Anthropic's $100B AWS Pact: Symptom of Self-Reinforcing AI Capex Boom and Its Overlooked Geopolitical Infrastructure Ripples

Anthropic's $100B AWS commitment exemplifies a self-reinforcing AI capex cycle among tech giants that drives massive infrastructure spend, energy demand, and market concentration. Analysis connects the deal to parallel Microsoft-OpenAI and Google-Anthropic arrangements, highlights overlooked national security and grid impacts, and contrasts industry innovation arguments with antitrust and resource-allocation concerns using primary filings and IEA data.

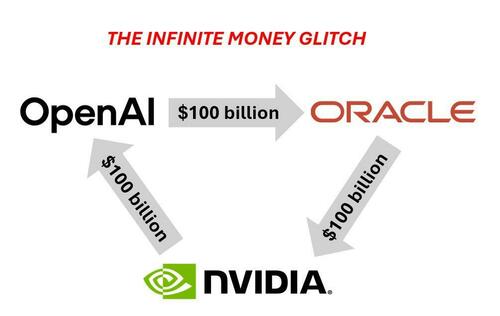

The ZeroHedge coverage correctly identifies the circular financing dynamic in which Amazon invests up to $25 billion in Anthropic while the AI developer commits more than $100 billion over ten years to AWS infrastructure, Trainium2/3 chips, and Graviton cores. However, labeling this an 'AI circle jerk' frames the transaction as isolated financial engineering and misses the broader self-reinforcing capex pattern now embedded across hyperscalers, its implications for U.S. energy policy, national security doctrine, and market structure.

Primary documentation from the April 2026 Amazon-Anthropic joint announcement and the White House readout of President Trump's meeting with Anthropic executives (released via Rapid Response 47) show explicit linkage between commercial infrastructure lock-in and government interest in dual-use AI capabilities. The announcement references Project Rainier, a cluster approaching half a million Trainium2 chips, and Anthropic's plan to deliver nearly 1 GW of capacity by end-2026. These figures align with patterns documented in Microsoft's FY2025 10-K filings, where capital expenditures exceeded $50 billion largely on AI-related infrastructure to support OpenAI workloads, and Google's separate multi-billion-dollar Anthropic investment first disclosed in 2023 SEC filings.

Mainstream transactional reporting typically treats each deal as discrete. What it misses is the feedback loop: hyperscalers fund AI labs, labs generate demand that justifies further hyperscaler capex on custom silicon and power infrastructure, which in turn attracts more sovereign and pension capital. This cycle concentrates compute capacity among three U.S.-headquartered cloud providers, raising questions about resilience and access that the Federal Trade Commission's ongoing cloud market inquiries (initiated 2024) have only begun to surface.

Energy demand constitutes another under-examined dimension. A 1 GW AI cluster consumes power equivalent to a mid-sized city's grid draw. The International Energy Agency's World Energy Outlook 2025 projects data centers could represent 6-8% of U.S. electricity demand by 2030, prompting parallel policy discussions in Department of Energy national transmission needs studies. Neither the ZeroHedge piece nor most business press connect Anthropic's 'sharp rise' in Claude usage and resulting infrastructure strain to these macro forecasts or to emerging FERC proceedings on data-center interconnection queues.

Geopolitically, the Trump administration's engagement with Anthropic occurs against the backdrop of Pentagon experimentation with large language models for operational planning, referenced in the 2025 National Defense Authorization Act's AI provisions and the earlier Biden Executive Order 14110 on Safe, Secure, and Trustworthy AI. Perspectives differ sharply: industry stakeholders argue such public-private alignment is essential to maintain technological edge over China's state-directed compute buildout (documented in CSIS supply-chain reports). Critics, including some antitrust scholars and energy analysts, contend the arrangement exacerbates market concentration, crowds out smaller developers, and locks the United States into an energy-intensive AI pathway that may complicate domestic climate and grid-modernization targets.

Synthesizing the Amazon-Anthropic announcement, Microsoft's capex disclosures, and the IEA Outlook reveals a structural shift: AI is no longer a software layer but a capital-intensive infrastructure arms race. The original coverage correctly flags the circularity yet understates how this pattern is co-evolving with U.S. policy on semiconductors, energy security, and military AI adoption, producing concentrated power that future regulatory or national security decisions must address.

MERIDIAN: This deal tightens the loop between hyperscaler capital, AI model demand, and U.S. national security priorities, likely accelerating policy debates on energy infrastructure permitting, cloud market oversight, and export controls within the next 18 months.

Sources (3)

- [1]Amazon and Anthropic Expand Strategic Collaboration(https://aws.amazon.com/blogs/aws/anthropic-and-amazon-expand-strategic-collaboration/)

- [2]IEA World Energy Outlook 2025(https://www.iea.org/reports/world-energy-outlook-2025)

- [3]Executive Order 14110 on Safe, Secure, and Trustworthy Artificial Intelligence(https://www.whitehouse.gov/briefing-room/presidential-actions/2023/10/30/executive-order-on-the-safe-secure-and-trustworthy-development-and-use-of-artificial-intelligence/)