Fed Faces Policy Trap as Sticky Inflation, Private Credit Risks and Record Debt Converge

The Federal Reserve confronts a challenging mix of above-target inflation (CPI at 2.4% YoY in Feb 2026), mounting private credit and CRE refinancing risks, and record federal debt that may limit monetary options, raising concerns about systemic economic fragility.

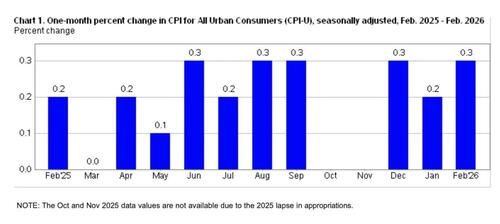

As of early 2026, the Federal Reserve finds itself in a constrained position, balancing persistent inflation above its 2% target with emerging stresses in leveraged financial segments. U.S. CPI rose 2.4% for the 12 months ending in February 2026, with core measures holding at 2.5%, confirming that inflation has not fully returned to the central bank's preferred level despite prior rate hikes and quantitative tightening. At the same time, the Fed has held its target range for the federal funds rate at 3.5-3.75% in March, acknowledging ongoing uncertainties in the economic outlook. This environment limits traditional monetary responses: aggressive rate cuts or balance sheet expansion to address market stress risk re-accelerating price pressures, while inaction could allow fragilities to spread. A key area of concern is the private credit market, which has expanded rapidly to fill gaps left by traditional banks, particularly in commercial real estate (CRE). With over $2 trillion in CRE loans expected to mature by 2030—many originated in a low-rate environment—refinancing challenges are mounting amid higher borrowing costs and shifting demand for office and retail space. Private credit's opacity and leverage have drawn comparisons to potential systemic risks, with recent commentary questioning whether it could become the next major stress point on Wall Street. These issues connect to broader fiscal pressures: U.S. national debt has reached approximately $38 trillion, with debt-to-GDP around 120%. Former Treasury Secretary Janet Yellen and economists have warned of "fiscal dominance," where massive government borrowing needs could constrain the Fed's ability to fight inflation without exacerbating debt servicing costs. A Federal Reserve staff paper from March 2026 explores options for further balance sheet reduction, signaling awareness of limited tools under the current ample reserves framework. CBO projections similarly highlight large structural deficits persisting through the decade. The combination of high systemic leverage, an opaque private credit ecosystem intertwined with CRE and regional banks, and inflation that refuses to fully subside creates a policy bind with few clean historical parallels. Potential paths include orderly deleveraging—which could prove painful given debt levels—or renewed intervention that might unanchor inflation expectations. While markets have shown resilience, underlying interconnections suggest fragility that a modest downturn could expose more fully. External shocks, such as oil-driven inflation, further reduce policy flexibility.

Liminal Observer: The intersection of sticky inflation, leveraged private markets, and fiscal dominance is narrowing the Fed's room to maneuver, increasing the odds of either a disorderly deleveraging or a return to large-scale intervention that could destabilize long-term expectations.

Sources (7)

- [1]Consumer Price Index - February 2026(https://www.bls.gov/news.release/pdf/cpi.pdf)

- [2]Federal Reserve issues FOMC statement(https://www.federalreserve.gov/newsevents/pressreleases/monetary20260318a.htm)

- [3]Janet Yellen warns the $38 trillion national debt is testing a limit(https://fortune.com/2026/01/05/janet-yellen-warns-38-trillion-national-debt-fiscal-dominance-eric-leeper-heather-long/)

- [4]Federal Reserve, Powell face challenges in 2026(https://www.cnbc.com/2026/01/03/federal-reserve-powell-face-challenges-in-2026.html)

- [5]Private credit could be the next crisis. How worried should you be?(https://www.cnbc.com/2026/03/11/private-credit-could-be-the-next-crisis-how-worried-should-you-be-.html)

- [6]2026: The Real Estate Debt Super-Cycle(https://www.dws.com/insights/research/real-estate-research/2026-the-real-estate-debt-super-cycle/)

- [7]The Budget and Economic Outlook: 2026 to 2036(https://www.cbo.gov/publication/62105)