The Return of History: Geopolitical Shifts Driving Gold's Resurgence Over the Dollar

Deutsche Bank’s analysis highlights a 'return of history' as geopolitical shifts drive central banks, especially in emerging markets, to favor gold over the U.S. dollar in reserves. This article explores overlooked catalysts like sanctions, historical parallels, and the interplay with digital currencies, questioning whether gold can truly anchor a new monetary order amid the dollar’s persistent dominance.

Deutsche Bank’s recent analysis, titled 'The Return of History: Deutsche on Gold, the Dollar, & the Monetary Future,' posits a profound shift in global financial systems, driven by geopolitical realignments. The report argues that the post-Cold War era of U.S. hegemony and dollar dominance is eroding, with central banks—particularly in emerging markets (EM)—increasing gold reserves while reducing reliance on the U.S. dollar. This article delves deeper into the historical and geopolitical drivers of this trend, examines overlooked implications, and contextualizes the shift within broader patterns of currency devaluation and safe-haven asset accumulation.

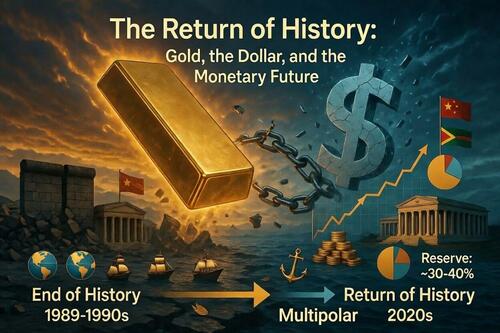

Deutsche Bank’s framework ties the resurgence of gold to three factors: the volume of gold held by central banks, its price, and the trajectory of global foreign exchange (FX) reserves. The report notes that gold’s share in reserves has tripled from a low to 30% today, while the dollar’s share has fallen from over 60% to 40%. This reversal of a trend that began in the 1990s—post-Berlin Wall and during peak U.S. unipolarity—signals a 'return of history,' where superpower struggles and geopolitical fragmentation drive financial strategies. However, the report underplays the role of specific crises and sanctions as catalysts. For instance, the 2022 freezing of Russian central bank assets by Western nations, totaling over $300 billion as reported by the U.S. Treasury, directly spurred de-dollarization efforts among non-Western states. This event, more than a generalized geopolitical shift, provides a concrete trigger for EM central banks to diversify into gold.

Historically, gold has served as a hedge during periods of monetary instability or imperial decline. The Bretton Woods system’s collapse in 1971 did not immediately reduce gold’s reserve share, as Deutsche Bank notes; rather, it was the geopolitical stability of the 1990s that marginalized gold. Today’s context mirrors the pre-1990s era of multipolarity, with rising powers like China and India leading gold purchases—China alone added 225 tons to its reserves in 2022, per World Gold Council data. This pattern suggests not just a reaction to U.S. policy (e.g., weaponization of the dollar via sanctions) but also a proactive strategy to anchor alternative financial systems, potentially tied to initiatives like the BRICS currency discussions. Deutsche Bank’s projection of gold reaching $8,000 per ounce if EM reserves target a 40% gold share assumes a static geopolitical environment, which may underestimate accelerating tensions or sudden shocks like further sanctions or trade wars.

What mainstream coverage, including the original ZeroHedge summary, often misses is the interplay between gold accumulation and digital currency experiments. While gold represents a return to tangible assets, central bank digital currencies (CBDCs)—with China’s digital yuan already in pilot phases across 26 regions as of 2023—offer a parallel path to bypass dollar dominance. This dual strategy among EM nations suggests a more complex monetary future than a simple gold-versus-dollar dichotomy. Additionally, the environmental and logistical costs of gold stockpiling, rarely discussed, could limit its long-term viability as a reserve asset compared to digital alternatives.

Synthesizing data from the World Gold Council’s 2023 reports and the International Monetary Fund’s (IMF) Currency Composition of Official Foreign Exchange Reserves (COFER), the trend of de-dollarization is clear but uneven. While the dollar’s reserve share has declined, it remains the dominant currency for trade invoicing and debt issuance, with 88% of international transactions still dollar-denominated as of 2022 (per IMF data). This inertia suggests that gold’s rise is more symbolic of distrust in U.S.-centric systems than a functional replacement for the dollar’s liquidity. Yet, if geopolitical fractures deepen—say, through a U.S.-China decoupling or expanded BRICS influence—gold could indeed anchor a new monetary order, as Deutsche Bank speculates.

The 'return of history' is not merely a financial story but a reflection of declining trust in a unipolar world. Gold’s resurgence signals a hedge against uncertainty, but its ultimate role depends on whether EM nations can balance tangible and digital strategies while navigating the dollar’s entrenched position. This tension, more than price projections, defines the monetary future.

MERIDIAN: If geopolitical tensions escalate, particularly between the U.S. and China, expect gold prices to surge past Deutsche Bank’s $8,000 projection within three years as EM central banks accelerate diversification from the dollar.

Sources (3)

- [1]The Return of History: Deutsche on Gold, the Dollar, & the Monetary Future - Deutsche Bank Research Institute(https://www.zerohedge.com/markets/return-history-deutsche-gold-dollar-monetary-future)

- [2]World Gold Council - Gold Demand Trends 2023(https://www.gold.org/goldhub/research/gold-demand-trends-2023)

- [3]International Monetary Fund - Currency Composition of Official Foreign Exchange Reserves (COFER)(https://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4)