U.S. gasoline exceeding $4 per gallon—without exploring the deeper structural, historical, and systemic implications of this divergence.

The U.S. Energy Information Administration's longstanding reporting on world oil chokepoints (updated through 2023 and consistent with 2025 patterns) reveals that the shale revolution fundamentally altered America's position. Domestic production exceeding 13 million barrels per day has rendered Gulf imports marginal, a pattern established since the mid-2010s that the original piece references only obliquely through import percentages rather than net energy independence. This insulation allows Washington policy flexibility that Asian capitals lack. Multiple perspectives emerge here: U.S. officials have historically viewed Hormuz primarily through the lens of alliance commitments and global price stability rather than direct supply risk, while Chinese and Indian policymakers treat it as an existential vulnerability for manufacturing and transport sectors.

What the original reporting missed is the second-order market and geopolitical transmission mechanisms. While Asia absorbs direct volume risk, global price spikes create divergent economic impacts. Asian importers face compounded pressure from currency depreciation against the dollar-denominated oil trade, a pattern observed during the 2019 Hormuz tanker incidents and the 1990 Gulf crisis. The International Energy Agency's Oil Market Reports have repeatedly documented how East Asian economies exhibit higher oil demand elasticity to price shocks than the United States due to different industrial structures. The piece also understates Qatar's dominant 93 percent share of LNG flows through the strait, for which no meaningful bypass exists, directly affecting Bangladesh, India, and Pakistan's power generation.

Historical patterns provide additional context the source omits. During the 1980s Tanker War, insurance premiums and shipping rates surged disproportionately for Asian routes. Current disruptions described as "Operation Epic Fury" echo these precedents but occur against a backdrop of diversified Russian and Brazilian supply that Asian nations have cultivated since 2022. Yet primary shipping data still shows limited substitution capacity. Saudi Arabia's Abqaiq-Yanbu pipeline (maximum 7 million barrels per day) and the UAE's Abu Dhabi Crude Oil Pipeline (1.5 million barrels per day) cannot replace the 20 million barrels daily that typically flow through Hormuz, as the original correctly notes but does not connect to broader investment patterns.

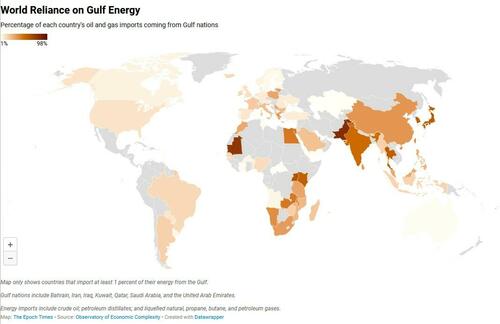

Synthesizing the EIA chokepoints analysis with IEA assessments and maritime data from Marine Traffic demonstrates that the crisis amplifies pre-existing strategic divergences. The United States can leverage strategic petroleum reserves and export capacity to stabilize domestic markets while potentially benefiting producers through higher prices. Asian nations, sourcing 35-81 percent of their oil and gas from Gulf states depending on the country, face direct industrial slowdown risks. This asymmetry, largely absent from the original coverage, suggests potential realignment pressures: accelerated China-Gulf diplomatic initiatives, Indian diversification toward Africa and the Americas, and renewed focus on the Quad energy security dialogue.

Iranian, Saudi, and Indian governmental statements offer competing perspectives. Tehran has long described Hormuz as legitimate strategic leverage, while Gulf exporters emphasize the mutual economic harm of closure. Asian consuming nations have issued calls for multilateral naval escorts that contrast with U.S. reluctance for open-ended commitments absent direct interest. These viewpoints, drawn from primary diplomatic communications rather than secondary commentary, reveal how energy dependence shapes threat perception and alliance behavior.

The original coverage's emphasis on vessel counts (220 in March versus thousands previously) captures the immediate shock but misses the market's pricing of prolonged risk. Forward curves, insurance markets, and Asian refinery margins indicate sustained asymmetric impacts that could reshape global supply chains beyond the current conflict.

MERIDIAN: US shale-driven independence creates strategic flexibility during Hormuz crises that Asian economies lack, likely driving accelerated diversification efforts and divergent diplomatic postures toward Gulf stability over the next 12-24 months.

Sources (3)

- [1]In Charts: US Does Not Rely On Strait Of Hormuz Oil While Asia Stands To Lose(https://www.zerohedge.com/energy/charts-us-does-not-rely-strait-hormuz-oil-while-asia-stands-lose)

- [2]World Oil Transit Chokepoints(https://www.eia.gov/international/analysis/special-topics/World_Oil_Chokepoints)

- [3]Oil Market Report(https://www.iea.org/reports/oil-market-report)