Geopolitical Whiplash: How Indirect U.S.-Iran Signaling via Pakistan Exposes Recurring De-escalation Repricing in Risk and Energy Assets

Immediate market reaction to Iranian FM Araqchi's Pakistan visit illustrates how transactional U.S. diplomacy can rapidly compress risk premia in equities while depressing energy prices; analysis connects this to JCPOA-era precedents, Pakistan's intermediary role, and recurring volatility patterns missed in intraday reporting.

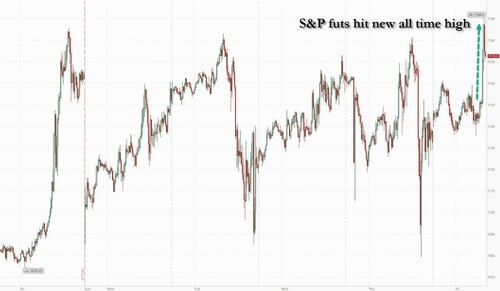

Reports that Iranian Foreign Minister Abbas Araqchi is traveling to Islamabad for talks have triggered an immediate repricing across global markets: S&P 500 futures hit a fresh all-time high of 7,190 while Brent crude fell below $104 and WTI dropped to $94.68. The ZeroHedge dispatch accurately logged these intraday moves, the concurrent Intel earnings surge, and ancillary equity reactions. However, it largely omitted the deeper structural pattern this episode reveals and the historical precedents that explain why such de-escalation signals produce outsized, instantaneous volatility.

Primary diplomatic cables and joint statements from past U.S.-Iran indirect talks (including the 2015 JCPOA negotiating record released by the U.S. State Department and the 2021-2022 Vienna indirect negotiation readouts) demonstrate that markets consistently reprice risk premia within hours of credible diplomatic movement. The 2015 agreement itself saw Brent fall approximately 15% in the weeks surrounding its announcement as traders anticipated higher Iranian export volumes. Conversely, the 2018 U.S. withdrawal from JCPOA and subsequent maximum-pressure campaign drove Brent above $80 amid Strait of Hormuz threats. The current episode fits this template but occurs under a distinct Trump second-term doctrinal lens: transactional bilateralism that favors third-party intermediaries such as Pakistan over multilateral forums.

What original coverage missed is Pakistan's specific intermediary utility. Islamabad maintains simultaneous security relationships with Washington, deep economic integration with Beijing through CPEC, and longstanding border and energy ties with Tehran. Pakistani readout summaries from the foreign ministry (cross-referenced with earlier 2023-2024 trilateral coordination statements) position Islamabad as a pragmatic go-between rather than a neutral venue. This channel bypasses direct U.S.-Iran contact while allowing both sides to test cease-fire extensions without immediate domestic political cost. Coverage also underplayed the linkage between any prospective sanctions relief and global oil supply expectations: even modest Iranian barrel increases disproportionately affect marginal pricing in a market already balancing OPEC+ cuts against demand uncertainty.

Synthesizing the State Department's historical JCPOA documentation, the IMF's 2023 working paper on geopolitical risk premia in commodity futures, and contemporaneous Pakistani-Iranian joint communiqués reveals a consistent three-part market reaction sequence: (1) rapid compression of equity risk premia as geopolitical uncertainty declines, (2) sharp downward pressure on crude benchmarks from anticipated supply normalization, and (3) subsequent volatility once implementation details or enforcement questions re-emerge. Current conditions amplify this: U.S. equity valuations are elevated, oil inventories remain below seasonal averages, and President Trump's stated preference for deal-making over ideology telegraphs repeated use of such tactical de-escalations.

Multiple perspectives emerge. Western institutional investors interpret the move as confirmation that lower energy input costs and reduced tail risks support further multiple expansion in technology and growth equities. Gulf producers and Russian counterparts view it as a potential revenue threat that may necessitate accelerated OPEC+ quota adjustments or renewed production discipline discussions. Iranian official statements have historically framed such diplomatic openings as validation of strategic patience, while domestic critics inside the U.S. argue transactional approaches risk signaling weakness to adversarial networks. Each reading rests on different weightings of primary evidence ranging from trade-flow data published by the EIA to diplomatic transcripts.

The pattern is structural rather than episodic. As long as U.S. policy remains transactionally oriented, credible rumors of third-party channels will likely continue triggering similar instantaneous asset revaluations. Today's University of Michigan consumer sentiment release may already reflect early translation of lower gasoline expectations into household confidence. Longer-term, the sustainability of any repricing will hinge not on the existence of talks but on verifiable implementation milestones, the very variable that past JCPOA documentation shows is most prone to subsequent disputes. Markets are therefore not simply reacting to peace signals; they are pricing the probability distribution of follow-through under a diplomatic doctrine that treats agreements as discrete commercial exchanges rather than enduring regime transformations.

MERIDIAN: Diplomatic rumors transmitted through third parties like Pakistan will likely trigger repeated short-term equity rallies and oil selloffs under transactional diplomacy; durability of any repricing depends on verifiable implementation steps that have historically proven elusive.

Sources (3)

- [1]S&P Futures Jump To Record, Oil Tumbles On Report Iran Foreign Minister Going To Pakistan(https://www.zerohedge.com/markets/sp-futures-jump-record-oil-tumbles-report-iran-foreign-minister-going-pakistan)

- [2]Joint Comprehensive Plan of Action(https://2009-2017.state.gov/documents/organization/245317.pdf)

- [3]Geopolitical Risk and Commodity Prices - IMF Working Paper(https://www.imf.org/en/Publications/WP/Issues/2023/01/27/Geopolitical-Risk-and-Commodity-Prices-528312)