The Unnamed Mechanism: How Bipartisan Monetary Denial Drives America's Deepening Inequality and Cultural Fracture

Monetary policy and repeated QE represent the core, bipartisan-ignored driver of wealth inequality and resulting cultural/fiscal decay. Real research from the Fed, Brookings, IMF, and ProPublica shows asset inflation overwhelmingly benefits the wealthy, revealing a deeper denial that renders partisan fights theater while perpetuating systemic distortion.

While politicians from both parties engage in perpetual theater over taxes, spending, immigration, and cultural flashpoints, a deeper force quietly reshapes the economic and social landscape: the Federal Reserve's permanent regime of monetary intervention. This 'third rail'—rarely named in partisan combat—has become the primary engine of wealth concentration, distorting markets, socializing risk for the connected, and fueling the cultural decay visible in declining trust, rising populism, and institutional erosion that neither side will confront.

Extensive research corroborates the original critique. Quantitative easing and ultra-low rates disproportionately inflate asset prices—stocks, real estate, equities—held overwhelmingly by the top decile and especially the top 1%. A New York Fed staff report found that unconventional policies reduced inequality within the bottom 90% via unemployment channels but significantly widened the gap between the top 10% and everyone else through profits and equity appreciation. Similarly, research from the Center for Economic and Policy Research concluded that while employment gains and mortgage refinancing from QE were equalizing, these effects were 'swamped by the large dis-equalizing effects of equity price appreciations,' resulting in modestly increased overall inequality. ProPublica documented how the Fed's policies triggered a multitrillion-dollar stock boom that exacerbated decades-long inequality trends, with the rich capturing the vast majority of gains while working-class households saw minimal wealth uplift.

Brookings Institution analyses and IMF working papers further contextualize this: expansionary monetary shocks often deliver short-term employment benefits skewed toward lower-income and minority groups but generate persistent wealth transfers upward due to asset ownership concentration. One IMF study across advanced economies found contractionary policy increases income inequality while expansionary moves show complex but often disequalizing wealth effects in the short-to-medium term. These are not fringe assertions but patterns acknowledged in official research, even as policymakers frame interventions as universally beneficial 'stabilization.'

The deeper pattern this reveals is one of systemic denial shaping all outcomes. Both parties reliably endorse the Fed's independence and its 'infinite' liquidity backstop—evident in repeated bipartisan support during crises and oversight hearings—because it sustains the financialized economy their donor classes inhabit. Republicans decry fiscal profligacy while ignoring how endless balance sheet expansion monetizes debt; Democrats push redistribution rhetoric while depending on the asset inflation that props up portfolios and campaign finance. This consensus on monetary machinery collapses the illusion of competing ideologies.

Connections missed in mainstream discourse tie this directly to cultural and fiscal decay. By replacing organic price discovery with liquidity dependency, the regime erodes the link between productivity and reward, fostering moral hazard, zombie firms, and a rentier class detached from real economy contribution. This economic bifurcation manifests culturally: hollowed-out middle classes fuel polarization, conspiracy thinking, and anti-institutional sentiment on both flanks—from Occupy Wall Street to MAGA skepticism of 'the Fed.' Rising wealth gaps correlate with declining social cohesion, trust in democracy, and fertility rates, as younger generations face asset prices decoupled from wages. The Cantillon effect—new money benefiting financial insiders first—operates as an unacknowledged tax on the periphery, amplifying the very grievances politicians exploit without addressing root causes.

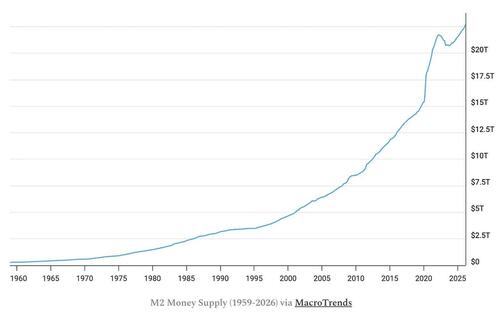

What began as emergency measures post-2008 and COVID has normalized into structural reality: the Fed's balance sheet ballooned from under $1 trillion pre-crisis toward multiples higher, with interventions now expected at any whiff of correction. Historical valuation metrics lose meaning in this distorted system. Until the pattern of denial breaks—requiring honest reckoning with how monetary policy drives outcomes neither party wants to own—surface debates will remain performative, ensuring continued decay beneath the partisan noise.

Liminal Observer: This unaddressed monetary distortion will accelerate populist surges, institutional distrust, and social fragmentation, forcing a reckoning neither party is prepared to navigate as asset dependency clashes with real economic limits.

Sources (5)

- [1]Inequality: Is the Fed to blame?(https://www.brookings.edu/articles/inequality-is-the-fed-to-blame/)

- [2]How the Federal Reserve Is Increasing Wealth Inequality(https://www.propublica.org/article/how-the-federal-reserve-is-increasing-wealth-inequality)

- [3]Quantitative Easing and Inequality(https://www.newyorkfed.org/research/staff_reports/sr1108)

- [4]Did Quantitative Easing Increase Income Inequality?(https://www.cepweb.org/wp-content/uploads/2017/11/Montecino-paper.pdf)

- [5]The Effects of Monetary Policy Shocks on Inequality(https://www.imf.org/external/pubs/ft/wp/2016/wp16245.pdf)