China's LNG Imports Hit 8-Year Low Amid Middle East Crisis, Signaling Deeper Economic Weakness

March 2026 Chinese LNG imports are collapsing to 2018 lows due to price spikes from Iranian strikes on Qatari facilities, but this builds on a pre-existing 2025 demand slump that reveals broader economic fragility in China with global market repercussions.

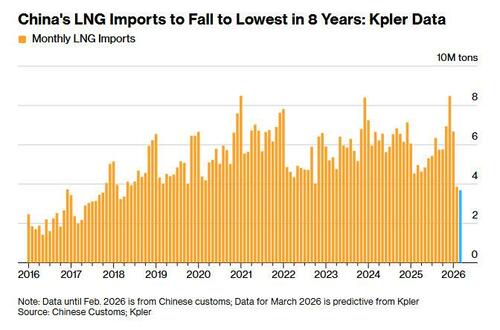

China's liquefied natural gas (LNG) imports are on track to reach their lowest monthly level in eight years in March 2026, dropping to approximately 3.7 million tons according to Kpler tanker-tracking data. This represents a roughly 25% decline from March 2025 and is driven by sharply higher Asian LNG prices following Iranian missile attacks on Qatar's Ras Laffan Industrial City, the world's largest LNG production hub. QatarEnergy has declared force majeure on multiple long-term LNG contracts with buyers in China, Europe, and Asia, with damage assessments suggesting repairs could take up to five years and result in substantial lost revenue.

While the immediate trigger is the disruption from the Iran-related conflict closing key supply routes and damaging infrastructure, this import crash occurs against a backdrop of already weakening Chinese LNG demand throughout 2025. Imports fell 11-12% for the full year 2025 due to milder winters, expanded domestic natural gas production, increased pipeline supplies, and greater reliance on coal, hydropower, and nuclear energy. Analysts had forecasted only a modest rebound in 2026, with volumes unlikely to recover to 2024 peaks, reflecting persistent softness in industrial activity.

This pattern exposes structural economic challenges in Beijing. Rather than aggressively bidding for spot LNG cargoes despite having storage buffers around 51%, Chinese buyers are prioritizing cost control and domestic alternatives. This restraint—uncharacteristic for the world's top LNG importer—suggests underlying weakness in manufacturing, real estate, and overall energy-intensive growth that mainstream narratives often overlook. The cascading effects are significant: Asian spot prices have surged, shifting restocking seasons later into the year for Northeast Asia and redirecting cargoes toward more price-sensitive Southeast Asian markets. Global LNG market loosening from weak Chinese demand in 2025 is now amplified by supply shocks, creating volatility that impacts European buyers, U.S. exporters, and commodity-linked economies in Australia and Southeast Asia. Connections missed by conventional coverage include how this accelerates China's energy security pivot away from seaborne imports while pressuring global producers and potentially hastening transitions in fossil fuel dependencies.

LIMINAL: China's aversion to high-priced LNG spot purchases highlights chronic industrial slowdown and overcapacity issues, likely reducing demand for global commodities like iron ore and LNG longer-term while boosting price volatility and accelerating Asia's energy diversification.

Sources (4)

- [1]China’s March LNG Imports Poised for 8-Year Low as Prices Spike(https://www.bloomberg.com/news/articles/2026-03-27/china-s-march-lng-imports-poised-for-8-year-low-as-prices-spike)

- [2]Iran attack on Qatar causes 'extensive damage' to massive LNG facility(https://www.cnbc.com/2026/03/18/iran-war-qatar-ras-laffan-natural-gas-lng.html)

- [3]QatarEnergy declares force majeure on some LNG contracts due to Iran war(https://www.aljazeera.com/news/2026/3/24/qatarenergy-declares-force-majeure-on-some-lng-contracts)

- [4]China's LNG imports set to recover in 2026 though not to 2024 level(https://www.reuters.com/business/energy/chinas-lng-imports-set-recover-2026-though-not-2024-level-2026-02-10/)