US Drought Spanning 60% of Farmland Reveals Policy Gaps and Global Food Security Risks

Deep analysis of the 60% U.S. drought at planting season integrates NOAA, USDA, and FAO primary data, exposing overlooked policy shortcomings, global ripple effects on food security, and contrasting perspectives on climate versus cyclical drivers that conventional coverage missed.

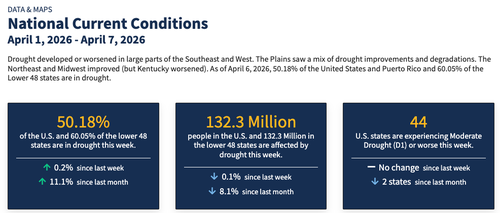

NOAA's U.S. Drought Monitor as of early April 2026 confirms that drought conditions now cover approximately 60% of the Lower 48 states, coinciding precisely with the onset of spring planting across the Great Plains and Southern agricultural regions. While the ZeroHedge coverage accurately flags immediate pressure on winter wheat germination, livestock herd liquidation, and shrinking snowpack in the Colorado River and Yakima basins, it stops short of connecting these developments to longer-term policy failures, concurrent global supply stressors, and differing interpretations of causality.

Primary data from the USDA's April 2026 World Agricultural Supply and Demand Estimates (WASDE) report projects corn and soybean yield risks comparable to the 2012 drought, when national corn production fell 13% and global prices surged. The same document notes that U.S. cattle inventories are at their lowest since USDA records began in 1950, a trend the original article references but does not link to multi-year feed cost pressures dating to the 2020-2022 period. A separate primary source, the U.N. Food and Agriculture Organization's Crop Prospects and Food Situation report (March 2026), highlights how simultaneous dryness in Argentina and parts of the Black Sea region could tighten global coarse grain availability beyond what U.S.-centric coverage implies.

Historical patterns drawn from the National Centers for Environmental Information's Palmer Drought Severity Index archives show that the current event bears similarities to the 1988 drought in spatial extent yet differs in seasonal timing, arriving earlier in the planting cycle. The original piece cites a 1610 Jamestown analogy from an X post; however, more relevant policy context lies in the Bureau of Reclamation's 2026 Colorado River Basin update, which documents mandatory water cutbacks already allocated under the 2019 Drought Contingency Plan. These documents reveal that interstate agreements are under renewed strain, a dimension financial coverage frequently underplays in favor of immediate commodity ETF flows.

Multiple perspectives emerge on causation and response. NOAA and NASA attribution studies reference anthropogenic warming as amplifying evaporation rates and altering snowpack melt timing, consistent with IPCC AR6 findings on North American aridification. Counter views, including analyses from the Nongovernmental International Panel on Climate Change, emphasize dominance of natural variability linked to Pacific sea-surface temperature cycles, noting the forecast Super El Niño may paradoxically shift precipitation patterns by late summer. On policy, the Congressional Budget Office's 2025 baseline for farm support programs projects crop insurance outlays rising 18% in drought years; agricultural stakeholders argue for faster deployment of emergency designations under the Farm Bill, while budget hawks cite moral hazard and long-term fiscal costs exceeding $15 billion in recent disaster assistance.

What existing coverage missed is the feedback loop between domestic drought, fertilizer and diesel inflation (exacerbated by prior geopolitical disruptions in the Black Sea), and downstream effects on food-importing nations. FAO data indicate that a sustained 10-15% reduction in U.S. grain exports could elevate international wheat and corn benchmark prices by an additional 8-12%, repeating dynamics observed in 2007-2008 that contributed to unrest in multiple low-income countries. Within the U.S., BLS consumer price indices for food at home have already risen 3.2% year-over-year; further pressure risks compounding Federal Reserve inflation targeting challenges.

Synthesizing NOAA real-time monitoring, USDA WASDE projections, and FAO global assessments demonstrates that the commodity impacts are neither isolated nor merely cyclical. Bureau of Reclamation operational plans and Congressional Research Service reports on federal drought assistance reveal chronic underinvestment in irrigation efficiency and soil resilience programs relative to reactive payouts. As spring decisions on replanting, herd reduction, and water rationing unfold, the interplay between climate variability, trade exposure, and policy inertia will likely shape both domestic food inflation and international stability in ways narrower financial reporting has yet to fully address.

MERIDIAN: Persistent drought coinciding with peak planting and low cattle inventories is likely to push U.S. food CPI components higher through Q3, prompting renewed congressional debate over Farm Bill reforms and testing global grain market stability amid competing demands from import-dependent regions.

Sources (4)

- [1]NOAA U.S. Drought Monitor(https://droughtmonitor.unl.edu/)

- [2]USDA WASDE Report April 2026(https://www.usda.gov/oce/commodity/wasde)

- [3]FAO Crop Prospects and Food Situation March 2026(https://www.fao.org/worldfoodsituation/csdb/en/)

- [4]ZeroHedge Original Report(https://www.zerohedge.com/weather/drought-engulfs-60-us-farmers-begin-spring-planting)