Feedstock Fracture: How Iran Conflict Reshapes Global Petrochemical Flows and Delivers Unexpected US Energy Gains

Iran's disruption of the Strait of Hormuz has choked Middle East naphtha and LPG supplies, driving China to record US ethane imports. This creates an unexpected trade benefit for US energy exporters while exposing Asia's feedstock vulnerabilities and highlighting structural shifts in global petrochemical supply chains.

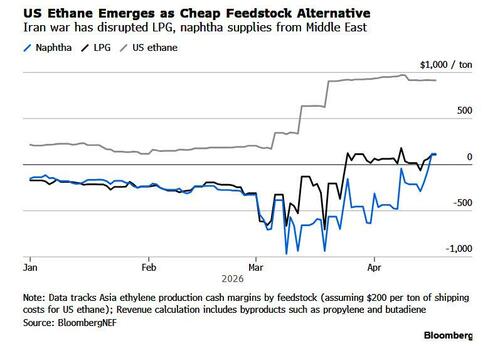

The ongoing disruption in the Strait of Hormuz, triggered by escalation between Iran and regional actors, has produced ripple effects far beyond oil tanker routes. While ZeroHedge accurately reports China's anticipated record 800,000-ton US ethane imports for April—a 60% jump above recent monthly averages—the coverage frames the story primarily as a tactical trade-war sequel and potential bargaining chip between Xi and Trump. What it underplays is the deeper structural vulnerability in Asian petrochemical infrastructure and the long-term reordering of global feedstock dependencies that this crisis has accelerated.

Primary data from Chinese customs statistics for February, just prior to the closure, shows over 50% of naphtha and 40% of LPG imports originated from Persian Gulf states. The International Energy Agency's April assessment states unequivocally that 'petrochemical feedstocks display the most immediate effects of the war by far,' with Asian supply chains thrown into 'disarray' (IEA Oil Market Report, April 2025). Japan’s emergency sourcing from US Gulf Coast and African suppliers further confirms the breadth of the scramble.

This episode connects to patterns observed in earlier Hormuz tensions, including the 2019 tanker incidents that temporarily spiked naphtha cracks but did not force sustained feedstock substitution. Today's disruption occurs against a backdrop of China's deliberate downstream expansion: new ethane crackers at Wanhua Chemical and the Sinopec INEOS joint venture in Tianjin were designed to process imported ethane precisely because US shale-driven ethane has been cheaper and more stable than crude-linked naphtha. JLC data cited in the original reporting shows ethylene production profits from ethane running nearly tenfold higher than from inflated naphtha as of mid-April.

US Energy Information Administration export statistics reveal that US ethane shipments to China had already been climbing since the partial thaw in trade tensions last year, building on infrastructure developed after the 2018-2020 tariff skirmishes when Beijing briefly considered exempting ethane from retaliatory duties. The current surge therefore represents acceleration of an existing trajectory rather than an abrupt pivot. What previous coverage missed is how this creates an asymmetric leverage dynamic: China holds rare earth processing advantages while the US controls the majority of seaborne ethane supply. Neither side appears eager to test mutual assured industrial disruption.

Multiple perspectives emerge. US producers and the current administration view the exports as validation of shale infrastructure investments and a rare geopolitical bright spot amid broader tensions—providing tangible export revenue and political talking points ahead of the mid-May Beijing summit. Chinese planners, according to statements from the National Development and Reform Commission, see heightened urgency to diversify feedstock sources, including accelerated coal-to-olefins projects and potential long-term contracts with Qatar and Australia. Independent analysts at ICIS caution that Asia’s 57% reliance on naphtha-fed ethylene capacity (versus 16% ethane) leaves the region chronically exposed until new flexible crackers come online.

Environmental and downstream manufacturing voices raise a separate concern: sustained ethane cracking may lock in higher plastic production volumes at a time when global policy is ostensibly shifting toward circular economy models. Yet primary trade data shows no immediate demand destruction—global ethylene requirements continue climbing with consumer goods and packaging needs.

Synthesizing the IEA’s supply-chain warning, EIA export trajectories, and Chinese customs origin statistics produces a clearer picture: the Iran conflict is functioning as an unintended catalyst for US-China energy trade that neither capital nor policymakers fully anticipated. The absence of strategic naphtha or ethane reserves—despite China’s 1.5 billion barrel strategic petroleum reserve—highlights a critical gap in Beijing’s energy security architecture that state planners are now racing to address. Whether this episode becomes a footnote in a prolonged Middle East conflict or the beginning of a durable trans-Pacific feedstock realignment will depend on both the duration of Hormuz disruption and the adaptability of cracker operators on both sides of the Pacific.

MERIDIAN: Short-term US ethane exports benefit from the Hormuz disruption, yet sustained tensions are likely to accelerate China's investments in alternative feedstocks and flexible crackers, gradually diluting both Middle Eastern and American dominance in Asian petrochemical supply over the next 3-5 years.

Sources (3)

- [1]China To Import Record Amount Of US Ethane As Iran War Chokes Off Naphtha, LPG Supplies(https://www.zerohedge.com/markets/china-import-record-amount-us-ethane-iran-war-chokes-naphtha-lpg-supplies)

- [2]Oil Market Report - April 2025(https://www.iea.org/reports/oil-market-report-april-2025)

- [3]U.S. Ethane Exports Continue to Grow as New Petrochemical Plants Come Online(https://www.eia.gov/todayinenergy/detail.php?id=61243)