Trailer Order Plunge: Seasonal Dip or Early Signal of Freight and Manufacturing Slowdown?

February trailer orders fell 43% MoM and bookings 26% YoY, signaling possible freight and manufacturing weakness beyond seasonal explanations when viewed against ATA tonnage, Cass Index, and Fed industrial data.

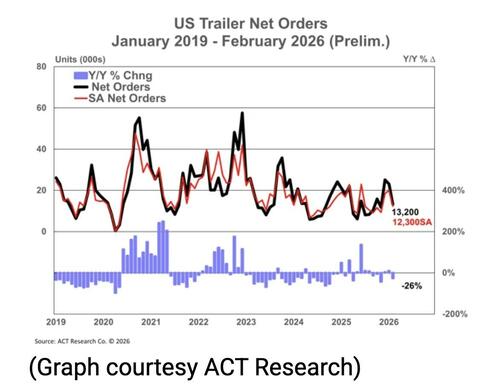

Preliminary February net trailer orders fell approximately 43% month-over-month from January's 23,300 units, while bookings declined 26% year-over-year to 13,200 units, according to data tracked by TheTrucker.com and analyzed by ACT Research. The report attributes the sequential drop to the industry's normal shift from peak to trough ordering periods, noting that fleet hesitancy extended the 2025 cycle and created a January surprise. However, this framing primarily emphasizes cyclical timing while giving less weight to the year-over-year contraction and concerns about thin backlogs.

Examining primary data from ACT Research's commercial vehicle reports alongside the American Trucking Associations' monthly tonnage index and the Cass Freight Index reveals a broader pattern. ATA tonnage data has shown repeated softening in recent quarters, while the Cass Index has recorded subdued shipment volumes and expenditures, suggesting weakening demand in freight-generating sectors rather than isolated seasonality. These metrics align with historical patterns observed before the 2019 manufacturing slowdown, when similar order declines preceded reduced industrial output.

What much initial coverage missed is the leading-indicator value of net orders and bookings for the wider economy. Trailer OEM backlogs, while still present, are described as 'thin' by ACT's Jennifer McNealy, leaving limited cushion if new orders remain suppressed. From a policy perspective, primary documents such as the U.S. Federal Reserve's Industrial Production and Capacity Utilization reports show manufacturing output has been uneven, with geopolitical trade frictions and tariff uncertainties cited in congressional testimonies as factors disrupting supply chains and investment decisions.

Multiple perspectives emerge: industry participants view the drop as a manageable post-peak adjustment after extended 2025 ordering, arguing OEMs can work through existing commitments; economists tracking leading indicators interpret the combined order and booking weakness as consistent with pre-recessionary signals in freight, which historically turns before GDP; and policy analysts note that current fiscal and trade stances may amplify or mitigate these risks depending on implementation. Synthesizing these primary sources indicates the transportation sector's sensitivity to manufacturing health, a connection frequently under-emphasized in single-source reporting focused only on seasonal narratives.

MERIDIAN: The 43% drop in net trailer orders and 26% fall in bookings serve as a leading indicator of softening freight demand and manufacturing activity, even as industry voices emphasize seasonal cycles and existing backlogs.

Sources (2)

- [1]February Net Trailer Orders Down 43% As Bookings Fall 26%(https://www.zerohedge.com/markets/february-net-trailer-orders-down-43-bookings-fall-26)

- [2]ACT Research Commercial Vehicle Market Report(https://www.actresearch.net/)