China's Enduring Rare Earth Chokepoint: Why US Defense and Tech Sovereignty Remain a Decade Away

Despite heavy investments, the US faces at least until 2035 to reduce dependence on China for critical heavy rare earths like dysprosium and terbium, exposing enduring vulnerabilities in defense systems, EVs, renewables, and broader tech decoupling amid rising US-China tensions.

A new Bloomberg investigation reveals the United States is unlikely to meaningfully loosen China's stranglehold on heavy rare earth elements until at least the mid-2030s, despite billions in Pentagon funding, policy pledges, and allied efforts. Heavy rare earths such as dysprosium and terbium—critical for high-performance permanent magnets in F-35 fighter jets, nuclear submarines, precision missiles, electric vehicle motors, and wind turbines—highlight a persistent strategic vulnerability that directly undermines American claims of defense and technological independence. While light rare earth progress is faster, forecasts from McKinsey, CRU Group, and Benchmark Mineral Intelligence indicate non-Chinese sources will satisfy less than 20% of global dysprosium and terbium demand by 2035.[1][2]

The challenge extends far beyond mining. China's near-total dominance of refining and separation—controlling approximately 90-99% of heavy rare earth processing capacity—stems from decades of state-backed investment, technical expertise accumulated since the 1980s, and export controls on processing technologies. Producing ultra-pure materials can require over 1,000 chemical stages, creating high barriers for Western entrants facing environmental regulations, skilled labor shortages, and volatile pricing that previously bankrupted non-Chinese projects. Lynas Rare Earths, the primary non-Chinese heavy rare earth refiner supported by US defense contracts, produced just eight tons of combined dysprosium and terbium in early 2026 against annual global demand measured in thousands of tons. New projects in the US, Australia, and Brazil offer incremental gains but face significant scaling delays in mining, refining, and magnet manufacturing.[1][3]

This timeline connects to deeper, often overlooked linkages in great power competition. China's April 2025 export controls on dysprosium, terbium, and related elements—explicitly tied to US tariffs—demonstrated how Beijing can weaponize this leverage during trade disputes or potential crises over Taiwan, directly impacting the US defense industrial base and green energy goals. A Council on Foreign Relations analysis notes that even "friendshoring" with allies cannot rapidly close the expertise and infrastructure gap, as Western environmental and permitting hurdles contrast with China's integrated industrial policy. This vulnerability intersects with semiconductor and AI supply chains: rare earth magnets enable the advanced motors and sensors underpinning next-generation defense systems and data centers, meaning delayed independence weakens overall technological decoupling efforts.[2][4]

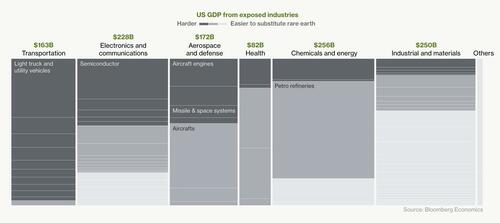

Fortune and Global Policy Watch reports further contextualize how China's 70% mining share and near-monopoly on heavy rare earth separation create cascading risks across $1.2 trillion in US-linked industries. Past price volatility and Beijing's willingness to restrict flows expose the limits of reactive US policy. Rather than a simple resource issue, this represents a structural asymmetry in industrial statecraft: while Washington announces initiatives, China continues refining its dominance through 2026-2030 planning. The result is a decade-long window of exposure that could force difficult choices on stockpiling, accelerated (and expensive) domestic subsidies, or concessions in future geopolitical flashpoints.[5][6]

LIMINAL: A decade-plus reliance on Chinese heavy rare earths creates a exploitable strategic chokepoint that could paralyze US military production and green tech scaling during any major escalation, revealing the gap between political rhetoric on independence and the harsh realities of industrial reshoring.

Sources (4)

- [1]US Needs Another Decade to Fix $1.2 Trillion Rare Earth Crisis(https://www.bloomberg.com/graphics/2026-us-china-heavy-rare-earth-magnets-defense/)

- [2]Leapfrogging China's Critical Minerals Dominance(https://www.cfr.org/reports/leapfrogging-chinas-critical-minerals-dominance)

- [3]Beijing's dominance in rare earth processing leaves others vulnerable(https://fortune.com/2026/03/11/china-us-rare-earth-processing-critical-minerals/)

- [4]Heavy Rare Earth Elements: Rising Supply Chain Risks and Emerging Policy Responses(https://www.globalpolicywatch.com/2026/02/heavy-rare-earth-elements-rising-supply-chain-risks-and-emerging-policy-responses/)