Apparel, Furniture and Plastics to Vanish First as Petrochemical Shock Exposes Global Supply Chain Fragility

Ongoing petrochemical and oil supply disruptions from Middle East conflict are idling Asian textile, furniture, and plastics factories, with basic apparel, sofas, bedding, and consumer plastics forecast to face shortages first. This reveals deep structural fragility in just-in-time globalized production and foreshadows broader inflation and deglobalization pressures.

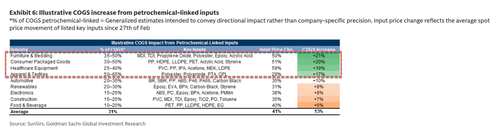

As Middle East conflict disrupts crude flows through the Strait of Hormuz, a petrochemical supply shock has rapidly transmitted into Asian manufacturing, forcing production cuts and threatening consumer shortages. Goldman Sachs analysts, including chemicals specialist Georgina Fraser, document how costs for PTA, caprolactam, polyester and polyamide have risen roughly 29% on average, driving COGS increases of 17-21% across key sectors. Furniture and bedding face ~21% cost inflation, consumer goods ~20%, healthcare equipment ~19%, and textiles/apparel ~17%. With typical textile margins of just 5-15%, many operators find continued production uneconomic, leading to idled lines and standstills.

Corroborating evidence is already visible on the ground. Textile weaving units in Surat, India—the world's largest hub for man-made fabrics—have collectively restricted operations to a single 12-hour shift per day amid surging yarn prices, labor issues, and demand weakness tied directly to the West Asia crisis. Industry associations are enforcing the measure until conditions stabilize. Broader regional stress includes reduced petrochemical output in South Korea, Japan, and China, diesel spikes, falling imports, and early signs of rationing and industrial slowdowns.

This episode illuminates systemic fragility few mainstream analysts connect: globalized production's extreme dependence on Asian factories that themselves rely on Middle East-derived petrochemical feedstocks for synthetic fibers, foams, plastics, and resins. Asia accounts for the vast majority of global textile capacity and apparel exports; polyester and polyamide dominate modern clothing, while polyurethane appears throughout furniture, bedding, and medical disposables. Just-in-time inventory practices mean retailers hold minimal buffer stock. Consequently, the first goods likely to disappear from shelves are T-shirts and basic apparel, upholstered furniture and sofas, synthetic bedding, plastic household items, and certain single-use healthcare products. These low-margin, high-volume categories cannot absorb sustained 17-21% input cost shocks without output contraction.

Deeper connections reveal this as the next wave of economic disruption. Unlike the 2020-2022 pandemic snarls, the trigger is geopolitical and potentially persistent even if fighting subsides, as inventories have already drawn down and confidence evaporated. It exposes the illusion of stable globalization: a single energy chokepoint can cascade into empty retail racks for everyday basics within weeks. This fragility may accelerate deglobalization pressures, friend-shoring initiatives, and higher baseline inflation in consumer staples, while punishing precisely those industries least equipped to pivot. The shock also underscores overlooked interdependence between oil markets, petrochemical crackers, and downstream consumer manufacturing—links that optimized supply chains treated as permanent rather than precarious.

Even an imminent resolution to the underlying conflict would not instantly unwind the production halts already underway. Consumers should prepare for higher prices, thinner selection, and potential quality substitution in clothing, home goods, and plastics long before more complex electronics or autos show visible strain. The episode serves as a stark forecast of how globalized efficiency, absent resilience, breeds repeated crises.

LIMINAL: Everyday synthetic apparel, upholstered furniture, and plastic consumer goods will disappear from shelves first, exposing how one Middle East energy chokepoint can unravel just-in-time globalization and trigger the next sustained wave of shortages and consumer inflation.

Sources (4)

- [1]Weavers opt for 12-hour shift to cut output amid rising costs(https://timesofindia.indiatimes.com/city/surat/weavers-opt-for-12-hour-shift-to-cut-output-amid-rising-costs/articleshow/129909611.cms)

- [2]Goldman Sachs Warns Oil's Biggest Shock Will Hurt Fuels Most(https://www.bloomberg.com/news/articles/2026-03-17/goldman-says-oil-s-biggest-shock-to-hurt-refined-products-most)

- [3]Goldman Sachs warns of Asia Oil shock: 5 signs of fuel rationing risks ahead(https://www.financialexpress.com/market/goldman-sachs-warns-of-asia-oil-shock-5-signs-of-fuel-rationing-risks-ahead-4196713/)

- [4]Surat Weavers Cut Operations to Single 12-Hour Shift Amidst West Asia Conflict(https://apparelresources.com/business-news/manufacturing/surat-weavers-cut-operations-single-12-hour-shift-amidst-west-asia-conflict/)