Accenture's Record Plunge Signals AI-Driven Compression in High-Skill Consulting

Accenture's earnings miss and sharp stock drop, amplified by Morgan Stanley's downgrade, highlight how AI spending is displacing rather than expanding traditional consulting demand, pointing to wider white-collar automation risks in professional services.

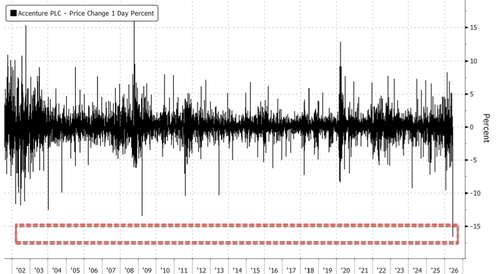

Accenture shares fell as much as 16-17% in after-hours and premarket trading following its fiscal Q3 2025 earnings release, marking one of the sharpest single-day drops on record for the firm. The company reported revenue of approximately $18.7 billion (slightly below estimates) with EPS growth of 9%, but issued Q4 revenue guidance of $17.75-18.4 billion, missing the Bloomberg consensus of $18.47 billion. New bookings declined to $19.3-19.7 billion year-over-year, with managed services particularly weak.[1][2]

Morgan Stanley downgraded Accenture to Equal-weight from Overweight, cutting its price target to $177 from $240. Analysts cited the absence of an expected budget inflection from AI investments, noting that enterprise AI spending is crowding out traditional discretionary IT projects rather than expanding overall IT services budgets (projected ~2% growth). This aligns with earlier warnings from Jefferies and reflects CIO survey data showing flat-to-low growth in broader tech spending.[3][4]

The selloff underscores a structural shift: generative AI and agentic tools are automating elements of strategy, implementation, and managed services that once required large teams of consultants. While Accenture reported strong GenAI-related bookings and revenue, overall demand signals weakness, echoing pressures across professional services. Reports highlight similar challenges at peers like Deloitte amid government spending caution and AI-driven efficiency gains, with firms exiting non-reskillable roles while hiring for AI orchestration capabilities.[5][6]

Broader data points to accelerating white-collar automation. Estimates suggest hundreds of millions of professional roles could be affected within five years, with consulting's junior-to-mid-level execution work particularly exposed as clients adopt internal AI agents for tasks previously outsourced. Accenture's own adjustments—layoffs tied to reskilling gaps alongside AI revenue growth—illustrate the transition, but investor skepticism persists on whether new AI services will fully offset margin compression in legacy lines. Analyst consensus remains predominantly Buy-rated with targets near $236, yet near-term volatility reflects uncertainty over the pace of demand recovery.

[LIMINAL]: AI is compressing traditional consulting margins faster than anticipated, forcing a pivot to AI orchestration services with uncertain revenue replacement timelines across high-skill professional services.

Sources (5)

- [1]Accenture Stock Plunge After Earnings and Outlook(https://finance.yahoo.com/quote/ACN/)

- [2]Accenture Downgraded by Morgan Stanley as AI Spending Crowds Out IT Services(https://finance.yahoo.com/sectors/technology/articles/accenture-downgraded-morgan-stanley-ai-174036267.html)

- [3]Accenture Leads S&P 500 Decliners as Bookings Fall Short(https://www.investopedia.com/accenture-q3-fy2025-earnings-11756058)

- [4]Accenture Reports Third-Quarter Fiscal 2025 Results(https://newsroom.accenture.com/content/3qfy25-earnings/accenture-reports-third-quarter-fiscal-2025-results.pdf)

- [5]AI and Trump Put Consulting Firms Under Pressure(https://www.axios.com/2025/08/10/ai-trump-deloitte-accenture-consulting)