Bank of Japan's Rare Vote Split Signals Deepening Economic Fault Lines Amid Stagflation Fears

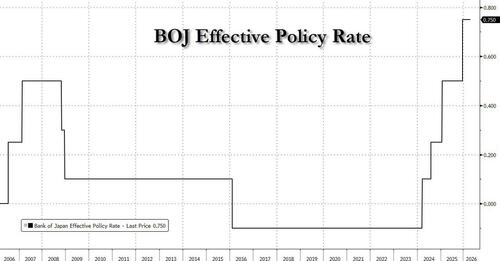

The Bank of Japan’s 6-3 vote split on maintaining rates at 0.75% reveals deep divisions over addressing stagflation risks, with inflation forecasts revised to 2.8% amid Middle East-driven energy shocks. Beyond the decision, historical policy inertia, domestic political pressures, and global monetary trends highlight Japan’s unique vulnerabilities and potential influence on investor sentiment and central bank strategies worldwide.

The Bank of Japan’s (BoJ) recent decision to maintain its benchmark interest rate at 0.75% in a rare 6-3 vote split reveals a growing rift within its Monetary Policy Committee over how to address mounting economic vulnerabilities. Announced on October 31, 2023, the decision comes as the BoJ sharply revised its core CPI forecast to 2.8% for the fiscal year ending March 2027, up from 1.9%, while warning of slowing growth—a textbook stagflation scenario. Governor Kazuo Ueda’s cautious stance, emphasizing uncertainty due to Middle East conflicts and their impact on energy prices, contrasts with the dissenting voices of Naoki Tamura, Hajime Takata, and surprisingly, the more dovish Junko Nakagawa, who pushed for an immediate hike to 1%. This internal discord, the widest since the negative interest rate policy began in 2016, underscores a critical debate: whether the BoJ risks falling further behind the inflation curve by delaying normalization of monetary policy.

Beyond the immediate decision, this split reflects broader structural challenges for Japan, a nation heavily reliant on Middle Eastern oil imports (over 90% of its crude supply). The BoJ’s outlook statement explicitly notes downside risks to growth and upside risks to prices, a dynamic exacerbated by geopolitical instability. Yet, what the original coverage misses is the deeper historical context of Japan’s monetary policy inertia. Since the 1990s, Japan has grappled with deflationary pressures, leading to ultra-loose policies that have constrained its ability to pivot swiftly during inflationary shocks. The current situation mirrors the 1970s oil crises, when Japan faced similar stagflationary pressures, but today’s globalized economy and post-pandemic recovery add layers of complexity. The BoJ’s hesitance also contrasts with the U.S. Federal Reserve’s more aggressive rate hikes in 2022-2023 to combat inflation, highlighting divergent central bank strategies despite shared global risks like energy price volatility.

Another underexplored angle is the domestic political dimension. Ueda’s reluctance to commit to a rate hike timeline may reflect tacit pressure from the Japanese government, which prioritizes economic stability amid a fragile recovery. A rate hike could strengthen the yen—potentially easing import costs—but risks dampening consumer spending and corporate investment, a concern for Prime Minister Fumio Kishida’s administration as it navigates public discontent over rising living costs. The original source notes market expectations of a June 2024 hike, but overlooks how Japan’s unique labor market dynamics, including recent wage increases, could force the BoJ’s hand sooner if inflation expectations become unanchored. Wage growth, while a positive sign after decades of stagnation, now fuels price pressures in a low-growth environment, a nuance not fully captured in the initial reporting.

Globally, the BoJ’s decision reverberates through financial markets and monetary policy circles. As the first G5 central bank to announce this week, alongside expected holds from the Fed, ECB, BoE, and Bank of Canada, Japan’s stance may signal a broader hesitance to tighten policy amid geopolitical uncertainty. Yet, Japan’s specific exposure to energy shocks positions it as a bellwether for how resource-dependent economies might fare in a prolonged Middle East crisis. Investors, already skittish about global inflation, may interpret the BoJ’s split as a warning of policy paralysis, potentially driving capital flows toward safer assets or currencies like the U.S. dollar. This dynamic connects to patterns seen during the 2022 energy crisis, when yen depreciation accelerated as the BoJ lagged behind other central banks in tightening.

Synthesizing primary and related sources, the BoJ’s own policy statement highlights the stagflation risk explicitly, while the International Energy Agency’s (IEA) 2023 World Energy Outlook warns of sustained oil price volatility due to Middle East tensions, directly impacting Japan’s import costs. Additionally, the International Monetary Fund’s (IMF) October 2023 World Economic Outlook notes Japan’s limited fiscal space to cushion energy shocks, a constraint that could force monetary tightening despite growth risks—an angle absent from initial coverage. Together, these sources suggest that the BoJ’s internal divide is not just a policy disagreement but a microcosm of Japan’s precarious balancing act between inflation control, energy dependence, and political stability in a volatile global landscape.

In conclusion, the BoJ’s 6-3 vote split is more than a procedural anomaly; it signals a critical juncture for Japan’s economy, with implications for global monetary policy coordination and investor sentiment. The central bank’s next moves—whether in June or sooner—will test its ability to navigate stagflation without triggering a deeper downturn, while offering a case study in how historical policy legacies shape responses to contemporary crises. What remains uncertain is whether domestic and international pressures will converge to force a bolder shift, or if caution will prevail at the risk of prolonged economic stagnation.

MERIDIAN: The BoJ’s internal split and stagflation warnings suggest a high likelihood of a rate hike by mid-2024, potentially in June, if Middle East tensions stabilize and domestic inflation pressures persist. However, political constraints could delay action, risking further yen weakness.

Sources (3)

- [1]Bank of Japan Monetary Policy Statement, October 31, 2023(https://www.boj.or.jp/en/mopo/mpmdeci/mpr_2023/index.htm)

- [2]International Energy Agency World Energy Outlook 2023(https://www.iea.org/reports/world-energy-outlook-2023)

- [3]International Monetary Fund World Economic Outlook, October 2023(https://www.imf.org/en/Publications/WEO/Issues/2023/10/10/world-economic-outlook-october-2023)