AI's Energy Hunger Exposes US Hardware Shortages and Geopolitical Supply Chain Risks

AI's explosive growth is driving a $65 billion boom in US power equipment by 2030, but hardware shortages and reliance on Chinese imports expose critical supply chain vulnerabilities. Beyond delays and cancellations, this crisis reflects historical manufacturing declines, unresolved policy conflicts, and geopolitical risks, with global competitors like the EU potentially gaining ground through sustainable strategies.

The rapid expansion of AI infrastructure is driving an unprecedented surge in energy demand, with a Wood Mackenzie report forecasting US spending on power generation equipment for data centers to reach $65 billion by 2030, up from $20 billion in 2023. This boom, fueled by the need for 110 GW of data center capacity by decade's end, is colliding with critical hardware shortages, particularly for transformers and switchgear, with lead times stretching 18-36 months. Beyond the numbers, this crisis reveals deeper vulnerabilities in the US tech sector's supply chain, heavily reliant on imports from China, and underscores a geopolitical tension that Washington has yet to resolve despite urgent policy rhetoric.

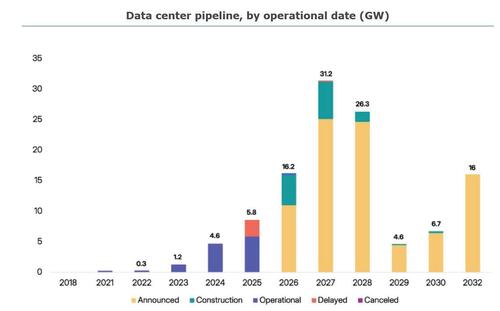

The original coverage by ZeroHedge highlights the transformer shortage and the resulting project delays—nearly half of the 16 GW of planned data center capacity for 2026 faces cancellation or postponement, per Sightline Climate data. However, it misses the broader historical context of US manufacturing decline in heavy electrical equipment, a trend dating back to the 1980s when domestic production was hollowed out by globalization. This is not a new problem but a chronic one, exacerbated by AI's sudden energy demands. Additionally, the coverage underplays the environmental and social trade-offs of 'behind-the-meter' solutions like small modular nuclear reactors (SMRs) or gas-fired plants, which hyperscalers are adopting to bypass grid delays. While these innovations address immediate needs, they raise questions about long-term sustainability and local community impacts, issues largely absent from the initial report.

Connecting this to broader patterns, the AI energy crunch mirrors past tech-driven resource races, such as the semiconductor shortage during the early 2020s, where geopolitical risks (e.g., Taiwan's dominance in chip production) similarly exposed US vulnerabilities. Here, reliance on Chinese imports for grid-critical hardware parallels that dependency, amplified by escalating US-China tensions. The Biden administration's invocation of the Defense Production Act in April 2023 to prioritize domestic manufacturing signals urgency, yet progress remains slow—domestic capacity cannot scale fast enough to meet AI-driven demand. A Department of Energy report from 2022 warned of these supply chain risks, noting that over 60% of large power transformers are imported, a statistic that remains relevant as hyperscalers like Amazon and Microsoft push for rapid data center expansion.

Moreover, the policy conflict is stark. The White House frames AI infrastructure as a national security imperative, likening it to a modern arms race, while simultaneously facing pressure to shield consumers from rate hikes driven by grid upgrades. The Ratepayer Protection Pledge, signed in March 2023, forces hyperscalers to fund their own infrastructure, but this risks slowing AI deployment—a trade-off between economic equity and strategic priority that remains unresolved. This tension also echoes historical energy policy dilemmas, such as the 1970s oil crisis, where national security clashed with domestic economic stability.

Finally, the global dimension deserves more attention. While the US grapples with hardware shortages, Europe is pursuing aggressive energy efficiency mandates for data centers under the EU Energy Efficiency Directive (revised 2023), potentially giving it a competitive edge in sustainable AI growth. Meanwhile, China's dominance in transformer production could be weaponized in a trade conflict, a risk heightened by recent US tariff hikes on Chinese goods. The intersection of AI's energy demands, supply chain fragility, and geopolitical rivalry suggests a looming crisis that neither policy nor industry is fully prepared to address.

MERIDIAN: The US will likely face intensified supply chain disruptions for AI infrastructure unless domestic manufacturing ramps up significantly by 2026. Without strategic investments, geopolitical risks tied to Chinese imports could delay critical tech advancements.

Sources (3)

- [1]Wood Mackenzie Report on US Power Equipment Market(https://www.woodmac.com/news/opinion/ai-data-center-boom-transformer-shortage/)

- [2]Department of Energy 2022 Report on Transformer Supply Chain(https://www.energy.gov/sites/default/files/2022-02/Large%20Power%20Transformer%20Study%20-%20Final.pdf)

- [3]EU Energy Efficiency Directive for Data Centers(https://energy.ec.europa.eu/topics/energy-efficiency/energy-efficiency-targets-directive-and-rules/energy-efficiency-directive_en)