Housing Affordability as Structural Tension: Shelter Needs Collide With Asset Speculation Amid Credit Expansion

Analysis frames U.S. housing tensions as shelter-asset conflict enabled by credit policies and weak occupancy verification, contrasting enforcement approaches across jurisdictions while citing primary Fed data on fraud.

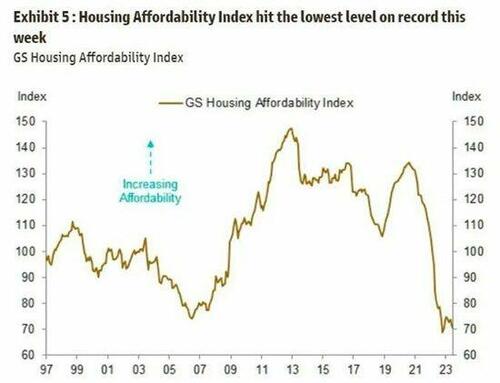

The Zero Hedge analysis highlights the incompatibility of treating housing simultaneously as essential shelter and a vehicle for parking credit-generated capital, drawing on Philadelphia Federal Reserve research documenting pervasive owner-occupancy fraud that sustains bubble dynamics. Primary data from the 2017 Philly Fed study 'Owner-Occupancy Fraud and Mortgage Performance' reveals occupancy misreporting rates exceeding 10 percent in sampled portfolios, enabling absentee ownership that distorts local supply without triggering regulatory audits due to privacy norms. This pattern extends beyond resort locales into urban centers, where rent-control regimes in jurisdictions like New York incentivize hoarding of below-market units, a mechanism absent from mainstream coverage focused on zoning alone. A contrasting perspective emerges from asset-market analyses, such as BIS working papers on post-2008 monetary accommodation, which frame housing appreciation as a natural outcome of low-rate environments that reward leveraged positions without inherent conflict. Yet these views rarely intersect with Japan's residency-tracking protocols, which treat dwelling occupancy as administrative data rather than private matter, exposing enforcement gaps that allow short-term rental proliferation to reach 15 percent of stock in high-demand areas. Broader bubble linkages appear in patterns connecting zero-day options trading excesses to parallel financialization of residential assets, where entities shielded by LLC structures evade detection and amplify price pressures decoupled from wage growth. Regulatory forbearance on mortgage verification thus sustains dual-market segmentation, with speculative demand outbidding shelter requirements in a manner that policy documents from the Federal Reserve's monetary policy reports acknowledge only indirectly through aggregate price indices.

MERIDIAN: Occupancy verification gaps and credit accommodation jointly sustain housing's dual valuation, with effects on supply allocation that standard indices understate.

Sources (3)

- [1]Owner-Occupancy Fraud and Mortgage Performance(https://www.philadelphiafed.org/the-economy/housing/owner-occupancy-fraud-and-mortgage-performance)

- [2]Choose One: Housing Is Shelter, Or Housing Is Just Another Asset In A Bubble Economy(https://www.zerohedge.com/economics/choose-one-housing-shelter-or-housing-just-another-asset-bubble-economy)

- [3]BIS Quarterly Review on Housing and Monetary Policy(https://www.bis.org/publ/qtrpdf/r_qt1709.htm)