Moody's Negative Outlook on Blue Owl Highlights Redemption Runs and Liquidity Risks in $2 Trillion Private Credit Market

Moody's downgrade of Blue Owl's flagship fund amid record redemption requests signals mounting liquidity stress across private credit, driven by retail investor exits, AI impacts on software borrowers, and structural mismatches in non-traded BDCs. This reveals underappreciated systemic risks in shadow banking that extend beyond one firm.

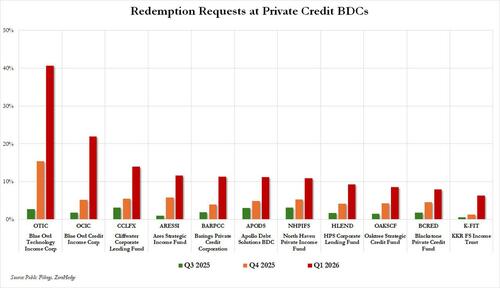

Moody's Ratings cut its outlook on Blue Owl Credit Income Corp (OCIC), a $36 billion non-traded business development company, to negative from stable, citing redemption requests significantly higher than peers in Q1 2026. The majority of requests came from a limited number of investors, raising concentration concerns in the equity holder base. Moody's expects elevated redemptions to continue, potentially eroding OCIC's strong capital and liquidity positions as inflows slow. This action aligns with Moody's broader revision of its outlook on U.S. BDCs to negative, citing rising redemption pressures, higher leverage, and weakening funding access.[1][2]

Blue Owl has become emblematic of stresses rippling through the private credit industry. Redemption requests hit 21.9% for OCIC (up sharply from 5.2% prior quarter) and a record 40.7% for its technology income fund. In response, the firm has limited withdrawals, sold assets (including to affiliated entities), and adjusted payout structures—moves that have drawn scrutiny over transparency, cherry-picking of assets, and potential delays in marking down valuations. A 20% drop in underlying asset values could breach key regulatory ratios, according to industry analysis.[3]

These events reveal deeper vulnerabilities in shadow banking. Private credit has ballooned to nearly $2 trillion, fueled by retail and high-net-worth investors channeled through non-traded perpetual BDCs. Unlike traditional institutional capital, retail investors prove less patient in volatility, creating liquidity mismatches: funds offer quarterly redemptions while holding illiquid loans, often to software and SaaS companies. AI-driven automation is disrupting these borrowers, contributing to rising defaults (estimated 5.8% and potentially heading to 8%), valuation opacity, and a classic run dynamic where early redeemers exit at reported NAV before potential writedowns.[4][5]

Congressional researchers note that redemption caps (typically 5% per quarter) are being tested industry-wide, with multiple major managers including Ares, Apollo, Blackstone, and Morgan Stanley imposing limits amid requests exceeding those thresholds. Over $4-5 billion in capital is reportedly trapped behind gates. While some frame this as a recalibration, the combination of concentrated retail exposure, interconnected leverage, and forced sales risks amplifying stress across credit markets. Mainstream coverage has often portrayed private credit as a stable alternative to traditional banking, yet these redemption runs underscore systemic fragilities long warned about in heterodox analyses of shadow finance—where opacity and first-mover incentives can rapidly escalate localized pressure into broader contagion.[6]

Blue Owl's stock has halved over the past year, reflecting investor skepticism. The episode serves as a stress test for the wealth channel's aggressive expansion into alternatives, highlighting how retail participation in illiquid private assets can introduce bank-run mechanics into non-bank lending.

[LIMINAL]: Redemption runs at Blue Owl and peers could expose liquidity illusions in retail-facing private credit vehicles, accelerating forced sales and valuation resets that ripple through shadow banking if AI-driven defaults in software lending intensify.

Sources (5)

- [1]Moody's cuts outlook on Blue Owl fund to 'negative' over surge in redemption requests(https://www.reuters.com/business/moodys-cuts-outlook-blue-owl-fund-negative-over-surge-redemption-requests-2026-04-08/)

- [2]Blue Owl Fund Outlook Cut to Negative by Moody’s on Redemptions(https://www.bloomberg.com/news/articles/2026-04-08/blue-owl-fund-outlook-cut-to-negative-by-moody-s-on-redemptions)

- [3]Private credit sector stresses could be catastrophic, but not just yet(https://www.reuters.com/business/finance/private-credit-sector-stresses-could-be-catastrophic-not-just-yet-2026-04-03/)

- [4]Private Credit Funds Redemption Restrictions(https://www.congress.gov/crs_external_products/IN/PDF/IN12674/IN12674.3.pdf)

- [5]Private credit's 'zero-loss fantasy' is ending as rising defaults spark investor exodus(https://www.cnbc.com/2026/03/25/private-credit-defaults-loan-quality-debt-risk-systemic-ai-disruption.html)