Intel's AI-Driven Surge Past 2000 Peak: Tracing the Semiconductor Supercycle and Concentration Risks in U.S. Industrial Policy

Intel's share price exceeding its 2000 dot-com peak reflects an AI-fueled semiconductor supercycle propelled by government policy via the CHIPS Act, yet primary documents reveal underappreciated risks from market concentration, Taiwan dependency, and U.S.-China tech decoupling that standard financial coverage has minimized.

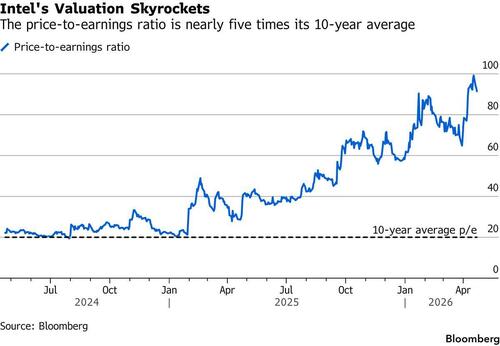

Intel's Q1 2025 earnings and upbeat Q2 guidance have propelled its shares past the August 2000 dot-com high, marking a striking turnaround from near-distress levels less than a year ago. While the ZeroHedge coverage accurately details the beats—Datacenter & AI revenue up 22% year-over-year to $5.05 billion, Foundry revenue up 16% to $5.42 billion, and Q2 revenue projected at $13.8-14.8 billion versus $13 billion expected—it frames the story primarily as a redemption arc for CEO Lip-Bu Tan and a straightforward beneficiary of AI infrastructure buildout. This misses the deeper interplay with U.S. geopolitical strategy, supply-chain vulnerabilities, and the structural concentration risks that define the current semiconductor supercycle.

Primary documents reveal a more nuanced picture. Intel's official Q1 2025 earnings release and accompanying SEC Form 10-Q explicitly tie the AI tailwinds to both cyclical demand and the effects of the CHIPS and Science Act of 2022. The White House's August 9, 2022, fact sheet on the CHIPS Act— which authorized $52.7 billion in incentives and $24 billion in tax credits—lists Intel among the largest recipients, with direct grants and loans supporting fabs in Arizona, Ohio, and New Mexico. These investments, combined with the company's reported 41% adjusted gross margin (still well below the 60%+ levels of its 1990s-early 2000s peak), reflect policy-driven capitalization rather than purely organic operational revival. The original coverage notes the government infusion but understates how these funds have de-risked Intel's foundry ambitions at a moment when TSMC produces over 90% of the world's most advanced chips.

Synthesizing this with the Semiconductor Industry Association's March 2025 global sales data—which recorded a 13.2% year-over-year increase in worldwide semiconductor revenue, led by logic chips for data centers—shows the supercycle is broad-based. Intel's renewed focus on Xeon processors for AI inference and its push into advanced packaging align with the SIA report's observation that 'AI-specific accelerators and associated general-purpose CPUs are experiencing sustained double-digit growth.' A third primary lens comes from the Congressional Research Service report 'Semiconductor Supply Chain: Policy Considerations for Congress' (updated February 2025), which documents increasing market concentration: three firms now control 65% of global foundry capacity, while Nvidia alone captured roughly 85% of AI GPU shipments in 2024. The CRS document highlights how U.S. export controls on advanced AI chips to China, detailed in Bureau of Industry and Security rules from October 2023 and subsequent updates, have simultaneously constrained Intel's China revenue while accelerating Beijing's domestic alternatives.

What existing coverage largely overlooked is the historical pattern repetition risk. The 2000 peak occurred amid internet infrastructure hype; today's surge reflects parallel optimism around foundational models shifting to inference and 'agentic' AI, as Tan stated. Yet the CRS report notes that unlike the dot-com era, current concentration introduces national-security externalities: over 40% of U.S. advanced semiconductor demand still routes through Taiwan, a vulnerability underscored by the 2022 CHIPS Act legislative text citing 'strategic competition with the People's Republic of China.' Intel's ability to capture more inference workloads could diversify away from Nvidia dominance, but its foundry unit still depends overwhelmingly on internal orders, per its own 10-Q risk factors. This internal reliance raises questions about whether external customers (e.g., Microsoft, Amazon) will truly diversify or if the supercycle merely entrenches a new oligopoly.

Multiple perspectives emerge from the documents. Industry voices, including Tan's Bloomberg interview emphasizing 'huge demand' and factory ramp constraints, project continued expansion as AI moves to the edge. Policymakers, reflected in the White House CHIPS implementation updates, view Intel's recovery as validation of onshoring policy. However, the CRS analysis presents a counterview: concentration heightens systemic risk, as any disruption—whether from Taiwan contingencies, further export controls, or AI investment fatigue—could amplify volatility across the AI trade. The SIA data supports the supercycle thesis but cautions that memory and analog segments remain cyclical, a nuance absent from purely celebratory earnings recaps.

In pattern terms, the post-COVID 2021-2022 shortage, the 2022-2023 inventory correction, and the current AI boom echo prior waves but now overlay explicit geopolitical decoupling. Intel's progress on foundry diversification therefore sits at the intersection of commercial revival and national strategy. Whether this breaks the concentration pattern or merely redistributes it remains an open policy question documented across the cited primary sources.

MERIDIAN: Intel's crossing of its 2000 peak validates CHIPS Act onshoring effects and sustained AI demand, yet primary policy documents flag rising concentration risks that could trigger renewed supply shocks or accelerated decoupling if inference spending disappoints.

Sources (3)

- [1]Intel Shares Soar On Strong AI-Fueled Outlook, Surpassing August 2000 Peak(https://www.zerohedge.com/markets/intel-shares-soar-strong-ai-fueled-outlook-surpassing-august-2000-peak)

- [2]Intel Corporation Q1 2025 Earnings Release and SEC Form 10-Q(https://www.intc.com/news-events/press-releases/detail/171/intel-reports-first-quarter-2025-financial-results)

- [3]Congressional Research Service: Semiconductor Supply Chain - Policy Considerations for Congress (R47581)(https://crsreports.congress.gov/product/pdf/R/R47581)