Geopolitical Oil Shocks Drive Market Pivot: Recession Risks Eclipse Inflation Concerns

Geopolitical escalation involving Iran and the Houthis has pushed oil above $100, prompting markets to price recession risks over inflation as evidenced by falling yields and rising gold despite the energy shock; analysis reveals historical parallels and stakeholder divergences missed in initial coverage.

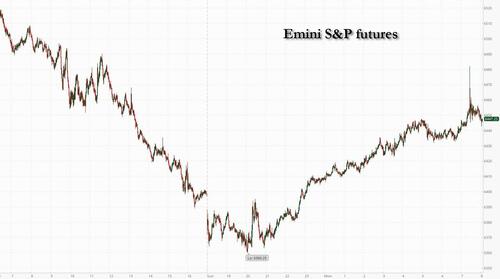

While the ZeroHedge dispatch captures immediate futures gains, falling Treasury yields, and rising gold and bitcoin amid Brent crude climbing above $100, the coverage centers on short-term positioning and select trader commentary without sufficiently exploring structural patterns or conflicting stakeholder views. Primary data from the U.S. Department of the Treasury yield curve shows the 10-year note declining 7 basis points to 4.36% and the 2-year falling to 3.87%, consistent with reduced expectations for sustained rate hikes as published on treasury.gov. CME Group futures settlement data similarly registers a clear shift toward recession pricing in equity and commodity contracts.

Synthesizing the ZeroHedge account with the International Energy Agency's April 2025 Oil Market Report (which documents supply risks through the Strait of Hormuz and Red Sea chokepoints potentially removing 5 million barrels per day) and the Bank for International Settlements' 2023 working paper on commodity price shocks reveals recurring historical dynamics. Parallel episodes—the 1990 Gulf War and the 2022 Russia-Ukraine energy disruption—demonstrated initial inflation spikes followed by demand destruction and growth slowdowns once higher energy costs transmitted to consumer and business confidence.

The original reporting understates several elements: the explicit Iranian Foreign Ministry statement rejecting direct talks with the U.S. and labeling demands 'excessive and illogical,' the absence of confirmed Houthi intent to fully close the Red Sea route, and divergent Wall Street interpretations. While Santander Asset Management and MPPM strategists emphasize growth drag eventually capping yield upside, other primary Fed communications and IMF assessments highlight risks of stagflation should supply shocks persist without offsetting fiscal or monetary accommodation. Goldman Sachs prime brokerage data on hedge-fund net exposure indicates capitulation-level selling, yet also notes potential for rapid short-covering upon any de-escalation.

Multiple perspectives emerge without consensus. U.S. administration statements, including reported comments on possible seizure of Kharg Island, frame the situation as leverage for energy security. Iranian officials counter that no substantive negotiations occurred in Pakistan. European asset managers view bonds as the clearest expression of macro repricing, whereas energy-sector participants see sustained high prices supporting cash-flow-heavy names. Emerging-market voices, per IEA demand forecasts, warn of sharper growth hits in oil-importing economies.

This episode illustrates how geopolitical shocks compel rapid investor repositioning—from inflation hedges to recession trades—without a predetermined endpoint. Asset allocation is shifting toward defensives, commodities, and liquid safe havens, yet the ultimate resolution hinges on diplomatic outcomes, OPEC+ responses, and central-bank reactions that remain fluid.

MERIDIAN: Geopolitical energy shocks are forcing investors to reprice growth risks faster than inflation, producing lower yields and safe-haven bids even as oil climbs; the durability of this pivot depends on whether supply disruptions persist or diplomatic progress materializes.

Sources (3)

- [1]Futures, Gold Jump As Yields Fall Despite Surging Oil As Recession Fears Surpass Inflation Concerns(https://www.zerohedge.com/markets/futures-gold-jump-yields-fall-despite-surging-oil-recession-fears-surpass-inflation)

- [2]Oil Market Report - April 2025(https://www.iea.org/reports/oil-market-report)

- [3]U.S. Treasury Yield Data(https://home.treasury.gov/resource-center/data-chart-center/interest-rates)