Stuck in the Lock: Goldman Forecast and Broader Data Signal Prolonged Housing Affordability Drought Through 2027

Credible forecasts from Goldman Sachs, Fannie Mae, and industry groups confirm elevated mortgage rates and sticky prices will keep housing affordability strained into 2027, driven by lock-in effects and incomplete supply relief.

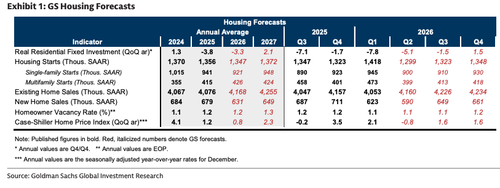

Goldman Sachs economist Ronnie Walker’s mid-year housing outlook paints a sobering picture for prospective buyers: mortgage rates are projected to hold near 6.43% through the end of 2026 before easing only modestly to around 6.3% in 2027, while national home prices continue their gradual climb. This combination sustains an ultra-low-turnover market dominated by the “lock-in” effect, where roughly 80% of existing mortgage holders enjoy rates well below current market levels. Existing home sales are expected to reach just 4.2 million in 2026—22% below 2019 levels—before inching to 4.3 million the following year. Residential investment has already contracted, and single-family starts are moderating even as the longstanding shortage eases only gradually.

Independent forecasts align closely. Fannie Mae and multiple bank economists anticipate 30-year fixed rates hovering between 6.3% and 6.5% through 2027, with limited relief from Federal Reserve policy. The National Association of Realtors notes that while inventory is rising modestly and the lock-in effect is slowly decaying, sales remain suppressed. Broader analyses highlight how elevated rates and constrained supply have entrenched a structural affordability crisis, transferring wealth from new buyers and renters toward existing homeowners via inflated asset values and reduced mobility. Policy choices around prolonged high rates and slow permitting/supply responses have amplified these dynamics, creating persistent barriers to wealth-building for younger cohorts and exacerbating intergenerational divides.

Goldman Sachs / Ronnie Walker: Persistent rate lock-in and modest price growth will keep millions sidelined, accelerating wealth concentration among current owners while new entrants face prolonged barriers.

Sources (5)

- [1]Goldman Sachs Mid-Year Housing Outlook (via Calculated Risk)(https://calculatedrisk.substack.com/p/goldmans-mid-year-housing-outlook)

- [2]Mortgage Rates Forecast 2026–2027: Expert Predictions(https://www.forbes.com/advisor/mortgages/mortgage-interest-rates-forecast/)

- [3]2026 Real Estate Outlook - NAR(https://www.nar.realtor/news/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching)

- [4]Fannie Mae Housing and Mortgage Forecast(https://www.fanniemae.com/data-and-insights/forecast)

- [5]Easing mortgage 'lock-in effect' could boost housing(https://finance-commerce.com/2026/01/mortgage-rates-above-6-percent-lock-in-effect-easing/)