Mass-Market Oral GLP-1s: The Underreported Structural Shift in Public Health and Pharma Economics

Analysts at Goldman Sachs, JPMorgan, and IQVIA project the GLP-1/obesity drug market to reach $95-200 billion by 2030 as oral formulations like Novo Nordisk's Wegovy pill achieve strong launches, attract needle-averse patients, expand internationally, and gain Medicare traction. This signals a lasting shift toward accessible, volume-driven treatment with major but underreported implications for public health outcomes and pharmaceutical business models beyond near-term stock movements.

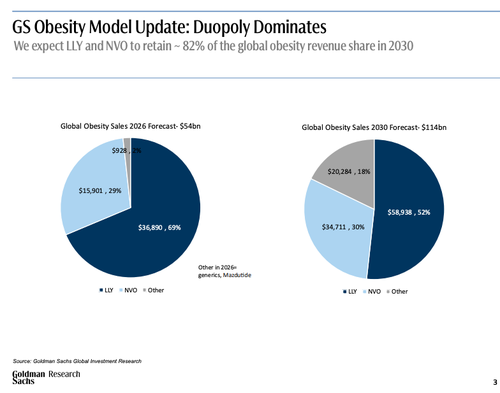

While financial media cycles obsess over Novo Nordisk's stock trajectory and quarterly earnings volatility, a deeper transformation is underway in the GLP-1 space. Goldman Sachs analysts recently upgraded their 2030 global anti-obesity drug TAM forecast to $114 billion from a prior $101 billion, driven primarily by faster-than-expected adoption of oral formulations, stronger international demand, Medicare expansion, and improving affordability. This aligns with broader analyst views that oral GLP-1 pills are moving obesity treatment from a niche, high-priced injectable market into something closer to mass-market medicine.[1][2]

Key drivers include orals capturing roughly 25-40% of the market by decade's end (Goldman previously modeled 25%; real-world momentum has pushed expectations higher). Novo Nordisk's oral Wegovy pill (oral semaglutide) has shown explosive early uptake since its January 2026 launch, generating over 600,000 prescriptions in the first two months and drawing in new patients who previously avoided injectables due to needle phobia or preference for daily pills. CNBC reporting highlights patients like those citing needle aversion now entering the GLP-1 category for the first time, expanding the total addressable population rather than merely cannibalizing injectable sales.[3]

This shift carries profound public health implications that receive less attention than stock noise. By lowering barriers to entry with pills priced as low as $149/month for starter doses in self-pay channels and broader insurance/Medicare coverage expected (potentially unlocking millions more patients from July 2026 onward via GLP-1 MFN deals), treatment penetration could rise substantially in both the US and ex-US markets. JPMorgan forecasts the broader incretin/GLP-1 market reaching $200 billion by 2030, with orals and generics accelerating global access. IQVIA and other models project $105-200 billion ranges, underscoring volume growth offsetting price erosion.[4]

Pharma economics are being rewritten. Goldman notes a 20% reduction in assumed US DTC pricing, a higher oral mix, and OUS sales climbing to $48 billion. Eli Lilly and Novo Nordisk are still projected to command ~82% global share through dominance in both injectables and orals (with Wegovy pill and Lilly's oral candidate leading). Yet the move toward daily orals at lower price points per patient signals a volume-over-margin model long-term. International ramps, particularly in China and other price-sensitive markets, plus Medicare's 17-million-patient opportunity, further broaden the pool. Reports from Reuters indicate analysts have tempered peak expectations due to competition and pricing pressure, but the consensus direction remains upward as orals democratize access.[2]

Mainstream coverage has underplayed these long-term dynamics in favor of short-term share shifts between Novo and Lilly or trial readouts. The real story is a potential inflection in metabolic disease burden: greater treatment of obesity could reduce comorbidities (type 2 diabetes, cardiovascular disease), yielding GDP gains and lower overall healthcare costs, as hinted in related Goldman and ITIF analyses. Challenges remain—adherence, GI side effects, and long-term outcomes require monitoring—but the transition from injectable exclusivity to mass-market orals represents one of the most significant public health and pharmaceutical market restructurings in decades. Oral GLP-1s are not just another drug class; they are infrastructure for treating obesity at societal scale.

LIMINAL: Oral GLP-1 pills are quietly turning a high-margin injectable niche into broad-access mass-market therapy, likely expanding treatment to tens of millions more people worldwide, easing obesity-related disease burdens, pressuring pricing, and forcing pharma to adapt to higher-volume, lower-per-patient economics while mainstream focus stays on quarterly stock noise.

Sources (4)

- [1]The anti-obesity drug market may prove smaller than expected(https://www.goldmansachs.com/insights/articles/the-anti-obesity-drug-market-may-prove-smaller-than-expected)

- [2]Novo Nordisk's Wegovy pill launch draws new wave of patients to GLP-1s(https://www.cnbc.com/2026/04/07/novo-nordisks-wegovy-pill-launch-draws-new-wave-of-patients-to-glp-1s.html)

- [3]Obesity market sales potential tightens as Novo and Lilly enter new era(https://www.reuters.com/business/healthcare-pharmaceuticals/obesity-market-sales-potential-tightens-novo-lilly-enter-new-era-2026-02-02/)

- [4]How Supply and Demand for Weight Loss Drugs is Playing Out(https://www.jpmorgan.com/insights/global-research/current-events/obesity-drugs)