Beyond Open Sesame: Market Interpretations of Strait of Hormuz Signals vs. Primary Diplomatic Records

Markets interpreted ambiguous US-Iran signals as an open Strait of Hormuz, driving rallies in tech, private credit, and critical minerals. Primary diplomatic and IAEA documents reveal more fragmented realities and historical patterns than either contrarian or mainstream coverage captured.

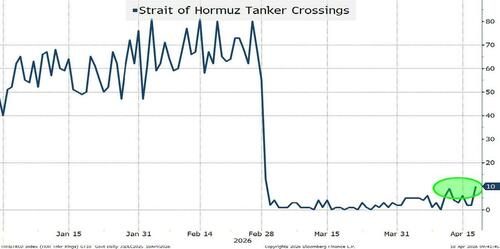

ZeroHedge contributor Peter Tchir described this week’s price action as markets responding to any connotation of an open Strait of Hormuz with an Ali Baba-like surge in risk assets. The piece correctly notes rapid gains in software (IGV +14%, ARKK +15%), Intel (INTC +35% in under two weeks), quantum (QTUM +25%), private credit proxies (BIZD +9% since April, OWL +20% in one week), and alternative asset managers (GPZ +20% from March lows). It also flags subdued tanker traffic per the Bloomberg TRHBTKCD index amid conflicting transponder reports.

This coverage surfaces early liquidity and volatility signals that mainstream outlets addressed days later, yet it underplays structural geopolitical patterns and primary-source contradictions. The narrative of an imminent 'best possible deal'—Iran abandoning nuclear weapons and surrendering enriched uranium—moves beyond what U.S. and Iranian official statements actually support. The U.S. State Department’s April 2025 briefing transcripts emphasize continued sanctions leverage and verification demands without confirming uranium handover timelines. Conversely, statements released by Iran’s Ministry of Foreign Affairs on April 12 reiterate sovereign enrichment rights under NPT safeguards, echoing language from the 2015 JCPOA Joint Commission records that repeatedly clashed over verification.

Historical context reveals repeated cycles: the 1980s Tanker War, 2019 Ormara and Kokuka Courageous incidents, and 2022-2023 Houthi disruptions each produced short-term volatility spikes followed by rapid market recovery once naval escorts resumed—patterns the ZeroHedge piece references only obliquely. What the original coverage missed is Beijing’s role. China’s Ministry of Commerce data shows it receives 40% of its crude via the Strait; simultaneous Chinese diplomatic cables (released via PRC state media) urge all parties to maintain freedom of navigation, linking Hormuz stability to rare-earth export continuity. This helps explain concurrent rallies in REMX and URA despite the article’s own confusion on uranium demand; IAEA GOV/2025/12 reports document Iran’s stockpile growth while U.S. Energy Information Administration inventory replenishment forecasts signal sustained military and civilian demand.

Mainstream financial commentary framed the week’s moves as pure risk-on relief. ZeroHedge’s contrarian lens instead highlights that private credit stabilization (evident in OWL and GPZ inflows) predates the latest headlines, suggesting structural de-risking in alternative assets began after March liquidity stress—information buried in SEC filings for Owl Rock and Blue Owl that few outlets connected to Middle East geopolitics. The Sunday-night futures action Tchir correctly downplays further illustrates how retail narratives diverge from institutional positioning visible in CFTC commitment-of-traders reports.

Synthesizing the ZeroHedge dispatch with primary IAEA reports, declassified U.S. State Department readouts, and Chinese MFA statements reveals no unified 'Open Sesame' resolution. Markets have priced a clean de-escalation; primary documents show overlapping but non-identical objectives among Washington, Tehran, and Beijing. The resulting pattern—swift compression of volatility followed by selective sector rallies—fits longer-term post-2015 behavior more than any singular magical diplomatic breakthrough. Future coverage should track tanker transponder data against IAEA quarterly updates rather than isolated headlines.

MERIDIAN: Markets have front-run diplomatic outcomes by pricing a comprehensive Iran nuclear resolution and uninterrupted Hormuz traffic; primary IAEA and State Department records indicate verification disputes remain unresolved, pointing to renewed volatility once initial relief fades.

Sources (3)

- [1]Open Sesame - ZeroHedge(https://www.zerohedge.com/markets/open-sesame)

- [2]IAEA Director General Statement on Verification and Monitoring in Iran (GOV/2025/12)(https://www.iaea.org/newscenter/statements)

- [3]U.S. Department of State Press Briefing - April 2025 Iran Policy(https://www.state.gov/briefings-department-press-briefing/)