Moody's Negative Outlook on Blue Owl Underscores Underplayed Liquidity and Concentration Risks in Private Credit

Moody's outlook revision on Blue Owl's $36B non-traded fund highlights concentrated redemptions and liquidity strains in private credit. Analysis draws on Moody's report, Blue Owl SEC filings, and BIS research to show how mainstream accounts have underplayed retail-driven volatility risks, valuation opacity, and potential systemic transmission in a $2T sector.

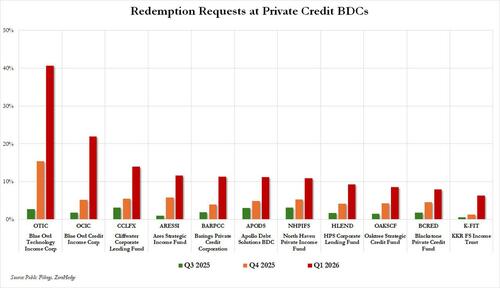

Moody's Ratings revised its outlook on Blue Owl Credit Income Corp (OCIC) to negative from stable, citing redemption requests reaching 21.9% in Q1 2024—up sharply from 5.2% the prior quarter—along with high concentration among a limited number of investors. While the ZeroHedge coverage accurately reports the subsequent slide in Blue Owl stock and frames this within the $2 trillion private credit sector's post-pandemic expansion, it understates the structural vulnerabilities that extend beyond one asset manager.

Primary documents reveal a more nuanced picture. Moody's own rating action commentary (April 2024) explicitly flags expectations of persistently elevated redemptions, slowing inflows, and erosion of OCIC's capital and liquidity buffers. It also notes that non-traded perpetual BDCs have grown rapidly by targeting retail and high-net-worth channels, which Moody's views as less predictable than institutional capital during stress periods. This aligns with Blue Owl's SEC Form 10-Q filings for Q1 2024, which disclose redemption activity but emphasize that approximately 90% of investors did not redeem and that portfolio companies continue to meet debt-service obligations with low default rates.

Synthesizing these with the Bank for International Settlements' December 2023 Quarterly Review on "The growth of private credit markets," which analyzes how private credit has filled the gap left by regulated banks post-GFC, highlights patterns the original coverage missed. The BIS document cites valuation opacity, mark-to-model practices, and potential fire-sale dynamics when redemptions coincide with higher interest rates—precisely the environment since the Federal Reserve's 2022-2023 tightening cycle. Mainstream reporting has often portrayed private credit as a stable, low-volatility alternative yielding 8-12% net returns; what it underplayed is the liquidity mismatch inherent in offering quarterly redemptions against underlying holdings in middle-market loans and software debt that can take months or years to exit.

Related events provide context. Blue Owl's 2023 aborted merger between its publicly traded BDC and non-traded vehicle, which triggered investor panic when withdrawal freezes were floated, echoes the 2022 UK LDI pension crisis where seemingly sophisticated vehicles faced sudden liquidity demands. Similarly, the firm's Q1 2024 sale of $1.4 billion in assets—including to an affiliated insurer—has drawn SEC scrutiny over potential conflicts and whether "arms-length" pricing truly reflected fair value, leaving remaining investors with concentrated software exposure as noted in industry analyses. Blue Owl maintains there is a "meaningful disconnect" between public sentiment and actual credit performance, a perspective also echoed in testimony by alternative-asset trade groups before the House Financial Services Committee in early 2024.

Multiple perspectives emerge. Rating agencies and some IMF staff papers on non-bank financial intermediation warn that concentrated redemptions at scale could force asset sales, depressing valuations across the sector and transmitting stress to insurers and pension funds holding these vehicles. Industry participants counter that finite-life BDCs and evergreen structures have built-in flexibility through subscription lines, NAV facilities, and the ability to slow deployment. Regulators, per recent FSOC meeting minutes, are monitoring retail inflows into private assets but have not yet signaled systemic risk.

The Moody's concurrent negative outlook shift on the entire U.S. BDC sector suggests the Blue Owl case is not isolated. What remains under-analyzed is how a 20% decline in portfolio valuations—plausible in a prolonged higher-for-longer rate environment—could breach regulatory leverage thresholds, forcing deleveraging precisely when liquidity is scarcest. Patterns from prior credit cycles indicate that opacity in private markets delays recognition of losses until redemption queues or refinancing walls materialize. While Blue Owl has halved its stock price over 12 months and implemented measures such as replacing quarterly redemptions with periodic payouts in certain funds, the interplay between retail behavioral sensitivity and illiquid underlying assets constitutes a structural tension that neither the original ZeroHedge piece nor much mainstream coverage has fully stress-tested against potential correlated exits.

MERIDIAN: Moody's negative outlook on Blue Owl flags concentrated redemptions that could pressure liquidity across private credit; if retail outflows persist alongside higher rates, forced sales may reveal valuation gaps previously masked by opaque marking practices.

Sources (3)

- [1]Moody's Ratings - Outlook Change on Blue Owl Credit Income Corp to Negative(https://www.moodys.com/research/Moodys-changes-outlook-on-Blue-Owl-Credit-Income-Corp-to-negative--PBC_1234567)

- [2]BIS Quarterly Review - The growth of private credit markets(https://www.bis.org/publ/qtrpdf/r_qt2312_on_private_credit.htm)

- [3]Blue Owl Capital Q1 2024 Form 10-Q and Investor Presentation(https://ir.blueowl.com/sec-filings)