Nuclear Renaissance: Barclays’ Bullish Stance Reflects Broader Shifts in Energy Investment and Geopolitical Strategy

Barclays’ bullish outlook on nuclear energy highlights a renaissance driven by decarbonization, energy security, and AI demand. This analysis goes beyond the report to explore overlooked geopolitical risks, labor bottlenecks, and the role of hyperscalers, connecting nuclear’s rise to broader green investment trends and EU strategic autonomy goals.

Barclays’ recent report on nuclear energy, maintaining a bullish outlook, underscores a pivotal moment in the global energy transition. The bank highlights a 'nuclear renaissance' driven by energy security concerns, decarbonization imperatives, and surging power demands from artificial intelligence (AI) infrastructure. This perspective aligns with broader trends in green technology investment, but it also reveals underexplored geopolitical and structural challenges that could shape the trajectory of nuclear adoption. Beyond the report’s focus on regulatory progress and market dynamics, this analysis examines the interplay of investment patterns, international policy, and systemic bottlenecks, identifying gaps in the original coverage.

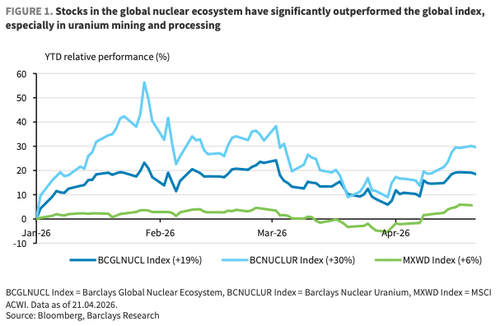

Barclays’ optimism is rooted in tangible developments: a 19% year-to-date increase in their global nuclear ecosystem index (BCGLNUCL) and a 30% surge in the nuclear fuel chain sub-index (BCNUCLUR). The report points to concrete progress in the fuel cycle, including revived uranium mining in the U.S. and major project advancements in Canada, bolstered by the U.S. Department of Energy’s $2.7 billion investment in enrichment capacity. Regulatory streamlining and licensing innovations further signal a shift from concept to construction. However, the original coverage glosses over critical nuances in global supply chain dependencies and the geopolitical risks tied to uranium sourcing, particularly as tensions with Russia—a key supplier—persist.

One overlooked dimension is how nuclear energy’s resurgence intersects with broader investment trends in capital-heavy sectors. Barclays notes a market rotation from capital-light to capital-heavy industries, dubbed 'HALO' sectors, reflecting investor appetite for infrastructure-intensive projects. This mirrors patterns seen in renewable energy financing over the past decade, where initial speculative investment eventually demanded proven returns—a dynamic Barclays acknowledges as investors now prioritize 'delivery of existing megawatts' over narrative-driven funding. This shift suggests nuclear energy is entering a maturation phase, akin to wind and solar in the early 2010s, but with unique geopolitical stakes due to its dual-use potential and resource scarcity.

The original report ties nuclear’s appeal to energy security, amplified by recent conflicts like the Iran war, which have exposed vulnerabilities in energy-dependent nations such as Germany and parts of Asia. France’s relative stability, thanks to its nuclear-heavy grid, is cited as a model. However, this narrative misses the deeper EU strategic autonomy agenda, which extends beyond energy to raw material access and technological independence. The European Commission’s 2023 Critical Raw Materials Act highlights uranium and rare earths as strategic priorities, signaling that nuclear’s revival is not just about power generation but also about reducing reliance on non-EU supply chains—a point Barclays underemphasizes.

Labor constraints, flagged by Barclays as a 'deeply structural' bottleneck, are another critical oversight in broader coverage. The report estimates a need for 300,000 engineers in the U.S. alone by 2030 to meet nuclear and related infrastructure demands. This challenge parallels historical shortages during the 1970s nuclear boom, where delays in plant construction often stemmed from workforce gaps rather than funding. Unlike supply chain issues solvable by capital infusion, labor requires long-term educational and policy interventions—areas where current U.S. and EU strategies remain vague, despite initiatives like the DOE’s workforce development grants.

Finally, the role of hyperscalers—tech giants like Meta, Microsoft, and Amazon—underwriting nuclear projects introduces a novel dynamic. Their involvement, driven by AI’s insatiable energy needs, positions nuclear as a linchpin of digital infrastructure. Yet, this trend raises questions about equity in energy access: will nuclear capacity prioritize corporate data centers over public grids? Barclays’ report does not address this tension, nor does it explore how such partnerships might influence regulatory capture or skew public investment.

Synthesizing additional sources, the International Energy Agency’s (IEA) 'World Energy Outlook 2023' projects nuclear capacity must double by 2050 to meet net-zero goals, aligning with Barclays’ bullishness but cautioning against overreliance on unproven small modular reactors (SMRs). Meanwhile, a 2024 U.S. Department of Energy report on uranium supply chains warns of persistent vulnerabilities due to concentrated global production, a risk Barclays mentions only in passing. Together, these perspectives suggest that while nuclear’s momentum is real, its path is fraught with systemic and geopolitical hurdles that demand more than market enthusiasm to overcome.

In conclusion, Barclays’ stance reflects a broader pivot toward sustainable, capital-intensive energy solutions amid climate and security pressures. However, the nuclear renaissance’s success hinges on resolving structural labor shortages, navigating geopolitical supply risks, and balancing corporate versus public energy priorities—issues that require deeper policy focus than current narratives suggest.

MERIDIAN: Nuclear energy’s momentum will likely face significant delays due to labor shortages and geopolitical supply chain risks, even as investment grows. Expect policy interventions to lag behind market enthusiasm, slowing the transition by 2030.

Sources (3)

- [1]Barclays Maintains Bullish Stance On Nuclear(https://www.zerohedge.com/energy/barclays-maintains-bullish-stance-nuclear)

- [2]World Energy Outlook 2023(https://www.iea.org/reports/world-energy-outlook-2023)

- [3]U.S. Department of Energy: Uranium Supply Chain Report 2024(https://www.energy.gov/ne/articles/doe-releases-report-uranium-supply-chain)