Nuclear Buildout Beyond the Charts: AI Demand, Fossil De-Risking, and the Structural Reordering of Global Energy Security

China’s projected nuclear dominance reflects a deeper global shift driven by AI data-center power needs and efforts to reduce fossil fuel import risks. Original ZeroHedge coverage quantifies capacity but misses private-sector SMR deals, post-2022 de-risking policies, and long-term supply-chain geopolitics. Synthesizing IEA, IAEA, and World Nuclear Association primary data reveals under-appreciated market and security implications.

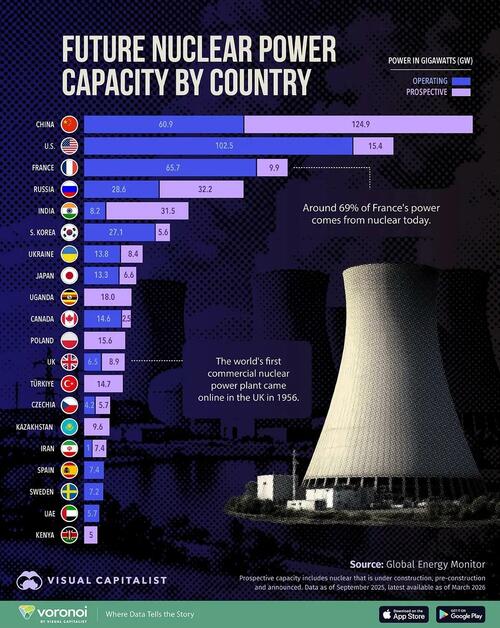

Data released by Global Energy Monitor and visualized by Visual Capitalist, as aggregated in ZeroHedge's September 2025 overview, projects China’s nuclear capacity rising from 60.9 GW today to 185.8 GW if all planned reactors come online, eclipsing the United States (projected 117.9 GW) and France (75.6 GW). While the ranking exercise is useful, it stops short of explaining the deeper drivers and misses the convergence of two structural forces: explosive AI and data-center electricity demand coupled with widespread governmental efforts to de-risk from volatile fossil fuel markets following the 2022 energy crisis.

Primary documents reveal patterns the original coverage under-emphasized. The International Energy Agency’s 2024 Nuclear Power report notes that hyperscale data centers could double their electricity consumption by 2026, with some forecasts from the U.S. Department of Energy’s National Laboratories indicating data centers alone may consume 8-12% of U.S. generation by 2030. Nuclear’s value here lies in providing firm, 24/7 low-carbon output that renewables supplemented by batteries cannot yet economically match at scale. This explains why Microsoft, Google, and Amazon have executed direct power purchase agreements and restart initiatives (Three Mile Island Unit 1, for example) that bypass traditional utility procurement.

Geopolitically, the post-2022 scramble to replace Russian pipeline gas has produced parallel policy signals. The European Commission’s REPowerEU plan and the U.K. government’s “golden age of nuclear” strategy paper both explicitly list nuclear as a tool of energy sovereignty. France’s long-standing fleet (69% of electricity) is being extended via lifetime upgrades documented in ASN regulatory filings, while Poland’s formal governmental program for six large reactors plus SMRs is framed as coal-exit strategy. Even Uganda’s 18 GW ambition, though early-stage, appears in IAEA technical cooperation documents as a development pathway for African states seeking to avoid perpetual fuel imports.

What existing coverage largely missed is the shift from megaproject gigantism toward mass-manufactured Small Modular Reactors. The U.S. Inflation Reduction Act’s nuclear production tax credit and the U.K.’s Great British Nuclear competition are designed explicitly for factory-built units that address the historic problems of cost overruns and decade-long build times documented in past OECD-NEA studies. China’s own Hualong One and planned Gen IV deployments combine state financing with supply-chain vertical integration, raising questions about future technology export influence that ZeroHedge’s piece does not address.

Historical patterns reinforce the analysis. The 1970s oil shocks triggered the last major nuclear wave; today’s AI shock plus net-zero mandates are producing a similar response, yet with faster approval pathways in several jurisdictions. Primary sources such as the IAEA’s Power Reactor Information System and the World Nuclear Association’s reactor database (updated October 2025) show that of the 60+ GW currently under construction globally, over half is in Asia, confirming a decisive eastward tilt.

Multiple perspectives exist on implications. Proponents, citing COP28’s declaration signed by 22 nations to triple nuclear capacity by 2050, argue this enhances grid stability and decarbonization without sacrificing growth. Critics, referencing unresolved high-level waste management plans in most countries and historical delays (Hinkley Point C, Flamanville-3), caution that optimistic schedules may not materialize and that proliferation risks could rise with expanded enrichment capacity. Uranium supply security also divides views: primary producer countries (Kazakhstan, Australia, Canada) hold leverage, yet secondary processing remains concentrated.

The long-term market ramifications remain undercovered. A nuclear fleet expanding at the projected pace could dampen volatility in electricity futures markets, alter LNG trade flows, and reposition uranium as a strategic commodity on par with rare earths. China’s dominance would extend beyond generation to reactor exports and fuel services, creating new dependencies even as Western allies attempt “friend-shoring” via initiatives like the U.S.-led Foundational Infrastructure for Responsible Use of Small Modular Reactors. These interconnections, visible in primary policy papers rather than secondary commentary, suggest the nuclear buildout is less an environmental sideshow and more a central pillar of emerging 21st-century energy statecraft.

MERIDIAN: The nuclear capacity surge, while framed around decarbonization, is structurally propelled by AI infrastructure’s baseload requirements and national strategies to escape fossil price shocks; primary policy documents suggest China’s lead will extend to technology standards and fuel services, quietly redrawing energy alliances by 2035.

Sources (3)

- [1]These Are The Countries Building The Most Nuclear Power(https://www.zerohedge.com/energy/these-are-countries-building-most-nuclear-power)

- [2]Nuclear Power in a Clean Energy System(https://www.iea.org/reports/nuclear-power-in-a-clean-energy-system)

- [3]World Nuclear Association - Plans for New Reactors Worldwide(https://world-nuclear.org/information-library/current-and-future-generation/plans-for-new-reactors-worldwide.aspx)