Geopolitical Energy Shocks Test Inflation Anchors as NY Fed Survey Signals Sticky Price Risks

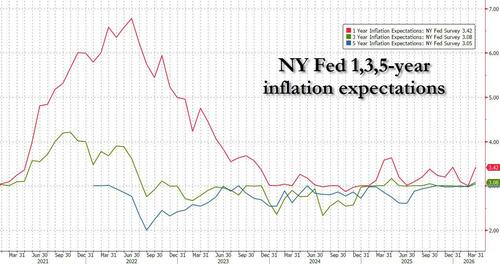

NY Fed March survey records one-year inflation expectations rising to 3.42% on gas-price fears linked to Iran conflict, with stable five-year expectations at 3.0%. Deteriorating labor and financial sentiment accompany the move, raising questions about sticky inflation and potential delays to rate cuts.

The New York Fed's March Survey of Consumer Expectations documents a sharp rise in one-year-ahead inflation expectations to 3.42 percent from 3.0 percent, matching highs not seen since April 2025. The survey explicitly ties this increase to a 5.3 percentage point jump in expected gasoline price growth to 9.4 percent. Three-year expectations edged up 0.1 percentage point to 3.1 percent while five-year expectations remained unchanged at 3.0 percent. Concurrently, households raised their mean perceived probability of higher unemployment over the next year by 3.6 points to 43.5 percent, the highest since April 2025, and reported deteriorating current and expected financial situations.

The ZeroHedge summary accurately reports these movements but underplays the survey's methodological grounding in a rotating panel of approximately 1,300 households and fails to connect the gas-price channel to primary energy-market data. The U.S. Energy Information Administration's March Short-Term Energy Outlook directly attributes recent gasoline price volatility to supply risks stemming from heightened Iran-Israel tensions and potential disruptions in the Strait of Hormuz, which carries roughly 20 percent of global seaborne crude. By contrast, the NY Fed's own press release and microdata files show the inflation-expectation jump is broad-based across income and education cohorts yet coexists with a decline in one-year earnings growth expectations to 2.4 percent, below the 12-month average.

This combination reveals patterns observed in primary documents from prior episodes. The Federal Reserve's 2022 Summary of Economic Projections and contemporaneous FOMC minutes repeatedly flagged risks of de-anchored expectations following the 2022 energy price spike after the Ukraine invasion. Similarly, the IMF's April 2025 World Economic Outlook flagged "geopolitical fragmentation" as an upside risk to inflation forecasts, citing Middle East supply disruptions as a transmission channel. These primary sources together indicate that transitory shocks can become sticky when households adjust wage and spending behavior.

Original coverage also missed the divergence in labor-market perceptions: the mean probability of losing one's job rose to 14.4 percent while the perceived likelihood of finding new employment if laid off increased modestly to 45.9 percent, still below trend. This suggests consumers anticipate a weaker labor market without corresponding wage gains, a dynamic capable of compressing real incomes even if headline inflation moderates.

Multiple perspectives emerge from the data. Federal Reserve officials, as reflected in Chair Powell's March 2025 congressional testimony, continue to emphasize that longer-term expectations remaining at 3.0 percent support the view that inflation remains anchored, potentially allowing policy easing if actual CPI prints soften. Other analysts, including those cited in the St. Louis Fed's April 2025 Economic Synopses, caution that repeated short-term expectation spikes can gradually lift medium-term measures, citing empirical work on sticky-information models. The Brookings Institution's March 2025 analysis of SCE microdata similarly notes that households above age 60 and below $50,000 income drove much of the debt-payment concern increase to 12.3 percent, highlighting uneven transmission across demographics.

Synthesizing the NY Fed SCE release, the EIA's April 2025 petroleum status report, and the IMF's latest regional economic outlook demonstrates that the current episode is neither unprecedented nor isolated. Whether the 0.42 percentage point one-year jump proves transitory, as occurred after the 2022 peak, or initiates a new upward ratchet will depend on resolution of the underlying Iran-related supply risks and the Fed's communication of its reaction function. The data underscore that consumer belief formation remains a critical variable for both monetary policy transmission and broader economic stability.

MERIDIAN: Short-term inflation expectations have jumped on energy volatility tied to Iran tensions, yet long-term anchors hold; sustained elevation could prompt the Fed to hold rates higher for longer, weighing on growth and labor-market perceptions.

Sources (3)

- [1]NY Fed Survey of Consumer Expectations (March 2025)(https://www.newyorkfed.org/microeconomics/sce)

- [2]EIA Short-Term Energy Outlook April 2025(https://www.eia.gov/outlooks/steo/)

- [3]IMF World Economic Outlook April 2025(https://www.imf.org/en/Publications/WEO)