Subdued Consumer Credit Expansion Hints at Household Caution and Implications for Consumption-Driven GDP

February consumer credit rose below expectations, led by notably weak revolving credit growth, signaling potential softening in household finances and slower consumption that could weigh on GDP and shape Federal Reserve policy choices.

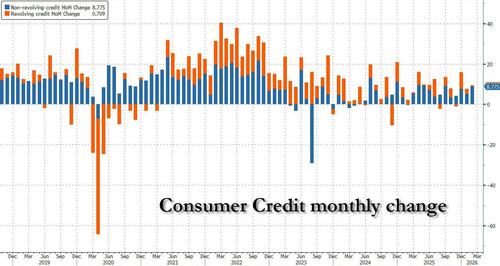

The Federal Reserve's G.19 Consumer Credit statistical release for February showed total credit increasing by $9.484 billion, below the $10.25 billion consensus and only modestly above the prior month's downward-revised $7.665 billion. Revolving credit (primarily credit cards) rose just $709 million—the weakest gain since November—while non-re revolving credit, including auto and student loans, advanced $9.2 billion to a record $3.789 trillion. This print aligns with the editorial lens that below-trend growth and tepid credit-card usage reflect softening household finances with potential downstream effects on personal consumption expenditures, which comprise roughly 70 percent of U.S. GDP per Bureau of Economic Analysis (BEA) national income accounts.

The ZeroHedge summary accurately notes post-2025 stabilization after earlier volatility and the recent decline in average credit-card interest rates to 21.52 percent as of March 31, yet it underplays longer-term patterns visible in primary data. The New York Fed's Household Debt and Credit Report for Q4 2025 documented aggregate household debt surpassing $17.5 trillion, with credit-card balances still elevated relative to 2019 levels and early signs of rising delinquencies in the 90+ day category. What the original coverage missed is the divergence: while non-revolving debt (student loans at $1.838 trillion) continues its mechanical upward path tied to federal lending programs, the stagnation in revolving credit suggests households are actively limiting new borrowing amid sticky high rates, even after the Fed's 175 basis points of cuts since September 2024.

Synthesizing the Fed's G.19, the BEA's January personal income and outlays release showing moderating real PCE growth, and the New York Fed's delinquency trends reveals connections often overlooked. Retail sales data have similarly disappointed in recent months, indicating that consumption—the primary growth engine—may be losing momentum faster than headline employment figures suggest. Two perspectives emerge from primary sources: Federal Reserve officials, as reflected in recent Beige Book anecdotes, have noted "signs of consumer pullback" in several districts, viewing subdued credit growth as consistent with their dual-mandate data-dependent framework. In contrast, Treasury market pricing and some Committee members' projections imply that weaker consumption could tilt the balance toward additional easing if labor markets soften further. A third reading from the Financial Accounts of the United States (Z.1 release) shows household net worth still supported by asset prices, suggesting any deleveraging may be precautionary rather than distress-driven.

The original piece correctly flags the credit-card rate drop but does not connect it to banks adjusting pricing in anticipation of regulatory scrutiny and possible further policy loosening. Nor does it address how this credit dynamic feeds into Fed policy deliberations ahead of forthcoming FOMC meetings, where consumption metrics increasingly compete with inflation persistence as decision inputs. Overall, the data point to a gradual normalization of household leverage that bears watching as an input rather than an immediate crisis signal.

MERIDIAN: Below-trend consumer credit growth and especially subdued revolving credit usage suggest households are retrenching, which could slow consumption—the largest GDP component—and lead the Fed to weigh additional easing against remaining inflation risks.

Sources (3)

- [1]Federal Reserve G.19 Consumer Credit(https://www.federalreserve.gov/releases/g19/current/default.htm)

- [2]NY Fed Quarterly Report on Household Debt and Credit(https://www.newyorkfed.org/microeconomics/hhdc.html)

- [3]BEA Personal Income and Outlays(https://www.bea.gov/data/income-saving/personal-income)