Physical Oil Price Collapse Amid China's Import Slump Signals Deeper Global Energy Market Shifts

Physical oil prices have tumbled amid a sharp drop in Chinese crude imports and negative refiner margins, driven by Beijing’s energy security policies. This article explores missed implications for global energy markets, including demand slowdown risks, inflation impacts, and commodity trading strategies, drawing on historical patterns and broader economic indicators.

The unexpected tumble in physical oil prices, despite geopolitical tensions in the Strait of Hormuz, has left traders and analysts puzzled, particularly in light of China's contradictory signals on crude imports and domestic refining policies. While the original coverage by ZeroHedge highlights the plunge in Chinese crude imports to 8.2 million barrels per day in April—a multi-year low—and the record negative margins for independent 'teapot' refiners in Shandong province, it misses critical broader implications for global energy markets and potential economic undercurrents. This article delves into the nuances of China’s energy security policies, the impact on global oil demand forecasts, and the ripple effects on inflation and commodity trading strategies.

China’s domestic fuel policy, which prioritizes consumer price stability over refiner profitability to prevent social unrest, has forced teapot refiners to process crude at a loss. As reported, refining rates in Shandong spiked to a two-year high in April, even as margins cratered. This centrally planned approach, while ensuring short-term energy security, risks long-term sustainability for these refiners, many of whom have slashed purchases of Iranian crude in response. Vortexa data cited in the original piece notes a drop from 11.7 million barrels per day pre-war to the current 8.2 million, a swing equivalent to Japan’s total consumption. However, what’s underexplored is how this import collapse—coupled with rising commercial stockpiles and 16 million barrels idling off the Yellow Sea per Kpler data—signals a deliberate stockpiling strategy or a deeper demand slowdown in China’s economy.

Beyond the immediate policy clash, this situation reveals vulnerabilities in global energy markets. The International Energy Agency (IEA) in its April 2023 Oil Market Report warned of weakening Chinese demand growth as a key risk to global oil consumption forecasts, projecting a slowdown to 5.5% year-on-year compared to 7.2% in 2022. This aligns with broader economic indicators, such as China’s PMI slipping to 49.2 in March 2023, signaling manufacturing contraction (per China’s National Bureau of Statistics). The original coverage overlooks how these trends could exacerbate oversupply risks, especially as Saudi Arabia and UAE bypass Hormuz with alternative pipelines, and strategic petroleum releases from the US and Japan further ease supply constraints. The result could be sustained downward pressure on oil prices, challenging OPEC+ cohesion and influencing inflation expectations in major economies.

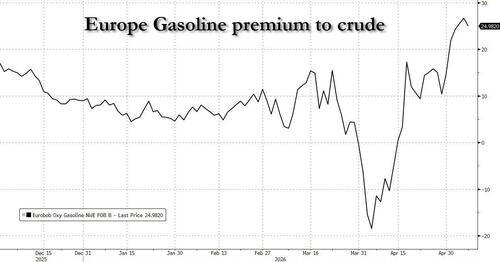

Moreover, the divergence between physical oil prices and futures—where Brent and WTI remain elevated due to geopolitical risk premiums—suggests a disconnect that commodity traders might exploit through arbitrage strategies. This discrepancy, unaddressed in the original piece, could reshape hedging behaviors and impact energy-intensive sectors globally. If Chinese demand remains subdued, or if Beijing continues to prioritize strategic reserves over imports, central banks in inflation-sensitive economies like the Eurozone and India may face unexpected relief on energy costs, potentially altering monetary policy trajectories.

What’s also missing from the initial reporting is the historical parallel to China’s actions during the 2014-2016 oil price crash, when Beijing similarly built strategic reserves during low-price environments while curbing imports. This pattern, documented in the US Energy Information Administration (EIA) archives, suggests a calculated move to leverage current market dynamics for long-term energy security. If confirmed, this could signal that China anticipates prolonged global oversupply or economic weakness, a perspective that traders and policymakers must factor into their strategies.

In synthesizing these insights, it’s clear that the physical oil price tumble is not merely a reaction to China’s domestic policies but a potential harbinger of broader economic shifts. The interplay of declining demand signals, strategic stockpiling, and geopolitical supply adjustments could redefine global energy market dynamics in the coming quarters, with implications far beyond China’s borders.

MERIDIAN: China’s import slump and stockpiling may signal a longer-term strategy to capitalize on low prices, potentially pressuring global oil markets further if demand recovery lags. This could ease inflation in energy-dependent economies but challenge OPEC+ unity.

Sources (3)

- [1]Traders Puzzled As Physical Oil Prices Tumble Amid Surging Chinese Crude Sales, Plunging Imports(https://www.zerohedge.com/markets/traders-puzzled-physical-oil-prices-tumble-amid-surging-chinese-crude-sales-plunging)

- [2]IEA Oil Market Report - April 2023(https://www.iea.org/reports/oil-market-report-april-2023)

- [3]EIA Analysis on China’s Strategic Petroleum Reserves (Historical Context)(https://www.eia.gov/international/analysis/country/CHN)